The Guardian reports this morning that:

Gordon Brown dealt a blow to Labour's economic credibility by wrongly giving the impression in his final year as prime minister that the party failed to understand the importance of tackling Britain's unprecedented peacetime budget deficit, the shadow business secretary, Chuka Umunna, has suggested.

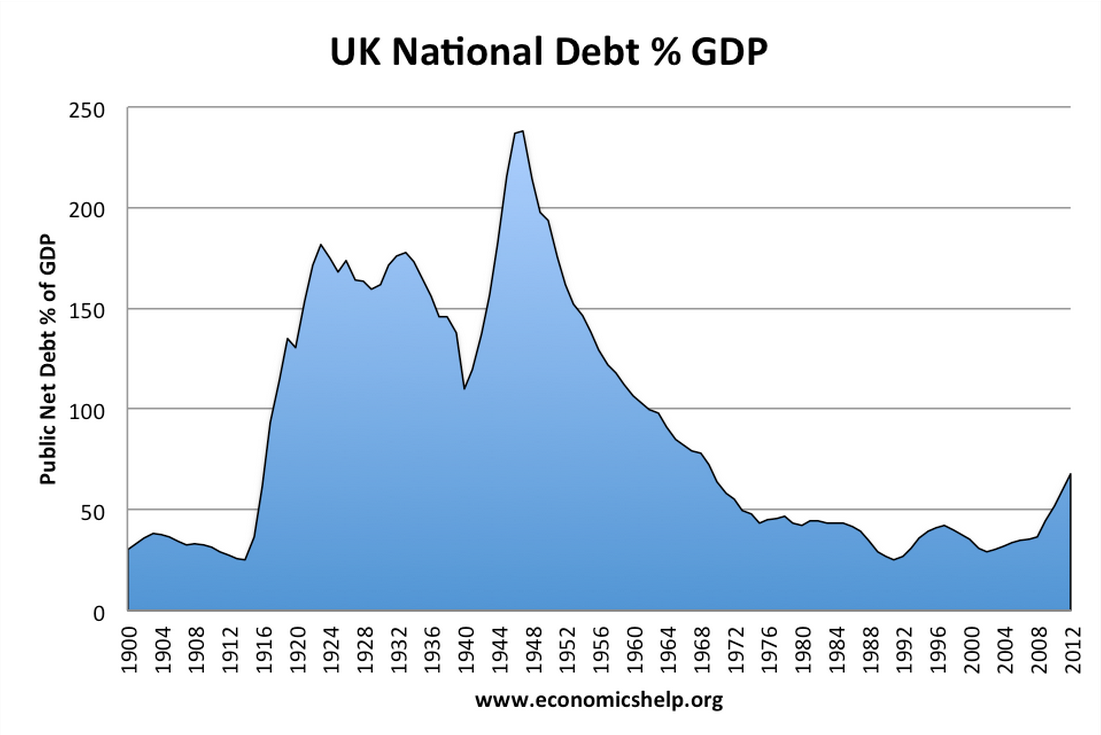

How many things can you get wrong in a sentence? This is UK public debt as a proportion of GDP since 1900:

From 1919 until 1970 peacetime debt was higher than now (and the above data fails to take QE into account). The claim that there is unprecedented UK peacetime debt is wrong.

And I wonder, what would Chuka have done here:

The source is HM Treasury Budgets.

In 2008 would Chuka have said let's abandon all automatic stabilisers and leave people on the streets?

Would he have abandoned the banks and let the economy fail overnight?

Would he have refused to take action to ward off recession - as happened?

And would he have said spending must be cut because GDP fell - compounding the economic cycle?

If not, what is he saying?

And how and why does he think in his period tackling debt was the priority (if it ever should be)?

I think it's a fair question to ask because I cannot work out what this is about in which case it is fair to think others might not as well.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Umunna is talking about the budget deficit, not the national debt (one is a per annum figure, one is an absolute amount). They are two different things, though admittedly many people use the terms interchangeably (probably because many people don’t understand the difference).

The charts at this website – http://www.economicshelp.org/blog/5922/economics/uk-budget-deficit-2/ – suggest that he may have a point: note the fourth chart down, headed “UK Government net borrowing – % of GDP”. This shows net borrowing as a percentage of GDP (a fair proxy for the deficit) peaking in 2009-10, which was Brown’s las year as PM.

