I was amused (in a depressed sort of of way) to read the Observer's headline yesterday saying:

David Cameron to curb 'fat cat' pay with people power

It takes some considerable stupidity (no point beating about the bush here) to suggest that when the market has failed (as it has) that individual shareholders can be given the power to put things right.

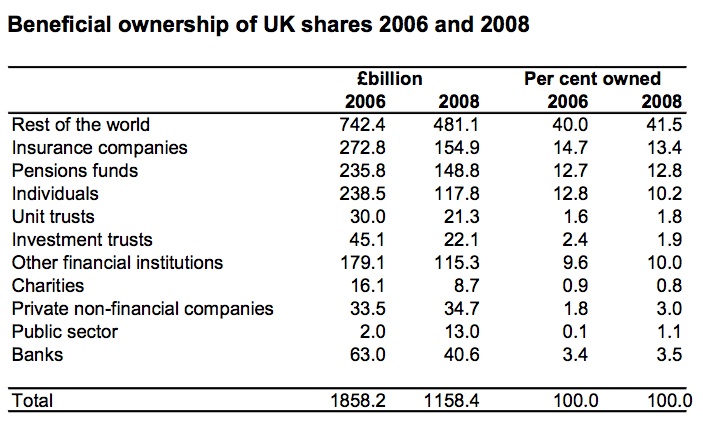

Let's think about why that isn't going to happen. The last survey of share ownership in the UK was prepared by the Office for National Statistics in 2010 based on ownership in December 2008. It showed the following:

So Cameron says 'people power' voting against high pay is going to solve the problem. Let's ignore how Blairite that sounds for a minute, let's instead just look at the reality of it.

More than 40% of the FTSE is owned overseas. They're not going to run to the defence of the UK economy.

Pension funds and insurance funds are for all practical purposes similar - and part of the same financial power hierarchy as the banks. So they're not inclined to vote for change. Sorry to be so cynical - but this group have shown themselves time and again to persistently fail those whom they are meant to represent and to side solely with those who might pay their bonuses - many of which are based on inappropriate trading and, frankly, churning.

The same pretty much applies to the banks and all other financial institutions.

So in the vast majority of cases we're down to charities and individuals. The trouble is those individuals are likely to be very wealthy. And first they don't vote - their fund managers do for them and second whose wide are they on?

So maybe charities and the public sector can be relied on to support the call on most occasions.

So much for 'Cameron's people power' but candidly it's so ludicrous an idea he really must think we're stupid to believe that all these people will vote against high pay.

And yes. I know the odd resolution has got support counter to this argument - but it's so rare it's simple proof of the rule. They've also almost never been won.

So Cameron is offering reform safe in the knowledge it will never harm his friends. How Tory is that?

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Here we go again with Cameron playing to the gallery following the example set by Clegg. These people have no idea what they are talking about and yet they are running the country. I would really like to emigrate but unfortunately I am far too old and and most destinations in the West are in the same mess because of the same neoliberal policies. How much longer will we have to tolerate this nonsense from our unconvincing politicians more interested in spin and a soundbite than doing anything constructive to help our failing economy.

1) Foreign shareholders won’t vote against large pay rewards to CEOs because they are concerned or not about UK income inequality they will vote against large pay packages because it is in their financial interests not to reward CEOs for failure with “their” money.

2) UK fund managers I know are just as concerned about CEO rewards for failure as anyone else. Individual fund managers get paid bonuses based on strict performance criteria (investment performance being easily measurable unlike management skill) so keen that others are held to same standards. (And yes I agree that fund management firms charge too high fees for indifferent performance). The reason that they don’t vote is institutional and clerical. The fund manager at a desk in front of a Bloomberg, or going to meet Unilever’s finance director, never sees shareholding voter forms or gets asked by back office what the house view is on XYZ’s re-election as director. This can all be changed if legislated by government and forced on fund managers to be more pro-active.

Agreed

Page 6 of that ONS report which shows the diminution of individual shareowners from over 50% in 1963, down to just under 30% in 1981, and then down to just over 10%. My favourite historian (for I do have one!) Stefan Collini, when discussing R H Tawney, used the term ‘absentee shareholders’ (on the model of absentee landlords). Collini was referring to Tawney’s assessment of the abysmal health and safety record of the UK’s interwar mining industry. I think that the term fits here also.

One of the issues with individuals getting actively involved in voting on appointments and renumeration packages is that it is complicated and time consuming to do properly.

Someone with a SIPP or who has been investing in ISAs for years will probably end up with a portfolio of a number of blue chip FTSE100 stocks.

You will then be faced with a deluge of documents asking to vote on XYZ’s appointment and salary. BP wants a new Finance Director on £2m and such-and-such an incentive scheme. You go off and check what Shell pays their FD. Is it more or less ? Is that deserved ? It’s an interesting task to some but I expect 90% just won’t bother.

Hence the reason why it has to be done by the institutions who have the staff, time and tools to monitor and judge these things objectively and efficiently.

There’s a question- more of a rhetorical one than a real one, about who gets to express their will this way.

It used to be the case that most employers’ penstion schemes in the private sector were defined-benefit schemes. When that was the case, the pension beneficiaries didn’t get much of a say in the decisions made by the scheme’s trustees. Fair enough- after all, it’s the employer that is on the hook if the investments don’t perform, the only agreement with their employees is to pay the pension at the agreed rate.

Now though, everything has changed, most private sector schemes are defined-contribution. The risk has been switched from the employer to the employee, so if investments don’t perform in the long term, it’s the pensioner who suffers if poor decisions are made. Yet, they’re still isolated from virtually all the decision making, that all happens at the fund level. It doesn’t seem morally right for employees to suffer the consequences of poor long term shareholder decisions, without having any input into what is decided on their behalf.

