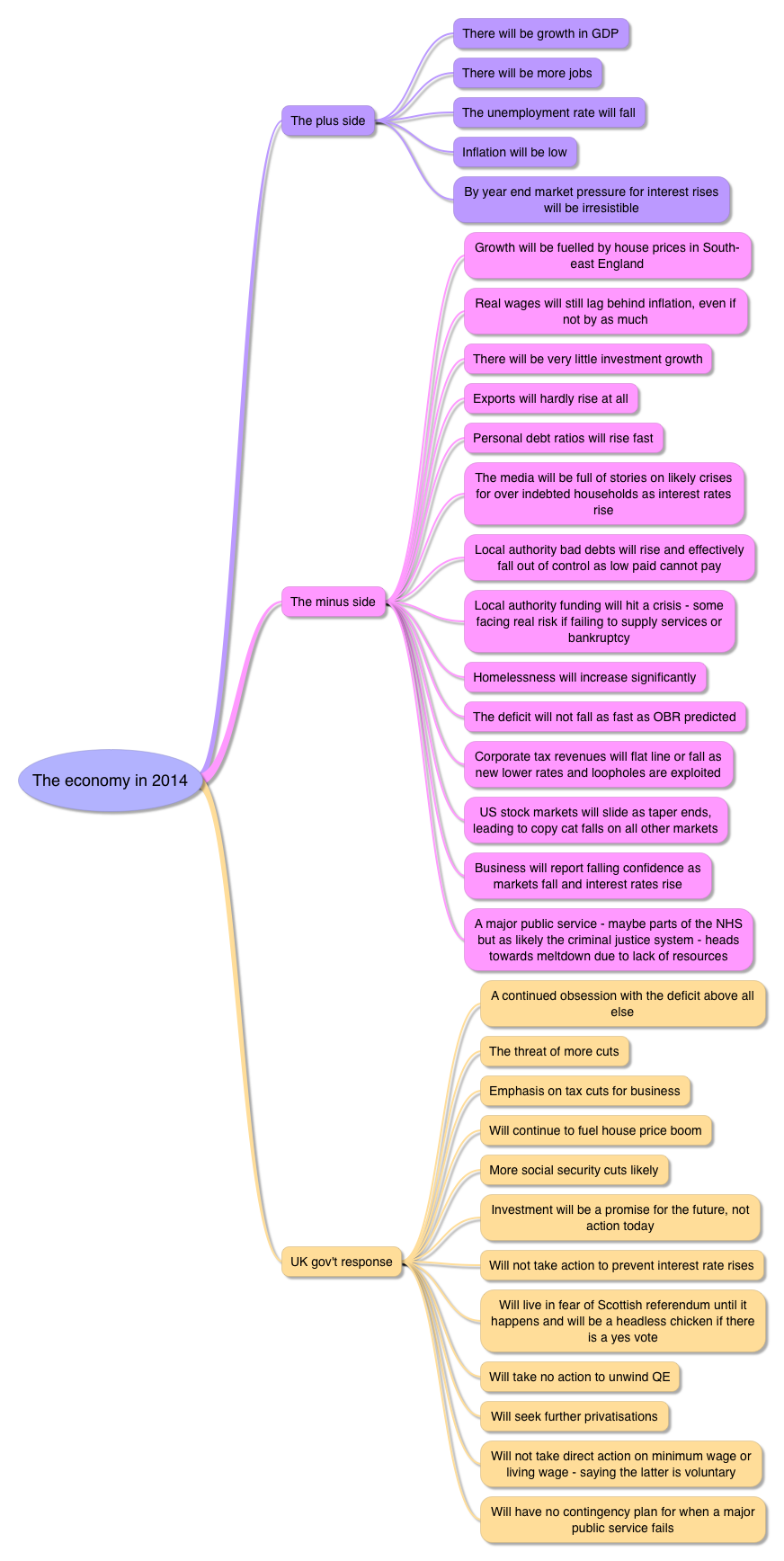

Looking at the year ahead and the range of work that needs to be done on tax justice issues I have a feeling I may be giving less attention to the economy as a whole than in the last year or so. That said, I couldn't help but muse on the economic outlook for 2014. You'll gather from what follows that I am not too optimistic. Click on the image for a bigger version if it's too small on what you're reading it on:

The only thing I can guarantee about that list is that it's wrong. All economic forecasts are. But I think the tone is right.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

There has been a risk people will be lose their house every year for the past 10 years. Maybe 2014/15 will be the time it happens. At least it will correct the housing market.

