Terry Le Sueur, finance minister of Jersey wrote to all members of the States of Jersey yesterday telling them why he thought Jersey will be EU Code of Conduct compliant when the Isle of Man was not. His letter reached me this morning and is available here. It's worth a read to make sense of the argument that follows.

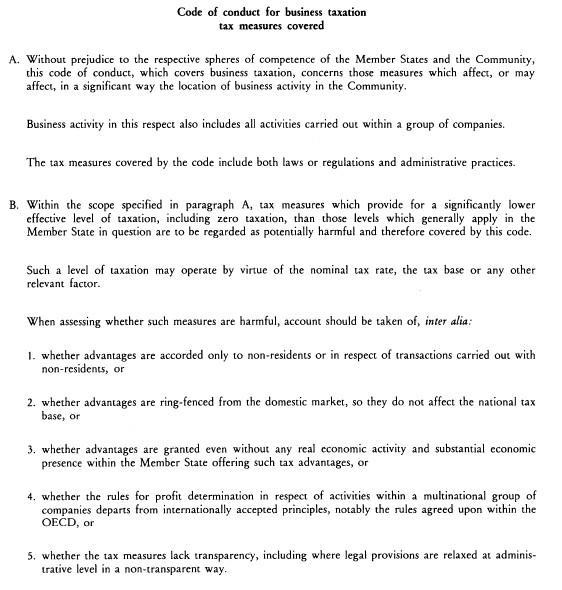

I'm afraid I think Senator Le Sueur is wrong. To put this in context the Code says this:

To date most objections to the Code have concentrated on Section B and its five clauses as they relate to law and regulation with regard to the payment of tax. What Senator Le Sueur has not noted (and nor has the Isle of Man come to that) is that section A also relates to administrative practices.

What both now propose are rules that say if a company owned by local resident people (but not other companies) does not pay sufficient of its profit to its shareholders in dividends on which they can be taxed then the locally resident shareholders (alone) in that company will be liable to pay tax on a dividend that the company is deemed to have paid to them even though it has not done so. And the tax they will be charged will be based on the profits of that company that would have been taxed if only it had been liable to make a tax payment, even though it is claimed that no such liability exists. Lewis Carroll could be forgiven for such a plot, but this claims to be reality. And the motive is unambiguous. It's to stop local people having the advantage of the 0% tax rate being offered to non-residents.

Let's be clear therefore: no one is pretending there is no ring fence in the new rules put forward by the IoM and Jersey. There is. They know there is. That's what they say they intend. All they are saying is that, to quote Le Sueur "This is [now] a personal tax measure. It is not a company tax measure." In other words they are seeking to use trickery to get round the requirements of the Code. So much for the claims made by the islands that they comply with the Code and are, to quote Allan Bell "responsible nation[s] hosting quality international businesses". This is untrue. Their actions are straightforwardly deceitful, and an obvious and intentional abuse of the Code.

But proving deceit is not enough to prove they are not Code compliant. They're not Code compliant for very logical reasons:

1) A shareholder cannot pay tax on the deemed taxable profits of the company (even though it has none according to law) unless the company first of all prepares a tax computation and secondly supplies it to both the Comptroller of Income Taxes in the jurisdiction (who will otherwise be unaware of the need to demand the tax due on a deemed distribution) and to the taxpayer themselves. This action of requiring a company to prepare this computation which it would not need to do if it did not have local resident members (and Jersey has stated quite categorically that it will not need tax computations if there are no such members) is the creation of a first administrative ring fence. And since the company has to be party to this process, and the process relates solely to its activities and not to those of the shareholder, it is impossible to argue that it does not relate to business taxation.

2) The requirement that the company supply its tax computation to its shareholders, a requirement otherwise unknown throughout the OECD, is a second administrative ring fence.

3) The fact that the liability arises whether or not a dividend has been received must also suggest that the tax measure lacks transparency. After all, the tax payer has a liability over which they have no control or say. What can be less transparent than that?

4) The fact that the company has to prepare a tax computation when it is cl;aimed it has no tax liability has to be a process that by definition lacks transparency. It is so opaque it is surreal.

