HM Revenue & Customs have published this year's tax gap report.

If anything these reports get more ludicrous by the year. The methodology - much of which relies on ignoring the fact that tax evaders do not submit tax returns or file their company accounts with HMRC or Companies House - continues to be absurd. I have taken it apart before, here, and don't propose to do so again now.

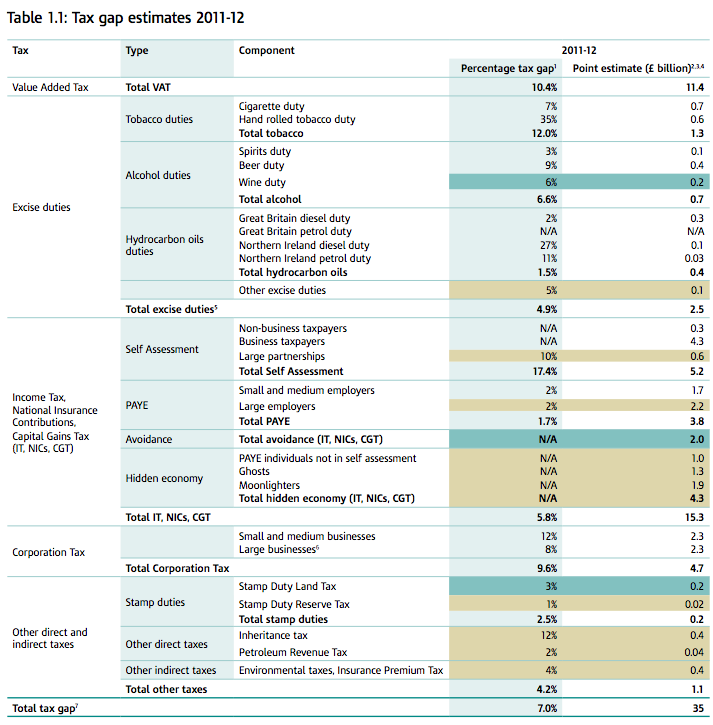

Instead let me just highlight some of the absurd anomalies in this year's report that I have noted so far. Let's take corporate tax avoidance for a start. According to HMRC in 2011-12, they year to which this report relates UK tax avoidance in that year was just £4 billion and was split down as follows:

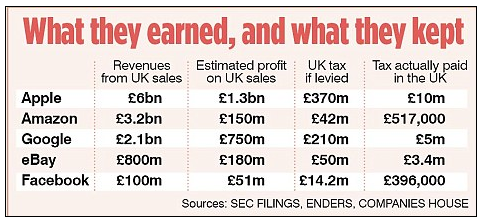

Now this report in the Mail on Sunday in April 2012 - covering the same year as a result - gave an estimate (and in my opinion a fair one) of the tax avoidance of just a few giant tech companies:

That's, as they note, £685 million lost to five companies. Microsoft and Yahoo are not in there. And there are, we know, plenty more playing such tricks. But apparently the total lost is just £1.5 billion.

Actually, that's because none of these losses to tech companies is in HMRC's figures. They may have been in David Cameron's sight lines when attacking tax avoidance but HMRC refuses top recognise they do anything wrong. And that's ludicrous.

And then let's look at NIC. There is no figure given in the report for a separate NIC loss that I can find. When it comes to NIC avoidance they say:

But the payment of dividends to the owners of small companies in lieu of salaries in the contracting trade is by far the biggest loss to NIC avoidance there is: that's all such arrangements are designed to deliver and successful challenges under IR35 still happen, albeit rarely. This is a scheme.

I estimated long ago that the annual loss to such abuse was at least £1.2 billion and the number of companies now suing such schemes has grown considerably since I did so in 2007. The loss must be much higher now. But it is nowhere in the calculations. the word dividends is not mentioned once in the report.

I could offer another example. When it comes to evasion these classic comments on methodology are made:

Let's be candid: this just means they made the numbers up. But there is data on the size of the shadow economy: I used it in my work on the EU tax gap which is now the basis of the official EU estimate on this issue. The UK shadow economy is estimated to be 12.5%. HMRC reckon the cost of the loss to the shadow economy is £3.2 billion - suggesting the economic activity in the shadow economy at an overall tax rate of 38% might be £8.4 billion or 0.5% of the UK economy. If I generously added in their crime figure to that on top of the moonlighters and ghosts the total loss would still be only £7.9 billion - implying shadow activity of £21 billion or 1.3% of the UK economy. To be polite this is pure fantasy.

