The response from commentators (Jo Michell, Jonathan Portes, retweeted by Simon Wren-Lewis) on Twitter to the ongoing debate on Labour's fiscal rule that I sparked has been to say that the likes of Bill Mitchell and I, who have responded to them, have not understood what the rule says. Jonathan Portes, for example, says this: So, let me avoid doubt and reproduce the rule in full as Labour has published it (and I have no clue who actually wrote this version):

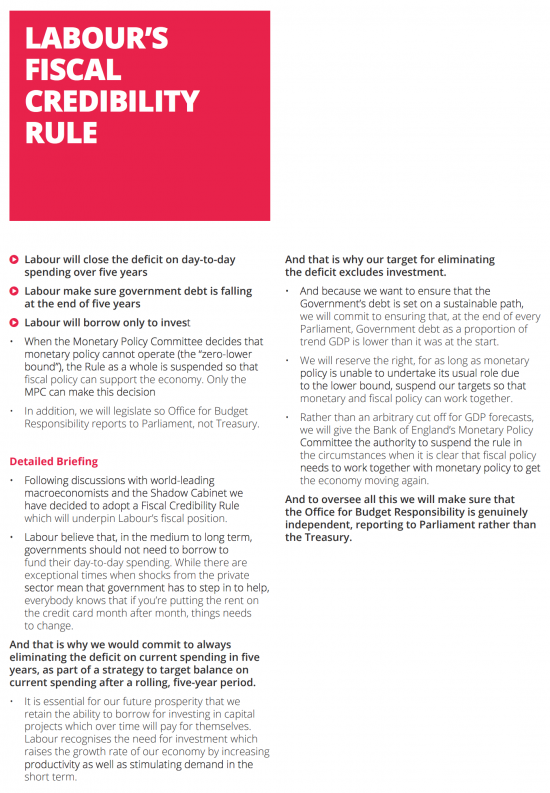

So, let me avoid doubt and reproduce the rule in full as Labour has published it (and I have no clue who actually wrote this version):

The defence is that the headlines are wrong, although they are highlighted, and are what it is clearly intended people read and understand.

Instead, we are meant to note that:

- If the Bank of England is so kind the rule can be suspended. In other words, the Bank and not the government is left in charge of economic policy, even when they have no hope of using monetary policy;

- The five years rule does not mean five years: it always means five years hence. In other words, this is a policy for 'never, never': Labour never has to balance the books because it always says it will do so in five years time. This reminds me of St Augustine's prayer that God make him chaste, but not yet. It's pure rhetorical nonsense, in other words if read in this way (as we are apparently meant to do). I am not a fan of disingenuous claims;

- And the reason why we must do this is that 'the credit card will be maxed out' if Labour does not do so. Or to put it kindly, the household analogy for macro is adopted in its entirety and the fallacy of composition that it embraces is accepted, lock, stock and barrel;

- Despite this debt will always be falling as a part of GDP, but how is not explained;

- And borrowing for investment is outside this book balancing exercise, except it clearly is not because total debt has to fall in proportion to GDP, meaning that in all likelihood a current surplus has to be run: after all, how else might this be guaranteed?

I accept the criticism that I, at least, did not read the full horror of the rule into what I wrote. That's because I could not believe that the accredited authors really meant it to be as bad as it is.

But apparently they do.

So I point out that it is much worse when read literally and in full than if just the headlines are noted as a summary of the whole.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

I have been following this across multiple sites. I am stunned that this document uses the credit card analogy. I had to download the document to fully convince myself that it was so (I am a party member).

Sad 🙁

Is it possible Labour’s New Keynesian fiscal rule policy is not a “nutter job” but a “neuter job” in that it’s an attempt to neuter the automatic stabiliser? What I mean by this is it possible by not imposing a fiscal collar on capital spend there can be so much of it the taxation from increased demand will substantially reduce the current spend gap? Will this result in the average voter having so much increased income and consequently well-being he or she won’t give a monkey’s what year the government actually balances its current spend books if ever?

That takes some getting the head round time

@ Richard

“That takes some getting the head around time.”