How much of the stocks are actually controlled by long term shareholders as opposed to people who are just taking short term positions (betting, churning) – and unlikely to ever intervene?

Genuine question that, I have no idea.

Nor me

I don’t have the exact numbers either but I suspect the vast majority of day-to-day trading of the FTSE100 is between short term traders, hedge funds, high velocity trading platforms and the constant rebalancing of derivatives contracts.

However the majority of blue chip stocks held will be by long term holders.

Pension funds, insurance companies and the large unit trust groups will have held large positions in BP, Shell, Unilever etc etc since time immemorial.

And of the 40% foreign shareholders these are going to be largely the large international funds like Fidelity or Sovereign Wealth Funds whose modus vivendi is as long term holders.

The entire market turns over in about 7 months on average

That shows the bias towards short term ownership

And churning by investment managers

The overall average disguises what is actually happening.

(Simplistically).

Hedge funds (10% of FTSE assets) turn over portfolios 10-30x pa.

Pension and insurance funds (90%) turn over portfolios 1x pa.

The likes of Scottish Widows will have held between 3-6% in BP since WW2. They are a long term holder. They’ll be meeting the CEO and FD twice a year.

Whereas some hedge fund running complicated algorithm trading strategy based on some black box nonsense will churn the FTSE on a daily basis.

Investment managers have no incentive to churn, in fact it is quite the opposite given that churn reduces the assets under management on which they charge their fees.

Some discretionary stockbrokers who still charge on the base of commission would benefit from churning, but they would be such a tiny part ofthe market as to be immaterial.

Short-term owners such as hedge funds would be responsible for most of the turnover, peversely they are the one most active in engaging managment and voting against things they believe are not in their interest.

Being a long-term holder is not the same ting as managing for the long term interests of society in general though. BP is a great example- fund managers love BP because it generates large cash dividends each year (or, it did). It also has a terrible safety record. Those two facts are probably not entirely unconnected.

The issue here is, the nature of a fund forces fund managers to interpret the interests of their ultimate beneficiaries (that is, the pensioners and other real people for whome they manage the fund) in a very specific, narrow way.

Obviously it wasn’t in the long term interests of the general public to allow BP to overlook safety checks over many years. Small shareholders tend to ask difficult questions about safety, the environment and corporate responsibility in general. Those are really long term concerns. Instutions focus on cash flows, and returns over the next few years. A fund manager doesn’t even have a mechanism for finding out what his customers broader concerns are, and a fundholder has no method of communicating them.

Each year after privatisation I voted against the Director’s remuneration package when I received the Northern Rock annual invitation to the Shareholders meeting. We all know how much effect that had.

Not only did nothing happen, but having overpaid all the Directors, I seem to have ended up now paying again through my taxes and somehow Richard Branson ends up with a Bank at half price.

Unfortunately David Cameron and his gang just don’t get it and his solution is the usual wishy washy Big Society type mix of amateur volunteer groups and individuals to try and square up to the wealthy and powerful.

The only sensible measure – employee representation on remuneration committees – is out of the question for ConDems. On Radio 4 yesterday Danny Alexander refused to support the idea when pressed several times. FFS what is the danger of one representative from the main stakeholder? IMOthe composition of remuneration committees should be at least 50% the workers who create the profits.

Another issue with allowing shareholders to set executive remuneration levels is that what constitutes ‘good’ performance from their perspective isn’t always what constitutes ‘good’ performance by employees, taxpayers or governments.

Many companies cite one of the reasons for using overseas tax havens as a need to please shareholders and boost their share price. But companies that were founded in the UK, built on decades and centuries of UK labour and custom, depriving the UK of much needed revenue at a time when many of their employees and customers are struggling with austerity may not be popular.

With regard to banks, how does one define how a bank has performed ‘well’ in the current climate? For example, if Lloyds Group makes a slightly less massive loss this year than last, is that really worthy of a multi-million pound bonus for the Chief Executive? One can argue that all UK banks owe their existence to public financing. According to the Bank of England, the exchequer, including support from the British taxpayer, provided more than £1trillion of public money to rescue banks from collapse. Through short-term loans, loan guarantees and quantitative easing the Bank of England helped to bolster bank’s balance sheets. Banks, even those such as Barclays and HSBC that did not receive a ‘direct’ bailout, therefore benefit from a promise that taxpayers will never let them fail, because it would be too damaging to the UK economy. Thus, even though it did not take any direct state help during the financial crisis, former Barclays boss, John Varley, had to acknowledge the crucial role played by the government in rescuing the City as a whole:‘Even those banks who did not take capital from governments clearly benefited (and continue to benefit) from these actions. We are grateful for them, and our behaviour should acknowledge that benefit ‘

So some might say it is UK taxpayers who should be having a say on bank bonuses and remuneration. At the very least we should have a direct say in that regard with RBS/NatWest, 84% owned by taxpayers.

The highly controversial takeover of Cadburys by Kraft, funded by that same 84% taxpayer owned RBS/NatWest, may have been viewed as a ‘good’ idea by shareholders of both companies and the bank who voted it through. But it was not necessarily a good thing for the UK business community or the workers at their Keynsham, Bristol site which closed, despite initial promises to the contrary.

And the recent Virgin Money takeover of Northern Rock, which saw bonuses for Northern Rock chiefs brought forward, may have been deemed a ‘good’ performance by both shareholder boards. But taxpayers lost out to the tune of £400,000,000.

[…] commentator on this blog this morning has made an excellent point on pensions: It used to be the case that most employers’ […]