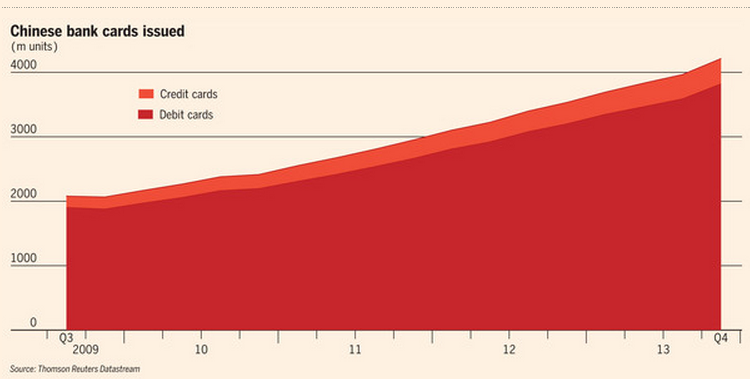

This is the Chinese Bubble in a graph from the FT, this morning:

There are now three credit cards for every Chinese mainlander.

I believe in the need for credit, but I also believe in the control of credit. This looks out of control.

There's a lot of potential for this to end in tears.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Not sure you are reading that right.

I see number of credit cards to be about 200 m units, so 1 in 6 mainlanders has a cc.

For debit cards then yes it’s 3 for 1

I am quoting the FT

Read the article again:

It states 3 BANK cards for each mainlander. The vast majority are debit cards. In fact there are only 391m credit cards. So 1 in 3.

I agree

I read the article

But debit cards are not neutral; they frequently imply credit shopping. Why do you need three each otherwise?

And they open the market for credit cards

As indication of credit risk I think my comments quite appropriate

You are indeed quoting the FT. And badly.

“Ten times more of them are debit cards than credit cards (3.8bn compared with 391m), but credit card issuance also rose by 19 per cent in 2013, and Euromonitor predicts credit card usage will grow faster than that of other cards over the next five years. “

I have already made clear why I have drawn the inference I did

It looks like the FT is actually saying just 391m credit cards for China. And the graph supports that. Are you wrong?

No: but it seems I could have made myself clearer

you misread it:

“China has a staggering 4.2bn bank cards in circulation, enough for every mainlander to have at least three. Ten times more of them are debit cards than credit cards (3.8bn compared with 391m), but credit card issuance also rose by 19 per cent in 2013, and Euromonitor predicts credit card usage will grow faster than that of other cards over the next five years. Overdue credit card debt — unpaid after six months — also leapt 72 per cent, but this is hardly US-style household debt: China’s overdue credit card debt is a mere 1.37 per cent of total credit outstanding.”

“No: but it seems I could have made myself clearer”

Nonsense. You made a mistake. That’s not a crime, we all make them, but the fact that you won’t even admit to it, despite it being so obvious, is quite worrying. You’re acting like a politician caught in a lie who’s trying to pretend he meant something different entirely.

And as for the issue at hand, what experience of day-to-day banking in China do you have to draw your conclusion that all these debit cards are so indistinguishable from credit cards that the difference doesn’t even bear recognition? How many ordinary Chinese people have you spoken to to ascertain why they might want three bank cards? Personally, I have three – but I’m not in debt at all. I’m not Chinese, though.

Pre-paid bank cards are widespread in China (as they are in most developing/emerging economies) – are they included in the figures you quote?

The FT piece is a positive one about a from cash to cards. What additional understanding, underpinned by what additional data, do you bring to the table to indicate that there’s a consumer credit bubble?

I should have said debit and credit cards

I agree

That was a mistake

It does not change the conclusions I drew

But if you disagree< that's your right

From the FT “Ten times more of them are debit cards than credit cards (3.8bn compared with 391m), but credit card issuance also rose by 19 per cent in 2013”

That is the evidence of the trend to which I was drawing attention. Phenomenal growth rare

Are the number of credit card roughly 4bn or are they simply the small orange portion at the top? If the vast majority of cards are debit cards that’s different since you can only spend money you already have with them.

See answer already offered

Not sure if I am missing something here, but the FT talks of “bank cards” not exclusively credit cards. 90% of the cards issued are debit cards, used simply for payment, not for borrowing. And the article points out that “China’s overdue credit card debt is a mere 1.37 per cent of total credit outstanding.” far less than that of the US.

So is this really a cause a for concern?

Yes for reason already noted to another commentator

Most western economies are heavily in debt to China so it follows that this problem ,if it is one, has the potential to undermine western finances just as likely as China . I think the Chinese financial management is pragmatic and can easily control internal credit if it thinks this is necessary. It is also managing internal demands for better living standards and preparing the internal market for the time when western markets run out of credit at which point the Remibi will become the dominant world currency as is already apparent in East Asian economies, whether they like it or not. Who knows when the Remibi replaces the dollar then the Chinese can do what they like just like the Americans today.