Yep. We just don’t have the data on how colossal the Labour Party’s capital spend will be and the apportionment over a five year period. The backlog of demand created by the previous Labour government and this current Tory one for affordable housing alone will be huge and I’ve no idea what bridges and highways back log for both maintenance/repair and new construction will be. Obviously Donald Trump and the Republican Party didn’t care what capital and current fiscal collar they broke with additional military spending and tax reduction programmes. It will be interesting to see how inflation fares in the USA although noticeably the Chinese have manouevred the value of their currency down in response to Trump’s tariffs. Since a great many of the manufactures bought in the United States are made in China the currency manipulation may help to contain any inflation from the fiscal easing. This obviously doesn’t help any making America or Britain great again programme since indigenous manufactures will still be under the cosh on price point from Chinese imports. Maybe quotas will be switched to and all the hassle involved in monitoring those.

@ Richard

Guardian reports today in an article there are 1.2 million people on the social housing waiting list and perhaps there would be more on the list if people thought the wait would be shorter than the several years it can take to be made an offer:-

https://www.theguardian.com/commentisfree/2018/aug/14/tories-houses-build-landlord-crisis-league-tables

Conclusion there’s a big capital spend in the waiting on social housing alone if you’ll excuse the no laughing matter pun!

Agreed

A new Green New Deal report is coming….

Richard and Schofield,

I can’t find it now and am a bit busy but Neil Wilson did some analysis on Labour’s fiscal rule a year or so ago that’s worth looking up on his blog (or old blog).

I forget the detail but I think he was saying that when you work through the various aspects of the rule it may well lead to extremely excessive infrastructure spending (read white elephants) while much of what we actually need (more salaried teachers, nurses, doctors, police etc.) remain in short supply due to the current budget rule. Potentially the rule forces an unnecessarily unbalaced approach to government spending that’s likely to backfire on Labour in particular and the left in general.

If I have time I will look it up and post a link tomorrow…

http://www.taxresearch.org.uk/Blog/2016/08/04/john-ncdonnells-fiscal-rule-a-final-note/

The link to Neil’s old blog is broken but I think the text is copied in full in Bob’s posts BTL on this old one of yours Richard. Maybe Neil moved the origin to his new blog on Medium but I can’t locate it.

I had forgotten that one….

@ Adam Sawyer

“I forget the detail but I think he was saying that when you work through the various aspects of the rule it may well lead to extremely excessive infrastructure spending (read white elephants) while much of what we actually need (more salaried teachers, nurses, doctors, police etc.) remain in short supply due to the current budget rule.”

Well fair point which is where I originally started out with my comment on one of Richard’s previous articles on this “fiscal rule” subject. I said why bother capital spending on things like schools and hospitals when you can’t afford to staff them except what I now realise is the angels and devils are in the detailed analysis. So, for example, teachers’ salaries are for the most part local state current spend raised from local revenue. Central government also gives local government permission to borrow to fund capital development. Corbyn might change this arrangement to accord with the USA autonomy way as pointed out by Greg Palast. This would mean increased local state tax revenue on the multiplier basis. Here’s the Greg Palast argument:-

“…the US does not have a single currency, at least not in the Maastricht sense. We have at least 50 currencies. Each state, every little burg and hamlet, has its own tax and employment policy. That’s what saved the US economy from Mundellian Reaganomics. What Reagan took away in federal funds, states and cities restored. Recently, in my village outside New York, the fire department decided we needed a new fire house. The citizenry voted to issue bonds on Wall Street and tax ourselves to cover the debt. We didn’t need Washington’s approval. Neither the state nor the Almighty (Alan Greenspan) could stop us.”

http://www.gregpalast.com/currency-rules-but-its-not-ok/

Corbyn probably if he has any “MMT” sense will also raise the National Minimum Wage in order to cut back on government current spend on welfare top-ups to inadequate private and public sector wages. There are probably other arguments that won’t pop into my head as yet. But I think you can see what I’m saying which is MMT has the right arguments but has to be careful to apply its analytical tools to see what is really going on and what’s possible to actually make a New Keynesian revised fiscal rule actually work.