Your callous indifference means that your comments are now being deleted

I ask some simple questions, nothing more.

As for the housing market we have all known for 10 years its been a problem. Anyone who tells otherwise is not telling the truth.

Is it normal of you to delete comments you cant answer or like??

I delete obvious neoliberal nonsense

Or comments that show a complete indifference for human suffering

You offered both

It’s called editorial freedom and I like it

It’s true that the housing market does need to be corrected but that should be a course of action to be developed over time – real people take a hammering when costs rise rapidly at once.

Frankly, I’d simply expect the CotE / GotBoE to make it harder for people to get mortgages at unrealistic interest rates but to announce the policy well in advance along with plans to allow LAs / HAs far more freedom to borrow to fund new builds and suspend the RTB on those new builds for at least 50 years.

For once, I have some sympathy with you

But the first one is significant because it’s such an important dynamic and ‘lifts many boats’ for example consumer confidence/spending , business confidence/investment possibilities and the government’s tax revenues. That I guess is the economics of a bigger cake but the politics is of course how the cake is shared out. But then I muse surely even under Labour or other configurations we would be looking at more state money ‘proportionately’ going on the massive demographic increase of the elderly,their pensions, their health care and their social care needs. So I guess what I am saying is yes we may have growth but more of it will be needed & some hard choices will continue who ever wins in 2015.

Please stop re-hashing trickle down theory

Respectfully, Richard I wonder if you have misunderstood my point which is that economic growth ( + improved tax revenues) your first point on the list- generally brings benefits to society as it did in the early to mid 2000’s under Blair when we were able to spend more on say all levels of education, health, infrastructure, reduced child poverty. I am not referring to the rich spending more and I fully appreciate that it is for the government to do the most socially just thing. I always think Denmark for example should be one of our models of a fairer society.

OK – sorry if I did

Have to agree – the economy may well get bigger but the pace of growth will not cover the rise in expenses related to pensions, health and welfare spending. Sooner or later the crunch will have to faced and the issue of universal benefits discussed.

Quite whether any political party or politician will have the stones to start that debate is of course a matter of some interest – after all when Frank Field raised points for discussion when the LP were in power, he was sacked for saying them!

The setting of spending priorities is going to be tough no matter which group(s) form the next govt. and I think some on the Right and Left are deluding themselves if they differently.

What I want to know is what you propose instead?

There is no savings medium that can deliver an alternative mechanism – private pensions are already almost wholly paid for by tax reliefs, not investment returns

So what do you want? Euthanasia?

I seriously suggest that is what you are proposing, whether you like it or not

Hope you had a good break, Richard.

This is a bit depressing but looks realistic. The govt. response looks about right-unwilling to take action even when they can.

In 1966 Wilson faced a crisis and he had six levers. One temporary tariff increases-no longer possible, in or out of the EU. Two, the exchange rate was more or less fixed, not set by the market. Three, we still had capital controls, four, more of the economy was state owned-much has been sold off since then five taxation could be put up -now we are told to will deter foreign investors. He didn’t have to deal with huge amounts being siphoned off to tax havens. Lastly, the interest rate is -in theory- now in the hands of the Bank of England not the Chancellor. All of those levers have been surrendered. Yet we still have politicians trying to take credit for the economy or blaming the other side for its poor performance. I wonder how far a govt. really has control of the economy. I can’t see things improving until they provide real leadership.

Agreed

I’d bring interest rates in house for a start

Indeed – there is just no vision of social justice only craven, cowardly and sub-reptilian men/women in suits displaying cheap opportunism and scamming and lying to the public. Expect a good deal more of this blather only with the volume cranked up! We need something like the 19th Century American break up of big corporations (Anti trust laws). Mill talked about capitalism being ‘wealth diffusion’, instead we have the whole populace being enema-ed and cathetered to death and hardly anyone objects! On his travels, the early Quaker, George Fox, noted in his journal that the populace was in a ‘sleepy’ state – I would say it is now narcolepsy and zombification, the prerequisites for fascism.