GDP fell

Of course the ratio increased

But the real issue is that no government can cut its way to reducing the deficit. That is a technical impossibility if everyone else in he economy insists on saving – which is encouraged by by government cuts. There is no way out of this inescapable fact

I think Brown may have known that – and if he did he was amongst the few

Chuka does not and that I find deeply worrying

Chuka, like Brown, knows perfectly well. But he also wants to toe the Party and Treasury line on austerity. Miliband understands the economics too, but has never really come to terms with his father’s critique of Parliamentary Socialism I fear.

“How many things can you get wrong in one sentence?”

A lot, it seems.

“From 1919 until 1970 peacetime debt was higher than now (and the above data fails to take QE into account). The claim that there is unprecedented UK peacetime debt is wrong.”

Apart from simply ignoring World War 2, you do realise wartime debt doesn’t suddenly disappear when the war stops, don’t you? During the two wars defence spending hit over 50% of GDP alone, pushing total government spending over 100% of GDP. In rough terms each war added about 125% to the debt/GDP number.

Under Labour, pre-crisis the UK had about 40% debt/GDP. We are now around the 90% mark. So it’s the biggest peacetime increase in the debt/GDP ratio, and the biggest ever peacetime budget deficit.

This analysis ignores these things

a) Inflation

b) Deficits in peace time

c) QE reducing debt now

d) The 40% debt ratio was exceptionally low

e) That it was not choice to create this deficit

f) That this did not happen here alone

To put it anothre way; it’s crass and selective analysis

a) no, debt/GDP is inflation adjusted.

b) not sure how an analysis of peacetime debt/GDP ignores an analysis of peacetime deficits. The 2009/10 budget deficit was a record peacetime deficit.

c) QE doesn’t reduce debt. Only outright monetisation does that. Eventually the cash injected into the system via QE bond purchases gets reversed as the bonds mature – which is what is happening in the US as bonds are maturing faster than new QE purchases.

d) 40% wasn’t exceptionally low. Not sure where you get that from.

e) Choice no, hubris yes. Labour chose to run deficits in times of good growth, resulting in a large structural deficit – believing that there would be no more boom and bust.

f) Indeed, it was a global recession. Why though did the UK end up with by far the worst budget deficit in the western world?

What I don’t understand is how you can simply say something as obviously wrong as you have and try and defend it! Debt/GDP was higher during 1919-1970 but that was wartime debt, the last of which was paid off in 2006. Since then our debt/GDP levels have once again exploded, and it has nothing to do with war.

“But the real issue is that no government can cut its way to reducing the deficit.”

Yet you don’t have to go very far to find many examples. The UK from 1997-2001, or more recently under the Coalition (where total government spending has fallen as a % of GDP, and also in real terms, CPI adjusted, yet the budget deficit has also fallen) or further afield you can look at Canada or New Zealand in the 90’s, or even the US at the moment.

Your answers a to d add nothing

Re e there is no evidence of a structural deficit – such things are just myths made up by those who think governments may not 1) borrow to pay for infrastructure 2) intervene in the economy for the benefit of those they represent c) seek to create social change

Re f – it was because of financialisation. Would you close the City? Tell us, please

And as for your final comments: the UK did not cut its way to reducing a deficit in 1997

And as for your suggestion that the UK has achieved this goal now….shall we treat that as your joke?

I see we have moved on from your initial claim, and now you are just blustering away like an old steam train. Comparing the debt/GDP ratio was have now with post war Britain was pretty silly.

I think you had better check your facts when it comes to structural deficits. They certainly aren’t myths. It’s the budget deficit adjusted to remove the cylical nature of the economy.

Other countries have large finacial sectors and it was well known before the crisis that the UK had a large one. Why then, as I asked before, did the UK end up with a budget deficit so much worse than it’s peers?

“And as for your final comments: the UK did not cut its way to reducing a deficit in 1997”

“And as for your suggestion that the UK has achieved this goal now….shall we treat that as your joke?”

