It has been claimed in comments on this blog that notes and coin are debt free money.

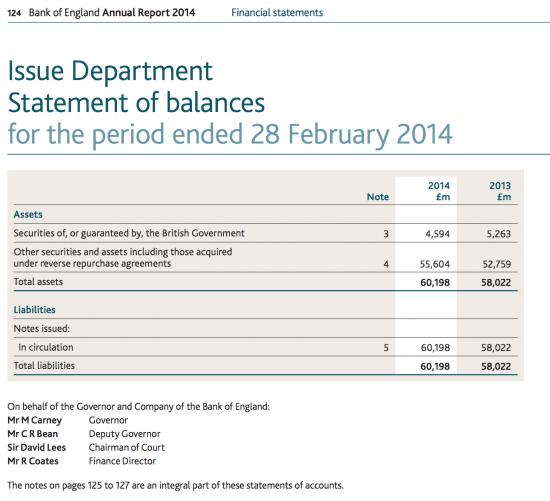

This is not true. The Bank of England accounts dealing with the Issue Department make this clear. This is its balance sheet:

The notes and coins in circulation are very definitely a liability of the Bank because they represent a debt owing.

Shall we put this idea of debt free money to bed?

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

A liability yes, but they are created debt free, minus costs for printing and minting, of debt.

They were not borrowed into existence. That means no debt to pay back, albeit, as you say, there is a liability.

Asset backed though, you’ll note

Yes- I think this distinction that groups like PM make (and debt free money was talked about by Gesell). As Richard points out, it’s all asset backed as per double entry bookkeeping, it’s just that the debate goes astray because PM and MMT are using languauge differently -frustrating really? I’m pretty sure that NOBODY is trying to say that money operates outside the debt/credit framework.

The treatment of notes issued in the Bank of England accounts and in broader macroeconomic statistics (including the System of National Accounts, and IMF Government Finance Statistics Manual and Public Sector Debt Guide) is interesting, and in my view flawed.

In the macro manuals, assets are divided into nonfinancial and financial assets. Nonfinancial assets, land buildings etc do not have matching liabilities, but financial assets generally having a matching liability. My mortgage is my bank’s asset, and my liability. Monetary Gold is an exception. It is only recorded as a financial asset. Historically, this made sense, as countries used the gold standard, so all other financial assets were ultimately a claim on the gold held by the relevant central bank. A mortgage loan asset could be converted into a deposit, which could be converted into a currency, and theoretically, converted into gold.

However, once the world left the gold standard, and all currencies became fiat currencies, the idea that notes and coins are the liability of the central bank looks odd – they are no longer convertible into gold or another “real” asset – instead, at best, the Bank of England would convert your bank note into a similar note or coins to the same value.

Currencies are therefore no longer “asset backed” in any way, and given this, for me they are “free money” and central banks are able to earn significant seignorage on this. The restriction on issuijng lots of free money comes not from the need for them to be asset backed, but for the very real constraints of inflationary effects, and floating exchange rates (i.e. you risk devaluing your currency). I’m strongly of the opinion that the international statistical manuals will conclude at some point that currency should be treated just like monetary gold, as a financial asset that has no matching liability.

Statistics geek sidenote – monetary gold is quite narrowly defined, and only includes “gold to which the monetary authorities (or others who are subject to the effective control of the monetary authorities) have title and is held as a reserve asset.” Nonmonetary gold, say that owned by Scrooge McDuck, or other private citizens, even in the form of bullion, is not even treated as a financial asset in macroeconomic statistics.

One last interesting footnote. In the UK, coins minted are not treated as a liability of the Bank of England, but as a liability of the government. These account for a further 4.3billion in 2013 (see UK Blue Book, table 5.2.9). In the European Union, the headline measure of government debt, Maastricht debt, is defined as general government gross debt in the form of currency and deposits, debt securities and loans. It excludes the liabilities of the Bank of England. This means that were the government to move responsibility for minting and issuing coins to the Bank, it could reduce its Maastricht debt. The impact today is pretty limited, given the massive scale of UK government debt, and the diminishing importance of cash, but historically it would have been more material for this EU wide debt measure.

Philip

The question is if notes are assets where does the credit go?

To a seignorage reserve?

Richard

Richard,

I’m not sure what you mean. When the a Central Bank prints banknotes, it incurs some cost. Banks purchase these notes from the Central Bank, the difference between the electronic deposits received (presumably mainly reductions in reserves held by the bank, i.e. reductions in BoE liabilities to the clearing banks) and the actual cost of printing the notes is pure profit for the Bank of England, available to be distributed to the government as a dividend – so yes, seignorage.