On the subject I would recommend Martin Jacques When China rules the world, a profound insight into China’s position in the world today.

But the ratio of credit cards to debit cards is tiny. And debit cards are credit at all, they’re deductions from your cash account. So what’s the problem?

The FT has joined the silly China about to collapse bandwagon. But even they say

“Ten times more of them are debit cards than credit cards (3.8bn compared with 391m), but credit card issuance also rose by 19 per cent in 2013”.

It’s three debit cards per person. It’s clearly shown on the graph.

No – it’s very clear the the FT is talking about debit cards, not credit cards. You either haven’t read it, or you haven’t understood it.

I think even the chart above says around 3.9 billion Debit cards and 300 million or so Credit cards- no? which would validate Jeanolivier comment. Unless I need glasses!

See my reply to him

The FT refers to “bank cards” not “credit cards” at that point

“4.2bn bank cards in circulation, enough for every mainlander to have at least three. Ten times more of them are debit cards than credit cards (3.8bn compared with 391m), . . ..”

It appears the article speaks more to debit cards than credit cards. A wildly different animal, even a nine year old knows the difference these days…..

I have made clear why I drew the conclusions I did in answer to other comments

How can credit be out of control if its about ten times less than you thought ?

You said 3 credit cards per mainlander

Now it’s clear that it is 1 card for every 3 persons.

How can you make the same argument when you got the numbers so dreadfully wrong?

A debit card cannot make credit go out of control.

Mutiple debit cards suggests thebagreesive selling of credit by banks

It is caled overdrafts

I am not quite sure why this relationship is so hard to see

Surely we need to see data on overdrafts to draw that conclusion, not debit cards?

I have 2 debit cards, only one of the of the linked accounts has an overdraft facility.

As has also been pointed out, pre-paid cards are popular emerging markets – these are most definitely are not an expansion of credit.

As a nation, we know China is a huge saver. The ratio of credit-to-debit cards supports the assertion that Chinese people are also savers – preferring to use money they actually have in their bank rather than by spending on credit cards.

I don’t see how this is any evidence of aggressive credit expansion in China.

China is subject to a massive banking bubble

You think this is unrelated to card expansion?

I don’t

But I could be wrong. It’s happened

Sometimes

Actually consumer overdrafts are rare in China so this is quite unlikely.

But once card usage is common the credit card follows

It always goes that way

Does it always got that way? Or are you just projecting based on the UK?

Doesn’t Japan have a problem due to too much private saving, as oppose to too much private credit? Isn’t it similar in Italy? They have debit cards. We had debit and credit cards here for a long time before the credit boom took off.

I’d venture that the primary drivers behind consumer credit booms are cultural. A savings culture is a powerful thing and if it’s deeply ingrained (as it is in China) it will take an awful lot to shift it.

I think that a fair point

But I suspect it is not as pervasive as suggested based on this rapid rise in the access to cash and credit

Cultures do change. 50 years ago people did not use much credit here

Time will tell

I think I am allowed to express concern

I agree, the culture can change – and it can happen quickly. I’m part of the UK generation that got swept up in it very quickly during the 90’s. I think that the savings culture in China is strongly linked to the lack of a state support infrastructure for the elderley. That’s a legacy of their past, but as the country get’s richer then it will change and might usher in a less frugal attitude amongst younger people – something that the Chinese government would probably quite like to see.

So of course, it’s a potential issue that shouldn’t be disregarded.

So we have moved to agreement – or something like it

I’ll accept I should have been clearer

This was not my best blog!

The real bubble to watch is the property/land bubble. How much of that is mortgage debt I have no idea, but I suspect that it may be seriously large.

It is very large

That and black money

I relate these issues: as we know, some will try to keep up and credit booms follow

I suspect I ma much closer to the truth here than many are crediting

Time will tell

I have read that China is full of empty apartment blocks (London is heading that way) -about 65 Million – so it looks like a real estate scam is in operation -you would have thought that their Government would have had more sense:

“The latest fear for developers in China in 2013?

“Wang Shi, CEO of Vanke told “60 Minutes” that developers are deep in debt. Many have abandoned projects midway through because the money dried up. He warned that if the bubble really did burst, China could see its version of the Arab Spring.”

See:http://www.thetruthdenied.com/news/2013/04/26/ghost-cities-in-china-64-6-million-empty-homes-apartments-condos/

“The middle class have invested massively in property and now estimates suggest that property investment accounts for as much as 20-30% of the economy,with 24 new cities are being built every year! The Government has allowed this expansion to continue to keep the economy growing but the level of infrastructure development is far ahead of the demand for property. Developers are going bankrupt, and in most cases have simply abandoned the projects for miles and miles.

Think once the initial interpretation of the graph was shown to be wrong, would have been wisest just to acknowledge the error because, as we see here, the result was always going to be your political enemies piling in.

i thought I had

I thought I’d also explained why I still was concerned about the trajectory – which is why I wrote it in the first place

But you can’t win them all – and if you think I got this one wrong, that’s life. I am not perfect and I know it

Really. Then admit that your whole post is based on a simple error.