This Telegraph article shows the deficit down to roughly 5% of overall government spend:-

https://www.telegraph.co.uk/business/2018/03/01/back-black-uk-current-budget-surplus-imf-says-osborne-right/

If we’re worrying as MMTer’s where the net financial asset savings are going to come from then it’s possible to see that Corbyn’s increased additional capital spend proposal of £70 billion is going to nearly double that current £40 billion deficit gap and the other policy options I’ve outlined could considerably add to that.

Finally, the “white elephants” argument. Are we to really take Neil Wilson seriously on his throw-away comment? Neil sounds very right-wing in his comment when there are 1.2 million on the social housing list and probably more who aren’t signed up because of the ludicrously long waiting period. Then there’s transportation infrastructure, repair, replacement and addition. Then there’s the whole “Green Initiative” ranging from energy saving measures to Green energy creation schemes. I’ve no idea where the education and healthcare capital spending programme stands, replacing out-dated buildings or refurbishing and extending them or indeed new buildings simply to accommodate population growth. Last I heard about Neil Wilson he was promoting the JG programme and how do you break that down by classification is it all current spend or a large part capital? Again it’s in the detail!

Sure this arbitrary breaking down of government spending into current and capital spend is a nonsense but it’s possible to take the New Keynesian “fiscal rule” approach as “pragmatic Keynes” given the high level of monetary system illiteracy in the UK. Here is Keynes saying in regard to Lerner’s Functional Finance that in order to convince UK treasury mandarins he’ll have to convince their children first and they’ll then convince their parents:-

http://cat.middlebury.edu/~colander/articles/was_keynes_keynesian.pdf

Richard Murphy told us recently that problem still exists nearly 75 years later:-

http://www.taxresearch.org.uk/Blog/2018/07/25/the-treasury-admit-that-tax-does-not-fund-government-spending-as-modern-monetary-theory-suggests/

Schofield,

Yeah I see what you’re saying. I previously believed/hoped the Labour Leadership essentially was viewing the economy through a MMT lens but had to jump through all kinds of mainstream hoops simply to up their chances of being elected. I believed once they won they’d adopt a greatly expanded functional finance approach where they subtly aborted austerity in a way that the mainstream couldn’t shoot down.

Now I am really doubtful that they are being that smart. I’ve heard from plenty of people with links to people close to the leadership who say that the shadow chancellor (at least) is ignorant of MMT. This latest stuff from his economic advisers doesn’t bode well either.

Maybe I’m wrong to doubt them, I don’t know. I suppose the point for me is that a well functioning democracy requires those standing for office to clearly explain their planned policies in language the electorate can understand. That either isn’t happening or Labour don’t get MMT. Either way it’s discouraging.

Nevertheless, I’ll keep my fingers crossed your perception is accurate.

On the debt to GDP ratio–is this not simply a constraint requiring that investment be of a sufficient quality, with large enough multipliers and returns to investment both public and private, that the debt to GDP ratio doesn’t fall.

By back of envelope calculations seem to suggest that this should be attainable given most reasonable projects. More broadly, isn’t this also a pretty reasonable objective at least over some time horizon? Would you advocate a permanently rising ratio?

Why is it that important?

I need to know why it really matters when debt servicing costs are negative in real terms and very likely to stay that way

1)

Given current interest rates as you outline and the huge opportunities for public investment this constraint will not be an issue for any but the whitest of elephants–and stopping them is probably a good thing to keep politicians’ vanity in check.

2)

Also if the debt to GDP ratio in question is looking at PSND then the fact it’s net debt means that investment spending will not cause issues as the capital accumulated cancels the gross new debt.

3)

If we accept that there is some argument to be had about desirable levels of debt – or at the very least that there are many who want to have this argument – then it is worth noting that saying your policy profile puts downward pressure on the debt to GDP ratio is a sufficient (but by no means necessary) way of satisfying critics in this area. Of course there are many other ways of winning this argument but they are all I would argue considerably more complex. Every minute of airtime you have to spend explaining why even when debt to gdp is rising the debt burden is not an issue is a minute less where you can make the positive case of what you can do with this investment and growth potential. And if you accept that adopting this position doesn’t limit the positive potential of fiscal policy then it must be worth choosing the path of simplest sufficient justification for your policy.