I agree with Nigel’s comments, although I probably wouldn’t have phrased them the same.

We have an absurdly over-inflated housing market. Why hasn’t there been a crash ?

The answer, I think, is that the banks know full well that if they start foreclosing on the homes of everyone who, in truth, has no hope of ever repaying their mortgage, they will have pulled the whole edifice down on themselves. Think Smaug in a pin-striped suit. Once they start foreclosing they will be left with thousands of houses to sell into a falling market, which will, of necessity, start to fall faster, leading to more foreclosures both bank-lead & voluntary (think of the 80s where people were trying to give the house-keys back to their building society), leading to ANOTHER bank melt-down.

Therefore, the banks don’t foreclose. They also don’t lend out even to good businesses because they are sitting, paralysed, on a monstrous icicle of unrepayable debt.

Ways out:

1 Pop house bubble & except foreclosures, even with a heavy heart. After all, why should the couple that took out a £200k mortgage on a £40k salary benefit from the more intelligent couple who realised that was insupportable & struggled on in rented accomodation?

2 Massive wage inflation & the £ sinking. Electorally advantageous but effect is that the thrifty pay for mistakes of the spendthrift (see 1 above)

3 QE. Certainly the worst outcome. It solves nothing & just allows the rich to get richer while the can gets kicked down the road.

QE does down the national debt, we’ve covered that here before… anyway, peering myopically into your diagram I see growth mentioned, my personal hope would be that at last the need for growth and the reasoning behind it is publicly expored! Bye-bye banksters!

I might add too, by way of query, why aren’t we discussing what scams mortgages are in the first place and ways of ending them instead of how we can afford them along with pensions and healthcare etc.? Mortgages as we know them, involving a life-time’s working to pay compound interest on so-called ‘loans’ which never actually happened in the first place, shouldn’t exist – so why are we calmly accepting them? If we got rid of them and other scams embedded in the structure of everyday life there’d be a lot more money to play with and a number of former parasites down at the Job Centre where they should be. Where’s the discussion? Who do I vote for to get that? No-one at all it seems. Where’s the point then?

Bill

If people want to own their own houses there isn’t an alternative. Even in the ’50s, when house prices were, massively, ridiculously, cheaper in real terms than they are now, my Dad’s buying his own home for cash entailed living with his mum until he married in his late ’30s. The vast majority of (at least white English) people won’t cope with living with their parents until they are 35 or more.

The alternative is saying “Mrs T was wrong about many things, but, above all, wrong about ‘Right to buy’. Most of us, outside the v wealthy, should live in Council accommodation”. That is, probably, the correct answer. It is also electoral suicide, I’m afraid.

The central bank could provide cheaper loans, by which I mean it could create money as debt and charge a whole lot less interest than the banks do ss it would be driven by a service motive rather than a profit motive. However, since we use fiat money these days, backed by what people think of it which means to retain value it has to be used to create proportionate wealth and not widdled up against the wall, I see no real reason why the central bank shouldn’t pay for new builds, flats and houses as appropriate, which can then be given to those who need them. I’m talking about servicable homes rather than anything palatial. See? There’s always an alternative. Let’s not forget, finance simply never should have been alllowed to influence our lives to the extent it has. Removing that influence is going to take us into the realms of what’s to us bizarre. It’s because normality, not being robbed at many, many levels by the banks, will seem bizarre because we’ve become so used to being fleeced as a matter of course. It’s high time we stopped being milked by the banks aided by their partners in government.

There is a brilliant graph in today’s Huff Post “Britain’s Housing Crisis Explained In This Simply Depressing Graph”, from research at University of Sheffield School of Architecture and Architecture.

A quantitative account of the ‘failure’ of the housing market for the ordinary citizen and “How Britain’s housing has got steadily more expensive as the rate of house building became steadily more sluggish”. It shows the Coalition Govt so far is depressingly and equally successful, as the recent recession, in destroying house building. Most of us only want (or dream of) one [house] to live in. Not built for the needs of investors.

http://www.huffingtonpost.co.uk/2014/01/02/housing-market-uk_n_4531425.html?utm_hp_ref=uk