The following piece comes from the The EREP network Review of the UK Economy in 2015. It is by Jo Michell who is a senior lecturer in economics at the University of the West of England:

In his 2015 Autumn Statement, Chancellor George Osborne gave a bravura performance. He congratulated himself on record growth and employment, falling public debt, surging business investment and a narrowing trade deficit. He announced projections of continuous growth and falling public debt over the next parliament.

While much of this was a straightforward misrepresentation of the facts -- capital investment has yet to recover from the 2008 crisis and the current account deficit continues to widen -- other sound bites came courtesy of the Office for Budget Responsibility. The OBR delivered the Chancellor an early Christmas present in the form of a set of revised projections showing better-than-expected public finances over the next five years.

When, previously, the OBR inconveniently delivered negative revisions, the Chancellor responded by pushing back the date he claims he will achieve a budget surplus. In response to the OBR's gift, however, he chose instead to spend the windfall. This is a risky strategy because any negative shock to the economy means he will miss his current fiscal targets -- targets he has already missed repeatedly since coming to office.

As it turns out, these negative shocks have materialised rather quickly. Since the Chancellor made his statement a month ago, UK GDP growth has been revised down, the trade deficit has widened and estimates of borrowing for the current year have increased.

In reality, the OBR projections never looked plausible. The UK's current account deficit -- the amount borrowed each year from the rest of the world -- is at an all- time high of around 5% of GDP. Every six months for the last three years, the OBR forecast that the deficit would start to close within a year; every time they were proved wrong. Their current assertion -- that the trend will be broken in 2016 and the deficit will steadily narrow to around 2% of GDP in 2020 -- must be taken with a large pinch of salt.

The current account deficit measures the combined overseas borrowing of the UK public and private sectors. In the unlikely event that George Osborne was to achieve his stated aim of a budget surplus, the whole of this foreign borrowing would be accounted for by the private sector. This is exactly what the OBR is projecting. Specifically, they predict that the household sector will run a deficit of around 2% per year for the next five years. They note that “this persistent and relatively large household deficit would be unprecedented”.

This projection has been the basis of recent stories in the press which have declared that the Chancellor has set the economy on a path to almost-certain financial meltdown within the current parliament. This is too simplistic an analysis. Financial imbalances can persist for a long time. The last UK financial crisis originated not in the US UK lending markets but in UK banks' exposure to overseas lending.

But the Chancellor's strategy entails serious financial risks. Even though there is no real chance of achieving a surplus by 2020, further cuts to government spending will squeeze spending out of the economy, placing ever more of the burden on household consumption spending to maintain growth.

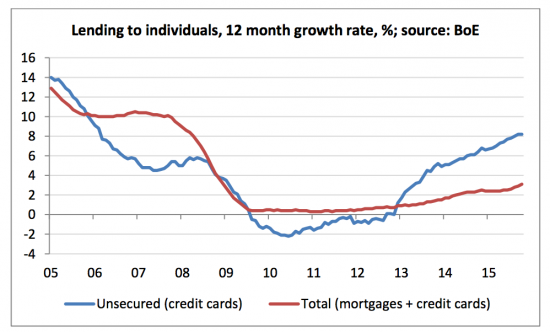

The figure below shows the annual growth in lending to households. While total credit growth remains subdued, unsecured lending has, in the words of Andy Haldane, chief economist at the Bank of England, been “picking up at a rate of knots”.

Moderate growth in the mortgage market may conceal deeper problems: household debtto-income ratios have fallen since the crisis but, at around 140% of GDP, remain high both in historical terms and compared to other advanced nations. The majority of new mortgage lending since 2008 has been to buy-to-let landlords. These speculative buyers now face the prospect of rising interest rates and tax changes that will take a large chunk out of their property income. Many non-buy-to-let borrowers are badly exposed: a sixth of mortgage debt is held by those who have less than £200 a month left after spending on essentials.

The Financial Policy Committee has noted that these trends “… could pose direct risks to the resilience of the UK banking system, and indirect risks via its impact on economic stability”. What is often left out of the more apocalyptic visions of a coming credit meltdown is that underlying all this is an unprecedented housing crisis in which an entire generation are locked out of home ownership Instead of tackling this crisis, Osborne is using the housing market as a casino in the hope of keeping economic growth on track during another five years of austerity. It is a high-risk strategy. His luck may soon run out.

NB: A fully annotated version of this piece is available here.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Headsup in Norfolk: http://www.theregister.co.uk/2015/12/30/solar_storm_northern_lights_in_california/

http://www.aurora-service.eu/aurora-forecast/

The phrase ‘bravura performance’ is a term of art and I should use it more often.

Meanwhile, we should ask: “Who is applauding?” and perhaps ask why.

Above all, we should ask: “Who gains?”

Without that, all our criticisms are mere handwaving: if we criticise his excuses and his showmanship, instead of his agenda, we are ineffective and we might as well join in with the applause.

The really scary thing is how under-reported this infomation is in the main-stream media. Osborne has been steering us into this situation with very little opposition and the tories still seem to control the narrative. Even on their own (misguided) terms, they are failing.

I think the term “Money Fascism” about sums it up. A widespread refusal amongst the “fat cats”, main stream media chums and an unquestioning majority of the electorate to face reality in the name of misguided self-interest.

Probably one of the most important issues of our time is “The unquestioning majority of the electorate” in my opinion.

And don’t forget this: https://www.opendemocracy.net/uk/kirsten-downer/osbornes-fire-sale-must-be-stopped.

It’s like the homeowner boasting about how warm his house is when others are feeling the chill, only to learn that he’s been chopping up the furniture to put on the fire! A simplistic but accurate enough analogy.

Hey, it’s New Year’s Eve so we need to be positive. I fear the UK progressive movement has become overly concerned with cursing the darkness – albeit the pervading gloom is depressing. So, in 2016 it’s time to light ever more candles – and form tangible links with other progressives in other countries.

As always thanks to Richard for keeping the flame burning. Let’s hope that 2016 will be a year to remember for the right reasons. Shift happens!

Best wishes to you all – wherever you are.

And to you

“Financial imbalances can persist for a long time”

I suspect the unholy trinity of housing/stagnant wages/consumer borrowing could carry on for some time -the financial system will be celebrating hard tonight (expensive champagne and the finest lines of coke, no doubt).

Still, Andrew Dickie mentioned Gramsci’s Optimism of the will in the face of intellectual despair-I’ll (Non-alcoholically) drink to that!

“The current account deficit measures the combined overseas borrowing of the UK public and private sectors.”

Richard, considering today’s ‘globalised’ world where corporations keep moving themselves around, how accurate is the data on overseas borrowing of the private sector anyway?

Reasonably accurate

You can also argue it is to some degree meaningless

But only to some degree

“So this global binge of QE has caused inflation, a lot of it, but not consumer price inflation. It has caused rampant asset price inflation”

http://wolfstreet.com/2015/12/27/i-was-asked-whatever-happened-to-inflation-after-all-this-money-printing/

And……the next global problem emerges…….

http://www.zerohedge.com/news/2016-01-02/500000-170-million-few-months-next-subprime-trade-emerges

Making money out of losing money…..