Check this out again:

“When the Monetary Policy Committee decides that monetary policy cannot operate ( the “zero lower bound”), the Rule as a whole is suspended so that fiscal policy can support the economy. Only the MPC can make this decision”

W – T – F?

Seriously? The BoE has been scraping along the surface of the zero lower bound for 10 years…

So, in other words, when the BOE can finally bring themselves to admit that then we will throw this nonsense “fiscal rule” in the bin where it belongs but first we need them to legitimise that decision, accept defeat and share the responsibility (?!).

And given that we are close to the zero lower bound one could almost surmise that this whole “fiscal rule” nonsense was effectively little more than a piece of theatre that was meant to appease and involve the establishment in a future shift to a fiscal policy regime – to create a premise and pretext for that .

But do we need that? I mean really? :”Only the MPC can make this decision”. So the monetary policy corpse must be alive until it declares itself to be dead?

I must admit that my suspicious mind is buzzing with questions and theories:

The BoE and most central banks will be still have rates that are close to zero when the next crisis strikes. It is obvious that they will have no room to cut rates substantially and therefore be useless in that situation – so, is there something psychologically and politically clever in getting the masters of monetary policy to declare their own irrelevance? Or was this idea just a prequisite (a formality) that was required to get agreement across the Labour Party?

Either way it appears to me that the fiscal rule could be a clever ruse that even its own creators may not be fully aware of.

If we stop for a second, clear our minds and look at this, we have a commitment that appears to put a whole lot of emphasis on fiscal rectitude – BUT all of that is wholly conditional on the idea that monetary policy is still viable and interest rates are not caught at “the zero lower bound”. But interest rates have been close to zero for a long time and and would only take one significant shock or crisis (or less) to ensure that “monetary policy cannot operate” and that “the Rule as a whole is suspended so that fiscal policy can support the economy.”

As for the periods in which monetary policy can operate (should they ever return), I can’t see Corbyn (or McDonnell) imposing austerity, so, the fiscal rule could also be used as a pretext for tax reform that targets the rich, the corporations, the tax havens etc…. using fiscal rectitude, rather than social justice alone, as the pretext for those initiatives.

In both cases this rule could use conservative principles as a basis to introduce progressive policies.

Personally, I can’t see why such a pretext would be needed nor do I see the necessity in getting the BoE to verify the extinction of monetary policy. But I can see the logic and why some might think it was cunning.

I may not be entirely right about this but, seriously, think about it.

I have

I am on your wavelength

I’ll say it again…………..

I hope that Labour are going with the flow with orthodoxy only for them to become more radical when they (if they) assume enough power in Parliament. There is an outside chance.

A slim outside chance.

Alright then…….a wafer thin outside chance.

BTW I watched Corbyn the other day dealing with Wreath Gate. The Channel 4 journalist ( a new red haired woman) was irritatingly bad but Corbyn just did not deal with it at all.

Corbyn lets them get to him. He bruises too easily.

You have to be tougher and braver than that to change Britain. I’m sorry………………………………

@ Marco Fante

“I must admit that my suspicious mind is buzzing with questions and theories.”

Don’t forget on the other side of the fence to your suspicious mind is a whole load of forelock tuggers who’ve been trained by the MSM to be super-suspicious of government who they believe at the drop of a hat will spend too much and cause Mega-Zimbabewean/Weimar Republic/Venezuelan hyperinflation. Having some independent technical agency who ought to know what they’re doing and have the power to jack up the Base Rate to defuse the hyper-inflation is so reassuring! Of course, the forelock tuggers have no idea the on/off hyper-inflation of house prices in the UK since the early 1970’s has anything whatsoever to do with the Bank of England technical experts along with heartless/corrupt Labour and Tory governments gutting the social housing construction programme!

