Following on from my demonstrating that Alastair Darling provided the framework for People's Quantitative Easing in 2009 here's another letter on the subject I've just unearthed thanks to my conversation with Danny Blanchflower today:

Now a lot of this repeats already made in my last blog:

Now a lot of this repeats already made in my last blog:

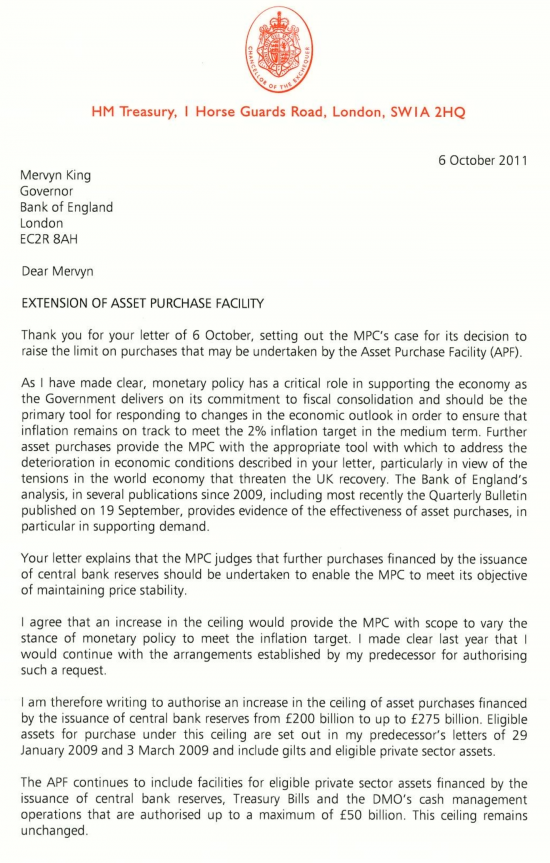

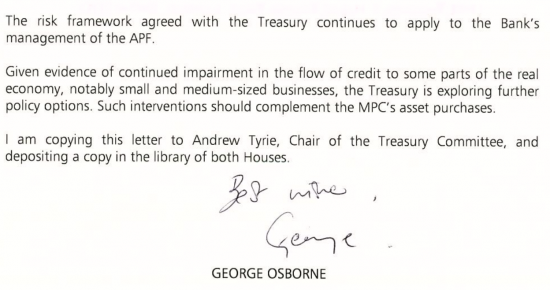

- The fiction of Bank of England independence is blown apart by this letter: Osborne decided on more QE, and the amount;

- Osborne said it would work in 2011: it's very hard to see what has changed now given that we still have 'tensions in the world economy that threaten the UK recovery'.

But, more important is the sting in the tail:

So, first the framework created by Alastair Darling that clearly permits People's Quantitative Easing remains in place.

And, second, Osborne and the Treasury were very obviously considering a small company intervention, and other options, in 2011. Something rather like People's QE looks to have been on the cards back then. But now Osborne denies it.

Why is that?

And why isn't People's Quantitative Easing on the agenda now when it would make complete economic sense to do it?

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Maybe time to remind ourselves of Keynes’ famous quote?

“The ideas of economists and political philosophers, both when they are right and when they are wrong are more powerful than is commonly understood. Indeed, the world is ruled by little else. Practical men, who believe themselves to be quite exempt from any intellectual influences, are usually slaves of some defunct economist.”

― John Maynard Keynes

Osborne’s reference to “the real economy” in an official communication like this one is interesting and it plays right into your argument.

The key difference between this part of the recent QE and your proposal, is that he sought to channel his real economy assistance through the banks and financial markets (the not-so-real economy).

In any case it would appear that you have accumulated the precedents and evidence necessary to support your claims regarding legality and the facade of central bank independence.

Beyond that, I think that there is something larger and more historic that is being played out in all of this. Initially, it began with the post-GFC QE programs, both in the UK and elsewhere. The first QE was actually in 1932. One key difference with the recent lot is that central banks were allowed to purchase (‘invest’ in) non-treasury assets.

Your proposal is a logical (arguably inevitable?) development which recognises that monetary and fiscal policy are no longer separate. The revelations in these letters adds to an existing body of evidence which reveals that the union of monetary & fiscal policy isn’t merely a proposal. It has already happened in effect, if not officially.

QE in 1932:

https://research.stlouisfed.org/publications/es/10/ES1017.pdf