5) To argue that this is a personal tax charge is so obviously disingenuous that you can imagine that the Code of Conduct Group are not going to look on this matter favourably from the outset. After all, the Code is just that - a guideline for acceptable behaviour. When it is so obvious that Jersey and Isle of Man are seeking to treat it as a rule based exercise it is clear that first of all they do not understand the Code and second they have no intention of complying with it. The Code Group will be pre-disposed to reject their obvious charade as a result.

So I've tough news for the Isle of Man and Jersey's - you're still building your economic futures on sand, and time is running out for you to find an alternative when none seems available.

So what are you going to do?

NOTE: Please also read this article which continues this argument and adds two more reasons why Jersey will fail the requirements of the Code of Conduct. (Added 19-11-07)

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

[…] Recent Comments Transparency International – one small but crucial step : AccMan on Mike Rake – a Knight too farTax Research UK / Russian corruption? on The Tax Justice Network Code of Conduct for TaxationTax Research UK / 2007 / November / 19 on Northern Rock: the core of the issueTax Research UK / Jersey will fail the EU Code of Conduct on Jersey: more reasons why it fails the EU Code of Conduct.Tax Research UK / Jersey begins to panic on Jersey – beginning to sink […]

All very interesting with one minor problem. According to Jersey… they are not IN the EU. And therefore have no code of conduct to fail. They did, however, form a trading agreement in 1973. But they are under no obligation to comply with EU, UK or any other tax laws than their own.

While we are on the subject, neither does the Isle of Man nor Gibraltar.

If you really want to go after tax havens you need not look any further than the top rate earners in the UK and how they avoid tax by taking dividend over and above the traditional limit. Or perhaps Tesco who TELL HMC&R what they are going to pay in tax each year.

Robert

The Crown Dependencies and Protectorates have their foreign affairs managed for them by the UK.

And they are not states in their own right.

For that reason UK foreign obligations apply to them

The UK is a member of the EU. It must apply EU rules to them in this area, and as such the EU code does apply.

Richard

Richard,

I know what you’re saying and I can understand your motivation in doing so.

Your comment “The Crown Dependencies and Protectorates have their foreign affairs managed for them by the UK.” is very misleading and inaccurate.

The fact is that the Isle of Man is self Governing (Tynwald). The Queen is ‘Lord of Mann’. The Isle of Man holds neither membership nor associate membership of the European Union. It trades with the United Kingdom under Protocol Three of the treaty of accession. In which it states that “the Principality of Monaco, the Isle of Man and the United Kingdom Sovereign Base Areas of Akrotiri and Dhekelia shall not be treated for the purpose of the application of this Directive as third territories.”. The directive being the inclusion of “Czech Republic, Estonia, Cyprus, Latvia, Lithuania, Hungary, Malta, Poland, Slovenia and Slovakia” into the European Union and the reforming of the member states. In other words, IOM, Monaco and Akrotiri and Dhekelia are NOT to be included in the new EU.

In conjunction with the Customs and Excise agreement with the UK, this facilitates free trade with the UK. While Manx goods can be freely moved within the EU, people, capital and services cannot. EU citizens are entitled to travel and reside in the Island without restriction; but only by laws established by Tynwald and not empowered down on them by the UK Government.

Just because the UK has makes Foreign Policy decisions doesn’t automatically have a cascade effect on it’s dependencies.

The IOM has the right to accept or not accept FCO policy and even has additional clauses to laws it has accepted (usually regarding the process of legal precedence).

So while it has agreed to certain international anti-criminal laws that have been established; it has a fundamentally totally different immigration policy.

I think geography has a lot do with this. If the Isle of Man was in the middle of the Atlantic we wouldn’t be having this debate.

Plus your assertion that what is law in the UK is therefore law everywhere in British territories is also false.

Do I feel that the IOM is immoral or allowing corruption of Tax Law as a result of this state of affairs? Well, given HM C & R moved the Trading Fund it uses for building management to Gibraltar, no.. I don’t.

Robert