Essentially, in a fiat currency world, banks are able to print assets, and sell them for an asset with a matching liability (though I would guess, in practice, they tend to reduce their liabilities rather than increase their assets).

Note however that the Bank of England accounts, and macroecnomic statistics don’t behave like that at present, instead they consider the notes are a liability of the bank.

But as I say, under the gold standard, this made perfect sense. The Bank of England promised to pay the bearer on demand the equivalent of 5, 10, 50 pounds worth of gold. But in a fiat currency, its not convertible at all. You cannot exchange your bank notes for anything except (presumably) a very similar bank note.

So what is your alternative double entry to that which shows them as a liability now?

Where does the credit go?

Hi Richard,

sorry for the delay in replying. The best explanation / argument I can offer is to to think of a Central Bank with a fiat currency as owning a gold mine or oil well.

The owners of a gold mine or oil well are able to extract and use an asset that they have not created but that nonetheless have value. The market value of the gold or oil, minus the actual costs of getting the stuff out of the ground is their profit, and the stock of oil or gold before they sell it, is there asset – with no matching liabilty.

In macroeconomics, both gold (other than “monetary gold” and oil) are both treated as nonfinancial assets, and so only appear as assets.

Now a Central Bank is able to mine notes and coins, only it doesn’t mine them, it prints or mints them. Obviously the cost of doing this varies depending on the denomination of the notes and coins. But clearly a GBP10, 20 or 50 note costs nowhere near this to design, print and transport, meaning the excess of value over the cost of production is almost all profit. Any stock of banknotes held by the central bank can be thought of as akin to nonfinancial assets or monetary gold, an asset with no matching liability.

In economic statistics, the value associated with the notes and coins comes into existence via what national accountants would call an “other economic flow” – though under the current recording rules, the matching transaction is an increase in the Central Bank’s liabilities. As noted above, the current rules don’t really make sense in a world of fiat currencies.

So the current rules would record the printing of bank notes as firstly, an incurrence of liabilities by the central bank matched by an increase in the banks holdings of currency, (with no effect on the Banks net worth, in fact, probably a slight worsening, given it will have cost something to make the notes in the first place) followed by a reduction in holdings of currency and probably a decrease in deposit liabilities to commercial banks.

Under my proposal, which is logical when notes aren’t convertible, the incurrence of liabilities is replaced by an other economic flow, meaning printing bank notes and selling them improves the net worth of the central bank. They are indeed, free money – albeit you cannot take this too far due to the external factors of inflation and devaluation.

But where is the credit?

Please answer the question

As a matter of fact there has to be one and you will not say where it is

You cannot have a Dr alone

Philip,

You say “Currencies are therefore no longer “asset backed” in any way”.

But fiat currencies are backed – by fiat tax!

The government won’t accept anything else in payment for tax but its own currency. Gold for example won’t do, they want their own money only.

And if you refuse, they give you a special invite to spend a few nights at one of HM prisons.

Stephen,

I agree that currencies are given value by government’s requiring them as taxes, but this has nothing to do with the macroeconomic statistical / accounting conventions I’m talking about.

I personally tend to view hard currency as an interest free loan, albeit that you have to ignore the cost of producing it.

Maybe it is more accurate to call cash “interest free” rather than debt free? Regarding liability, as with the national debt which will never be paid back, isn’t the liability on cash a technical liability? After all, the government isn’t likely to default on its cash liability as it can always just print more. The commonwealth bank effectively held as liability all the resources and assets of Australia.

Can a debt that is probably never going to be called in be properly called a debt?

I suspect interest free is right

And a debt that is interest free and never to be called in is money…

Like QE is money

Indeed – the way we use language is key to understanding/distorting our view of the way things work. It’s a gift to politicians that words can be so easily misunderstood -Osborne is having a field day with this!

I agree that notes and coin are not debt free, and sit on the BoE’s balance sheet.

But doesn’t this, by the same reasoning, mean that your claims that Green QE could provide debt free money are wrong?

Any money printed, or bonds bought through Green QE would sit on the BoE’s balance sheet much as the current QE does, and could not be cancelled as you have suggested.

GIQE is not debt free – it is created by debt

But it’s not repayable and no interest is due

In QE the BoE buys bonds which sit on the asset side of their balance sheet, in exchange for cash which then sits as a liability.

In your version of Green QE, what happens when these bonds mature? Are you saying they simply disappear from the balance sheet? By saying that these Green QE bonds are not repayable and carry no interest, you are also saying that they are essentially worthless – and the asset/liability balance sheet of the BoE won’t balance. Indeed, the BoE would be bankrupt.