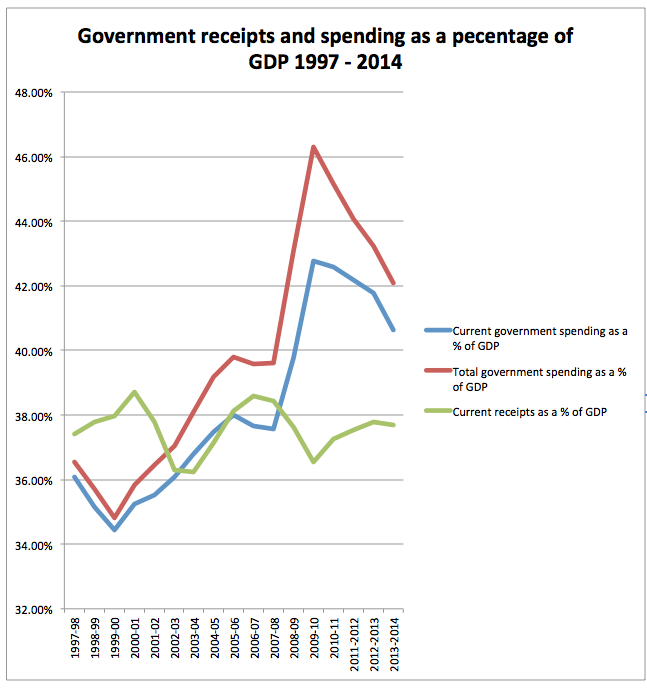

Let’s just treat these comments together. Total government spending as a % of GDP:

http://www.ukpublicspending.co.uk/spending_chart_1986_2016UKp_14c1li111mcn_F0t

You can see that both 1997-2001 and since 2011 it has fallen.

http://news.bbc.co.uk/2/hi/business/8636701.stm

http://www.economicshelp.org/blog/5922/economics/uk-budget-deficit-2/

Oh look! The budget deficit was also falling (from 1993-2001) and also from 2010.

So in short, yes, you can cut spending whilst also cutting the budget deficit. Which is the “goal” I was talking about. The one you state is impossible.

Aren’t you always going on about the nasty coalition’s spending cuts? Surely you must also know, being an economics expert, that the budget deficit is somehow being cut at the same time? And the UK economy is growing at a fair old lick despite those cuts? You read the FT don’t you?

You can cut spending and the deficit but only if others change their behaviour as a result e.g. They borrow or GDP rises or the trade deficit changes

Simply cutting alone can never achieve that result

And the fact is that right now – as I have said – UK households and business are not play9ing ball to make this possible and nor is the trade deficit and so cuts simply can’t reduce the deficit without reducing GDP at best

But what the heck, why worry about macroeconomics?

Why worry about macroeconomics indeed? It doesn’t seem high on your list of priorities – don’t you often say it’s all wrong anyway?

I agree with you that private sector borrowing is also declining, so I won’t post a link to another chart here.

As I have already posted, government borrowing and the budget deficit is also decreasing.

We can quickly deal with the trade balance/current account deficit:

http://www.economicshelp.org/blog/5776/trade/uk-balance-of-payments/

That’s money flowing out of the country, so the wrong way around for the purposes of your argument.

Which leaves GDP:

http://www.ons.gov.uk/ons/rel/naa2/second-estimate-of-gdp/q2-2014/stb-second-estimate-of-gdp-q2-2014.html

As we can see, GDP is growing very nicely at the moment.

So, to go back to your premise:

“And the fact is that right now — as I have said — UK households and business are not play9ing ball to make this possible and nor is the trade deficit and so cuts simply can’t reduce the deficit without reducing GDP at best”

Yet this seems to be exactly what is happening! It rather puts paid to the myth that you can’t cut and reduce a budget deficit at the same time without harming growth – something the IMF had to apologise for rather recently.

Actually, you’ve got trade wrong for this argument

And GDP is hardly increasing nicely – it’s small, unreliable and not benefiting most

Sorry: but you are wholly missing the point in terms of macroeconomics

You’re offering at best a micro analysis, as usual

Further debate on these terms is pointless

“Actually, you’ve got trade wrong for this argument”

Annual trade deficits are immediate and indirect reducers of their nations’ GDPs. So I think I’ve got this one right.

“And GDP is hardly increasing nicely — it’s small, unreliable and not benefiting most”

It was 3.2% at the last reading, and one of the highest in the developed world. It’s been accelerating since 2012. How good does GDP growth have to be before you acknowledge it is actually good?

I’m not sure how I am missing the point of macroeconomics, or focusing on the micro. The data is showing good growth, falling government spending yet falling budget deficits. I can’t see any micro there.

You have stated that this situation is impossible, yet the real world is telling us that it isn’t. You have then simply refused to debate the point.

Could it be that you don’t really understand why? Or that you don’t like having people point out rather basic errors you have made? Or is it because it doesn’t fit into the political narrative you are beholden too – that cuts are bad and budget deficits should be encouraged?

I’m really not sure, but I am pretty sure you should spend a little time sanity checking some of your posts before you press the button.

I’ve made no basic error

I am saying you can’t cut your way to closing a deficit

The reality is so long as we have a trade deficit (so many comes into the UK from overseas depositors if exchange rates are broadly stable as they now are) and high savings and low business investment then as a matter of fact the government will run a deficit

That is what is happening now.