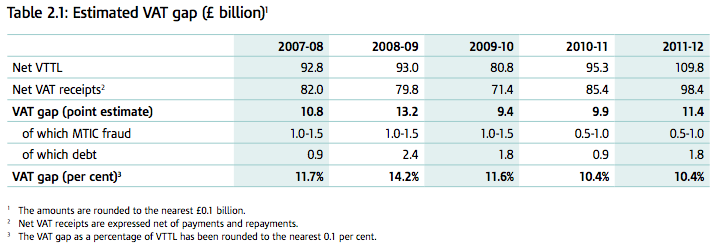

And finally, for now, let's look at VAT. It's important to remember some history here. The VAT rate was 17.5% for many years to 1 December 2008 when it dropped to 15% and stayed there until 31 December 2009 when it went back to 17.5% only to be raised again in January 2011 when it went to 20%. The implication of a higher rate is obvious: more VAT will be lost. Each pound put in the pocket costs HMRC more. But this is the estimate of the overall VAT gap:

As HMRC say:

![]()

This point is fair, but the implication is bizarre. When the incentive to evade VAT increased considerably because of the increased rate in 2010-11 and 2011-12 the compliance rate went up. Now I am grateful for what might be seen as an official rebuttal of any Laffer type effect but candidly I do not think that is in the remotest but plausible, especially given the massive decline in the number of VAT inspections which I think is far more likely to explain this loss. This data is just not credible.

There is however one overall piece of data on VAT which may approximate to credibility. This is the average VAT loss from 2005 to 2012:

The average loss? That's 12.2%. And that average loss for VAT remains remarkably close to the size of what I think the UK shadow economy might be at 12.5%. I do not think that a coincidence.

So, let's take HMRC's absurd totals for all losses to be right bar the shadow economy and crime, which total £7.9 billion and we are left as this table shows with an overall loss of about £27 billion form avoidance, mistakes and so on. That's far too low for reasons noted above, but let's not quibble for now. This is HMRC's estimate of errors and avoidance in the system.

Now let's take GDP as £1,581 billion, as it was when last I looked, and use an overall tax rate of 38% on that, based on budget data, and take an overall shadow economy rate of 12.2% (and yes I know VAT does not apply to everything, but the sample is big enough to justify the extrapolation across all economic activity) and then the loss to evasion comes to £73 billion.

Now what have I always said the losses to be? £25 billion to avoidance and £70 billion to evasion or £95 billion in all ignoring tax paid late.

And what does this combined total come to? Well, £100 billion.

That's a might big difference from HMRC. But it's a lot more credible than their work of fiction and guess work.

I stick by my numbers, and suspect they're now seriously understated.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

The problem is in the definition and terms.

Tax avoidance is legal, Tax evasion is illegal.

Estimation of avoidance is easier than evasion due to DOTAS and other initiatives.

Estimation of evasion is more speculative

It’s a bit like talking about the benefits problem and blaming the youth unemployed, it suits their arguments.

I think we all agree that more effort should be put in to ensuring that (i) tax due to be paid is paid, and (ii) that where necessary legislation is changed to reduce avoidance.

I have dealt with those issues in my piece

GDP is the value of produced goods and services. Corporation tax is tax on *profit* and VAT is tax on value *added*. You therefore cannot multiply GDP by 38% and get a sensible result. In principle I suppose you could look at what the black economy consists of, make rough estimates of profitability/added value and then do the calculation. Query how practicable this would be – HMRC doesn’t try but that’s not to say it couldn’t be done.

That said, the UK has one of the smallest black economies in the world. It may be optimistic of us to expect we can seriously reduce it. There are easier targets – some of which are mentioned above, but I’d add undeclared offshore bank accounts into the mix (and the fact they represent years, perhaps decades, of undeclared income means they are rich pickings indeed).