You are also directly contradicting the statement in the article above, that notes and coin are NOT debt free money, by saying Green QE (which is essentially about creating more notes and coin to spend on assets) somehow IS debt free.

The bonds would either not mature (technically possible) or would simply be replaced with new bonds

Remember – the bonds in question are issued wholly within the organisation – a technical necessity

It is not debt free – it is like debt between a husband and wife who only have a joint bank account – making payment makes no difference to the money in the accopunt

I am making a guess here and would welcome any input or corrections.

The Bank of England used to be a private company, and so the treasury would issue a bond to the BoE for it to issue notes and coins. That would be an asset to the bank and a liability to the government. Since 1844 on the BoE would have this monopoly as commercial banks were forbidden by Peels Bank Charter Act from creating notes.

The BoE would then sell the cash to the commercial banks. When the bank was private, this may have been a profit to the BoE.

I am making another guess here – Clement Attlee’s government nationalised the BoE. So the profit on cash then went to the treasury. So the BoEs asset is also the treasury’s asset, but the balance sheet still shows the traditional asset to the bank.

Yes

I have argued consolidated accounting would on this occasion make things much clearer

Maastricht/ Lisbon don’t allow this relationship to happen -everything has to go through secondary markets this is presumably why we need ‘accounting tricks’ like QE.

Yes

I highly recommend anthropologist David Graeber’s fantastic BBC R4 series “Promises, Promises: A History of Debt”. It aired in March, but is still available on BBC I-Player…

http://www.bbc.co.uk/programmes/b054zdp6

Especially pertinent to this discussion is Episode 3, “The Origin of Money”

(Is not ‘heavy’ and is only 15 minutes long)

xplores the ways debt has shaped society over 5,000 years e

Thanks

Worth listening again

Well, there are lots of different types of liabilities, aren’t there. Or perhaps it’s easier to think of liabilities as having different maturities. And one of the special things about this type of central bank liability is that they decrease in value with age because of inflation.

For example, there will be some millions (perhaps more) of pounds worth of liabilities there which are represented by pre-war white fivers. These things are still technically on the books as liabilities, but in practice are worth multiples of their face value on the collectors’ market. So they are assets in a way. If you found one in your grandad’s effects and took it to the BoE for a current note (which is your right), they’d sell it for, perhaps £100, to a collector. And if the world ever does become so messed up that people, en masse, want to hand those in to the BoE in return for the freshly-printed fiver they will give you in return, then we really have bigger things to worry about than central banknote issues being central bank liabilities.

Likewise, those banknotes are only ever one vote in parliament away from being declared worthless and replaced with, dunno, the New Anglian Peso, or whatever. Again, should the world be in such a state that that was likely, firstly the market would have already priced it in, and secondly we would have far more serious things to worry about.

You really only have two choices with the note issue. It’s either a fiat (or one legislature vote from fiat – cf. depression-era USA) central bank issue or a private issue, of which there aren’t any left that I am aware of (the few remaining private issues today, like in Scotland or Hong Kong are, in practice, by law, backed by government central bank issues). If you go for a private issue then now and again a bank will go under and trash the value of its notes but not all of them (England a long time ago). If you go for a government issue, you will get fewer overt trashings but each trashing will trash the value of all notes (Zimbabwe).

So yes, printed notes are liabilities, but when the liability is to be redeemed solely by another note then the central bank is solvent and liquid so long as it can afford paper and ink. Because central banks are special. They have liabilities, but only those in other currencies are a potential problem. They can book humungous profits (SNB for the last 3 years) or humungous losses (SNB this year) and no one really cares. It doesn’t matter, as long as their money is still carrying out its function – of being something people are prepared to accept in return for the goods and services they are selling.

Very good points, Bloke from Germany.

Worth noting too that a central bank is solvent and liquid as long as the manufacturers of paper, and the manufacturers of ink (assuming neither are produced by the bank itself) are willing to accept its currency.

Its all a confidence thing, and this, not the size of the balance sheet, nor the scale of central bank losses (though these clearly can impact on “confidence”) determine to what extent a central bank can simply print money.

Note also that actual notes and coins, as a percentage of GDP, vary considerably from country to country, depending on the extent to which countries have move to electronic transactions and cultural factors.

Philip,

Same point as I was making above. It is not “all a confidence thing”, fiat currency is ‘backed’ by the power of the law (which is just a nice way of dressing up what it is – namely brute force).

Regarding “impact on “confidence””, its laughable when the rating agencies ‘downgrade’ a soverign issuer of the currency (like they did with the UK) as such an entity can always pay its bills.

Consequently the BoE cannot suffer “losses”.