This is a basic macroeconomic accounting equation. If I’m wrong, where?

“I’ve made no basic error”

I can point out a few, but ignoring real world data is the first one I’d mention.

“I am saying you can’t cut your way to closing a deficit”

The UK is doing that precisely as we speak. Other countries have also done the same thing. Some have also failed to do so, but that doesn’t make it impossible.

Since 2010:

The budget deficit has fallen from over 11% to under 6%

GDP has grown, and the growth has accelerated

Government spending has been cut in real terms

The trade balance has been negative, which is a drag on GDP

Private sector borrowing has declined.

In your macroeconomic world, the above is impossible. Problem is, we have real world data to show it is. I’m sure an economist of your calibre can easily explain why this is so, rather than dismissing the observable as impossible?

You are excluding key variables from your considerations

I asked you a key economic question

You have ignored it

Please enlighten me. What variables have I ommitted, and what is the question you are asking me? I’ll endeavour to answer it as best I can if I have somehow “ignored” it.

It looks to me though that you are ignoring the reality of the situation though – that reality is flat out contradicting your statement.

The basic equation is the identity that holds between consumer spending, business investment, movements in trade balances and government spending

OK, without writing a PhD thesis here I will attempt to answer your question.

“The basic equation is the identity that holds between consumer spending, business investment, movements in trade balances and government spending”

Typically in classical macroeconomics (which I was under the impression you though was all wrong, but now seem to be relying on) economies are treated as semi-closed systems. By this I mean that the system is modelled as a closed system with a single external input – the trade balance/current account.

It’s a simplistic model, and usually holds fairly well – but not always.

For a government to reduce it’s buget deficit, it needs more revenue, normally achieved through GDP growth (let’s exclude taxation from this debate – it is essentially off topic and regardless has a negative correlation to GDP).

As you say, GDP growth can come from a variety of sources:

Consumer Spending

Business Investment

Trade balance/Foreign direct investment

Government spending

Let’s deal with the easy ones first. Government spending is falling (cuts) and the trade balance is in deficit, which is classically a drag on GDP growth.

Consumer spending is actually increasing slowly, but net private sector borrowing is falling (business investment + consumer borrowing) and the saving rate has increased a little – so it’s not private sector borrowing that is displacing government borrowing as the driver of GDP.

So we find ourselves in a situation where GDP growth is good and has been accelerating, yet the factors that should drive it are falling, along with the budget deficit. Seemingly an impossible situation – definatively so in statements you have made.

So how is this happening? Again without going into a thesis I would suggest a few points.

Firstly, you need to look at fiscal multipliers. Classically these are deemed to be greater than 1 for government spending.

However, this is looking more and more like a false assumption. The IMF (amongst others) have recently come out with a paper suggesting that fiscal multipliers in open countries with floating exchange rate regimes often tend towards zero, and especially so as the debt burden increases.

I wouldn’t argue that all government spending is wasteful, has a fiscal multiplier of less than 1 or even could be treated homogenously but clearly it can be the case. Look at Japan for example – endless government spending hasn’t achieved growth, and with free floating fx the money can simply flow into asset bubbles or directly offshore.

So it looks likely that some cuts to government spending can be achieved with little or no pain to an economy. Not only that, but as these economic resources get redeployed elsewhere in the economy the multiplier ends up being increased.

I think this is what is going on in the UK, in simplistic fashion. Cuts are having little negative impact on GDP growth, and are being more than offset by the slack in the Labour market being taken up – leading to a net higher fiscal multiplier. The data shows us the unemployment rate is falling fast, and that the nominal number of workers is at an all time high. This hasn’t translated into wage growth yet as labour market slack still remains, but this does dramatically affect GDP multipliers and likely government revenues.

Other factors also surely help. A population increasing faster than CPI tends to have a positive affect on GDP growth. Relaxation of pension fund rules is likely to as well, and reform of the labour and benefits systems will also likely be positive for the economy. Low interest rates haven’t hurt either, nor has CPI coming down slightly.

Ultimately though, it is not impossible for a country to grow whilst cutting spending. It’s not a closed system, the money supply is not fixed and GDP at the end of the day is a value added term – not an absolute one.

The real world example we see in the UK at the moment, as well as other countries in the past and present, puts paid to the idea that it is impossible to cut a budget deficit whilst cutting government spending without something else taking up the slack.

I’ll come back to you: at last you have provided an intelligible if wrong response

Why wrong? Well, let’s start with the fact that the IMF think they have seriously underestimated multipliers and you say the exact opposite

And you are ignoring financial flows. But as I say, that will be for later. There is other stuff to do right now

Poor old Tony Robertson. Not so much waving as drowning.