Your logic has micro but not macro sense

38% of the economy is paid in tax

I am looking at the untaxed element of the whole economy

It can be argued 38% would be different if this part were taxed but if it were that overall is what it would yield in a variety of taxes – not particular taxes – which is why such an estimate makes total sense

“the UK has one of the smallest black economies in the world.”

How do you know?

The data from Friedrich Schneider I used in my EU work

RM -I could add some areas of avoidance you have not even thought about. I may be wrong but my growing concern is that you are spreading yourself too thinly over too many campaigns.I wish you would concentrate on the area of taxation more because this is your area of most expertise, and is how all Public services should be financed in my opinion. I think that there needs to be root and branch reform of HMRC with independent oversight, especially in this area of the Estimate of the Tax Gap. HMRC should not be Judge and Jury on its own performance.

In my day job I almost only do tax

And country-by-country reporting

What do I drop?

Richard

That logic would be correct if the black/shadow economy were representative of the rest of the economy; however every indication is that it is typically small scale, comprised of individual traders and small busineses whose effective tax rate (were they subject to tax in the usual way) would be significantly lower than the average. One could in principle do an analysis on the macro rather micro level but again, I’m not aware of this having been done. And of course whether the analysis is macro or micro the end result must (if the analysis is correct) be the same.

The overriding point, however, is that the size of the black/shadow economy in the UK is small by European and international standards, and that suggests there is limited scope for reducing it further.

That’s just an excuse for continuing crime

Where else do we say such things?

“That’s just an excuse for continuing crime

Where else do we say such things?”

Absolutely everywhere.

Drunk driving is illegal and quite possibly immoral as well. Yet we do not breathalise each and every driver every time they drive in order to stop it.

We accept, perhaps even with a heavy heart, that the efforts to truly reduce incidence of a crime to nothing are not worth it. Perhaps in financial terms, perhaps in terms of freedom or liberty or even just the opportunity costs.

The same is true of every single crime. We might not particularly like the fact that we do this but a fact it is. We acept that there will always be some continuing crime because we know that the costs of entirely abolishing it are not worth it.

But was have a heavy heart

That is not true on tax crime

And that is the difference

On that one you show no sign of such feelings

And that’s the point you deliberately miss

Where I work 10 years ago we had 30 of us in VAT inspection – today there are 15- of whom 10 are newly trained inexperienced former direct tax staff, so is it any surprise that VAT leakage is so high, in the past with reasonable staffing levels businesses could expect a VAT inspection every 3 years or so which had a deterrent effect, but with staff cuts of 50% what do you expect ?

OK I don’t know how you allocate your time. My perception is that you are veering off into Left Wing Economics which is perfectly all right if you like that sort of thing, but I would rather you go for specific objectives. My objective is reform of HMRC. For starters just look at the comment from Anon HMRC Officer above.

We have one of, and maybe now, the longest Tax Codes in the world. Nobody I repeat nobody understands it in its entirety. It is criminally under policed. HMRC is underfunded, underskilled, underled and trapped in inflexible IT systems. Its leadership is entirely in hoc to a bunch of amateurs ( I do not exaggerate) at the Treasury.

In this type of environment for example Country by County Reporting, which I fully support, will be useless without proper policing. It is gesture taxation politics without enforcement. Auditors can’t audit without trusting Management, and as Management pay Auditors I would not put much hope of enforcement here.

And we also need to get at the heart of the problem, which is inadequate taxation expertise in tax policy formulation and lack of Parliamentary time and scrutiny.

And most MPs lack of taxation knowledge is almost laughable.

On the last we entirely agree

In fact we agree on a lot

And by this time next year microsoft will have ended support for windows XP…..which hmrc will continue to use albeit with a 50-million browser emulation package…what fun.

It starts is Parliament of course but I do think that radical reform is needed to HMRC. Tax is a people business; HMRC’s IT systems are based on a flawed Top Down approach and prevent action that even HMRC want to implement.In fact they have to perform manual work arounds for certain procedures. I believe their current systems are largely based on an old Management Consultancy fad of Business Re- Engineering (some of which now discredited) which thought stripping out people and replacing with IT was the answer to everything.

I think you are right

That was the 2005 model