Yes Schofield,

All of which ties in very neatly with the idea of getting the Monetary policy Committee to declare the death of monetary policy.

@ Marco Fante

“All of which ties in very neatly with the idea of getting the Monetary policy Committee to declare the death of monetary policy.”

I just see this New Keynesian Gang “Fiscal rule” policy as a sort of clunky half-way house MMT policy artfully crafted to be palatable to the great un-washed who have largely been reared on Daily Fail pap for decades! Why else, for example, would Jo Michell agree the UK government can create money in its own right for spending purposes:-

https://criticalfinance.org/2018/08/07/labours-economic-policy-is-not-neoliberal/comment-page-1/#comment-2209

@ Marco Fante

But interest rates have been close to zero for a long time and and would only take one significant shock or crisis (or less) to ensure that “monetary policy cannot operate” and that “the Rule as a whole is suspended so that fiscal policy can support the economy.”

Talking of shocks and interest rates:-

https://realmoney.thestreet.com/articles/10/19/2016/hey-volcker-thanks-nuthin

Could I unkindly suggest that all this is really tilting at windmills – the government rules, literally – surely?

http://www.progressivepulse.org/economics/how-money-really-works

You can….

Groupthink…”no one ever got fired for hiring IBM…. ”

Monetarism is dead but the establishment have nothing to replace it (that would benefit themselves) so it remains a corpse in the orthodox command chain which must be ritually bowed too…oh and don’t frighten the horses (i.e the media) with notions that its actually dead.

In the UK, every day gets more like Gormenghast.

A couple of hours ago, @PatriciaNPino pointed out the credit card guff in the Fiscal *Credibility* Rule to Jo Michell on Twitter.

His response – “That’s bad. I don’t know who wrote that. But it’s bad.”

I’m a little bit surprised – didn’t he read the thing he’s defending?

Good for her

And it makes clear that they have not read it

Well, in light of the above, we can all now understand what Liam Byrne’s allegedly jokey handover note about there being “no money left” was really about!

Put simply, he believed it was true, and that the Blair/Brown Governments really had “maxed out on the credit cards”!!!

I think that Labour and its coterie of advisors should be warmly applauded for turning an urban myth into a policy.

That takes some doing.

It’s as if they have accepted that the hoi polloi thinks that the earth is flat and then Labour thinks it has the job to produce the drawings to prove it.

Who is in charge here? Labour are playing to the crowd. It does not bode well……………………..

“Who is in charge here?”

Nobody.

@ Pilgrim

“It’s as if they have accepted that the hoi polloi thinks that the earth is flat and then Labour thinks it has the job to produce the drawings to prove it.”

Regret that having spoken to my MP, Ben Bradshaw (who I think is basically a decent individual, unpretentious and with minimal expenses – if too centrist for my personal taste).

I was amazed to be told that when I pointed out what the Treasury letter http://www.taxresearch.org.uk/Blog/2018/07/25/the-treasury-admit-that-tax-does-not-fund-government-spending-as-modern-monetary-theory-suggests/ implied, which he had after almost a year of trying, extracted from them, he just suggested “people would not believe they could have everything.”

This is someone who, as deputy chairman of the Health Select Committee has written a report on how social care in later life could be funded!

I cannot quite decide if this is simply a lack of ambition and poverty of aspiration or an acknowledgement of how difficult it is to change the narrative. As an ex journalist (and with a partner who is one too) perhaps he is just too ‘frit’.

It begins to suggest that the Labour Party is indeed working on the basis that the Tory roadmap must be followed, even if a different direction is taken.

And also of course that Labour is not nearly radical enough!

Sad, but true on all counts

Hello Peter

Hmm – sounds to me then that the likes of Bradshaw are treating the economy as a list of priorities – or a sort of triage.

The problem is that in the current economic set up, you cannot just tamper with one aspect of the dynamic without trying to deal with the others.

So Bradshaw’s (and therefore perhaps Labours’ ) aspirations are limited.

But then again – how is MMT promising people ‘everything’. And why is it OK for the rich to have everything then?