I have said I should have said credit and debit cards, not credit cards alone

That was a mistake

Why the aggression?

Richard for once I completely agree. China’s bubble at $24 trillion is the largest the world has ever seen. Its crash will likely cause something worse than 2007. It is not only banks, but the shadow banking system, along with local government debt.

Stay tuned on this issue, there will be more.

Thanks

It would be interesting to see total lending figures for China including bank overdrafts and other loans as well as credit cards – and for the business sector as well as households. My guess is that the rate of increase is very high indeed but I haven’t seen reliable figures to back this up.

personal debt very low. Corporate debt expanded by approx $15 trillion since 2008, as the government ordered banks to . “Extraordinary” is the only word that comes to mind…

Bar graphs of credit to debit spend for some selected countries.

http://www.theguardian.com/news/datablog/2013/jul/03/uk-card-use-debit-credit

I’m not sure what to make of that

Yes I bolted that reply. Comparing EU debit card and credit card spending (2012);

http://www.theguardian.com/news/datablog/2013/jul/03/uk-card-use-debit-credit#sthash.tqhefB9I.dpuf

with China data (quoted for 2010);

http://www.china.org.cn/opinion/2011-05/03/content_22485157.htm

Debit card spending ‘Total retail sales of consumer goods’ for China in 2010 is estimated from data in the above links to be just over half the EU average (in £) and credit card less. It’s the rate of increase of spending by debit card and credit card that China.org.cn focus on, in 2010 its quoted as 18.4%, with credit cards expected to exceed this rate in future. The article’s title was “China bankcard holders more willing to spend”, and aren’t they.

For EU data

At the very least that seems to suggest changes to those supposed savings ratios

I’m not sure how significant figure like this are, taken out of context. Beyond the hothouse environments of Beijing and Shanghai, vast swathes of the Chinese mainland population live in little more than third world conditions, as witnessed by a gini coefficient of 47, higher than our own (40), and the US (43). Fixed term contracts are the norm, with no requirement for an employer to renew, making long term income precarious. (Employees have no holiday entitlement in the first year of employment and can be dismissed for any reason during the six month probation period, which is likely to encourage those hiring to take on new workers rather than renew contracts).

China as a consumerist, acquisitive nation is in it’s infancy, unlike the sophisticated marketing machine which has been launched upon its population. Already you can see the signs of changing social mores that, as in 80’s Britain, encourages society to judge citizen’s worth by the property they own. That need to compete, coupled with employment insecurity, in a country of vast inequality that makes the expansion of credit,(and let’s not forget credit banking in China is itself still in its infancy), potentially dangerous.

This article is discussing debit cards not credit cards, please note.

It is discussing both

I and others have already addressed the issues: please rescue the comments

Thanks

¨Compared with the level a year ago, the growth in debit cards has accelerated 3.8 percentage points while that of credit cards slowed 1.5 percentage points, said the bank.

In the third quarter, a total of 10.08 billion transactions worth 88.2 trillion yuan (14 trillion U.S. dollars) were made through bank card payments, while per capita bank card consumption reached 4,151.97 yuan in the three-month period, according to the PBOC report.

Meanwhile, credit card loans that were more than six months overdue rose 8.8 percent quarter on quarter to hit 14.43 billion yuan, accounting for 1.4 percent of all credit loans outstanding, at the end of September¨

http://english.people.com.cn/90778/8035055.html

1$ = 6.1 yuan

http://thediplomat.com/2012/09/are-chinese-banks-hiding-the-mother-of-all-debt-bombs/

hmmmm….

I have three bank accounts in China, each with a different bank. That arrangement is to compartmentalise my finances and spread my risk. I have a debit card for each account, but no overdraft facility is available to me as an individual – although I could get a loan to assist in the purchase of property, guaranteed by that same property.

Note that for security reasons a relatively low limit is placed on each card as to the maximum amount that can be transacted or withdrawn at any one time. That is another reason why carrying more that one card is common.

Although transactions using credit card are not so widespread, I do have a credit card with a mainland bank. However, there are no facilities for extended repayment over a period, the full amount must be settled each month.

My situation is not unusual and my banking arrangements are probably quite typical. It seems to me that any risk to the banking sector would not at all be from exposure to individuals.

Do you honestly think we can extrapolate from you?

Sorry: that’s a pretty extravagant expectation

To make sense of the number of cards in issue you would need to understand the number of providers, what credit regulations exist, and the actual credit incurred on the cards. In an emerging and growing economy like china the number of cards per person and in total is likely to be large, and growing. That says nothing about the level of personal debt, and nor does it really indicate how that will turn out – there are other factors to take into account. Not least the practical differences in debit and credit cards in China – much to easy to assume they will work as they do here!