I mean what are the intellectual and cognitive terms of reference in Bradshaw’s statement?

Fuck me (sorry) – I thought MMT was about delivering fairness? Whatever happened to that as a concept!!!

AAAAAARRRRGGGHHH!!

Forgive me, perhaps I am missing something important; but I have no idea on what basis you expect anything of the Labour Party.

Better stick with the Tories then eh

Their rule is worse

Nobody is in charge: period.

Indeed.

With Labour (yet again) stupidly affirming the Gov = Houshold metaphor, that triggers worries about balancing the books.

Now I wonder what party stands by that goal above all others?

Well done Labour you just gifted the Tories countless votes on a golden platter.

So much muddied water:-

https://www.opendemocracy.net/neweconomics/labours-economic-policy-really-neoliberal/

The UK’s being held back by our politicians failing to act to clean up this water!

That’s a very poor article

@ Richard

“That’s a very poor article.”

Yes it is but very revealing of the confused thinking in the Labour Party hence my phrase “muddied waters” but think about the rest of the electorate who aren’t even Labour Party members!

Agreed

A completely stuffed up narrative, to be polite

You say it’s a poor article Richard (by Pete Green, who he?), but it hit me where it hurts. I’ve previously raised on this blog my fear of the Bond Vigilantes and the FX markets. Those of us with long memories remember with pain Denis Healey surrendering control of government policy to the IMF in return for a loan to bolster a subsiding sterling exchange rate – I see this as having been the start of the descent into Thatcherism and then neoliberalism.

I accept that things were different then – oil prices were a big issue – the article says today it will be food because of our declining self-sufficiency- but all I’ve really read in response to my (irrational?) fears is that any exchange rate effects will be short term and can be ridden out.

Makes me nervous and obviously does a lot of other people, and is a sharp weopon for the anti-MMT brigade. I’d like to see strong proposals for defence against these malign influences. Capital controls?

Give me time, but I hope others will wade in…

@ A. Pessimist

Should we be nervous of foreign exchange markets? Only if we have debts in foreign currencies.

What about a falling pound? Yes it makes oil more expensive but it also makes our exporters more competitive and as long as we have something to sell, foreigners will want to buy pounds. For multiple reasons, we should invest in UK based sustainable energy such that we are future proofed from fluctuations in the oil price. We should also be investing in UK farming, along with health and education. Take care of the basics and the exchange rate will be fine.

@ A. Pessimist

MMT economists are more than well aware of exchange rate depreciation (aka ‘pass through’ inflation), as Randy Wray explains here in a blog post “MMT AND EXTERNAL CONSTRAINTS”

http://neweconomicperspectives.org/2014/02/mmt-external-constraints.html

Thanks for the link Stephen, and the “common-sense approach” response Charles. I suspect that the fear of currency depreciation is much like the “government as a household” analogy – stories perpetuated by the media etc. to keep things from changing.

Nowadays there is ample explanation available as to why the latter is wrong but I find the complexities of international trade balances, international currency and bond markets etc. much more difficult to see through (e.g. see the comments following the article on that link) and the fear lingers!

Unfortunately this series of Richard’s blogs seems to show that both stories are currently considered to be true by Labour Party economic advisers. You would hope that they would be busy working up the policy options to minimise pass-through inflation, and I think I did read a while back about them “war-gaming” an attack on Sterling on Labour forming a government.

I checked in Denis Healey’s memoir “The Time of my Life” and he subsequently decided that he had been persuaded into the IMF loan unnecessarily by “the Treasury”.

He was very sure about that in late life

And Labour wants to maintain central bank independence and therefore authority to determine the workability of its New Keynesian fiscal rule when this agency is run by a bunch of bankers!

http://labour.org.uk/wp-content/uploads/2017/10/Fiscal-Credibility-Rule.pdf

https://www.theguardian.com/business/2018/aug/15/rbs-bankers-joked-about-destroying-the-us-housing-market

http://neweconomicperspectives.org/2018/08/bank-whistleblowers-united-told-doj-to-use-4506-t-as-kryptonite-v-banksters.html

Is the fuzzy distinction between capital and current spending not confusing the picture. Would a distinction between spending that brings economic returns and spending that doesn’t be more useful? Even through the MMT lens, if money creation drives an increase in demand that is not compensated by the production of goods and services that people will buy, the surplus will have to taxed or borrowed out of the economy to prevent inflation. In the context of a Job Guarantee for example, economic returns may be relatively short term (filling in holes in the road to make driving to work quicker), medium term (teachers’ salaries or building social housing) or long term (big infrastructure or replacing energy-intensive production methods with labour) – or zero (paying people to dig holes and fill them in again).

If this is true, does it suggests that there is some nugget of truth in the Labour Party position.

To the last, no….

To the former, I think we have been doing this for a long time

But I am happy to be reminded that we have

Peter Green (article above) cheap stuff on Richard Murphy. Nor even a good summary of proper full employment Keynesianism for Labour supporters, But has the one merit of going back to the start of this. How about we take the personnal stuff about Richard and Bill Mitchell out of this debate about what a proper Keynesian, Labour party can do after the failure of the Blairites ? Remember Peter, what the youngster in my northern city are begging for; Job contracts without the word, ‘zero hours’ in, and tenacy agreement without a 6 month notice to quit clauses clipped in from day one.

I have a copy of Randall Wray’s MMT second edition in front of me. He draws no distinction, as far as I recall, between the Sovereign powers of the UK, Japan, et al and the USA. Wray argues, sure, we have to worry about being floating, fixed and pegged currency, and if we are a third world developing nation, our foreign reserves. But for the UK, China is most likely to accommodate a devalued £, if it wishes to sell us stuff for the next fifty years or so. So I think that those above, who are more concerned about our relationship with China and Germany, are moving in the right direction.

So if Jo Mitchell (now Peter Green) wants an olive branch from an MMT, Georgist, Corbyn, supporting Labour member, as academics, address Randall Wray’s, ‘MMT’ second edition in the correct manner and publish a paper showing that he fails to produce the necessary demarcation criterion between US monety/fiscal sovereign powers and UK monetry/sovereign powers. In short, show why Wray is misleading and wrong and why MMT is not general in this respect. I will be happy to accept such a demarcation between the states and thus limits to a Labour, full employment policy that this may entail – if, of course – you can produce one. But don’t just assert it like you are writing a fucking, Daily Mail opinion page. Look scary things…!

Jo Mitchell feel free to take your time on Wray, as it will be the most important 300 pages you will read outside of Henry George’s famous book so recently hinted in the Labour manifesto. God Jo….. I am assuming that LVT is still on with the party? Or has the Jesuit Order, economists cancalled that bit as well? Have they already told you LVT too would be ‘ad hoc’ to the mainstream corpus or some such trick?

Once again,

I don’t think that most of you folks are really seeing this:

““When the Monetary Policy Committee decides that monetary policy cannot operate ( the “zero lower bound”), the Rule as a whole is suspended so that fiscal policy can support the economy.”

1. You can virtually ignore the “Monetary Policy Committee decides” bit because interest rates have been close to the Zero Lower Bound for years. When a crisis or event occurs that would normally require a big rate cut, the BoE won’t have any choice but to admit that they are up against the ZLB. It would be numerically undeniable. Getting them to admit that would at best be a formality and at worst, a humiliation for them. Overall, the MPC ‘decision’ would be meaningless.

2. Given that we are close to the ZLB and another crisis is inevitable, what we have in this document is a deceptively dressed pretext for the introduction of a fiscal policy regime.

That’s effectively what it is whether you like the dressing or not.

I have said that

But in that case there is collective deception

My fear is that they are all deceiving themselves

And that makes it especially dangerous

That’s fair enough in a way, Richard.

I wasn’t really thinking about you when I wrote that. I was thinking about some of the commenters above that seemed to be habitually falling back on their old scripts without fully picking up on the gist of this.

Fair point too

Whether it is ‘clever’ or not, the good thing is that it does not spell out the alternative – they may eventually have to accept that the only alternative is JG and spend-first-tax-later.