The deficit is growing again Tony. Have you not noticed?

And all the “reduction” in the deficit can be pinpointed to the coalition’s foolish decision to cut investment.

That led to the three years of stagnation under Osborne and inevtibale double dip recession you’ve tiptoed around.

GDP was growing nicely between 2009-10. Then Osborne happened to the economy and consequently it looks impossible to get the deficit down. He’ll borrow £200bn more than the hubristic 2010 forecasts said he would. All that extra borrowing is quite clearly borrowing for failure.

And we’ve seen recent economic data start to point to a slowing down of the economy, just at the wrong moment for the Tories, as the spurt from Help to Buy runs out. There is no rebalancing, services now account for 80pc of output, high value job creation is weak, productivity has collapsed.

All your assertions on economics are untrue. You need to read around a bit more.

@ Richard

You should read the IMF/NBER’s new (2013) paper. In some cases they do indeed think they’ve underestimated the multiplier. In other cases they think they have dramatically overestimated it – specifically for open economies with floating exchange rates and larger debt burdens.

They also state that they think the mulitpliers are larger in general earlier in a recession and decline over time. They also mention tax cuts – some have >1 mulitpliers and some less than 1.

Regardless, the point is not that multipliers exist – it’s that they can be less than one. Which means that ever more government spending has diminishing returns. The observable data is also proving that you can have growth and cut a deficit whilst reducing spending – which is something the IMF had to make a rather humbling apology over recently. That was the point of this whole argument I beleive.

I am not ignoring financial flows – the current account balance is negative which means the sum of financial flows is net out of the country, which is a negative for GDP.

@ BenM

The budget deficit isn’t growing. Indeed it has fallen (though not as fast as planned) every year since it peaked at the end of 2009.

The cut in investement and spending was simply not big enough to reduce the deficit as much as it has been reduced. We are talking a roughly 1% cut in real terms spending, but the deficit has fallen just under 6%.

What double dip recession? The UK never went into one.

What recent data is showing the economy slowing? The most recent data points to the economy accelerating. 3.2% YoY GDP growth is one of the best in the developed world.

Before my calling my economic assertions untrue, maybe you should check your facts first.

I’d suggest that’s pretty selective reading

But we’ll differ on that

And the deficit looks as though it is increasing at present

much of that increase was due to the bank bail out plus the fall in revenues due to the great recession.

Gordon’s mistake in 2009 wasn’t not talking about cuts – it was that he started talking about cuts about 3 months before the election and ended up backing the Tory-lite “Darling Plan” and looking like a total idiot. He should have fought the 2010 election saying no cuts (except for a few obvious lunacies like Trident replacement, Titan prisons, ID cards) – and promised to reduce the deficit using QE and tax increases on the rich. I think if he’d done that he might well have won (not totally sure about that mind you becuase he was SUCH a bad campaigner… all a bit of a disaster really).

It’s a shame about Chuka because I started out liking him but he’s obviously being lined up as a Tony Blair clone to replace Ed and hence the endless briefings from the guardian’s hard right Blairite political editor, Nick Watt. I’m not buying the Guardian again until they get rid of Watt because he’s worse than the Daily Mail people in many ways. At least they’re honest right wingers.

The Daring plan was crazy: a law decreeing a fixed cut in the budget deficit was almost as bizarre as one declaring the world was flat might have been.

Nobody with any sense believed Darling just as no one with any sense believes the world is flat.

The idea that prior to 2008 Brown was running a profligate government whose financial incompetence was responsible for the banking collapse and the subsequent great recession is a prime example of a ‘Zombie Idea’ which no matter how many times it gets squashed just keeps on being re animated again and again. You can blame Brown for lots of other things but not that

The argument often made here that Richard is some sort of maverick outlier in thinking that we should have boosted demand and substantialy increased infrastructure investment is just nonsense, its mainstream macroeconomics.

A mainstrem macroecomics as Krugman frequently points out has held up pretty well since 2008. The problem is the politicians even ones aledgedly on the centre left are just not listening as Mr Umunna demonstrates all too well.

Alan

It is obvious macroeconomics but you have to remember that such things are beyond most economist’s understanding.

The Bank of England had to say also all economics text books had got money wrong earlier this year – and in fact that what they said was the inverse of what was needed

The same could be true for deficit reduction and the interaction of cuts and the deficit. One day someone will say it. But not yet, I fear.

It

Cutting the deficit is a cover story for rolling back the state and preventing government from creating money. The City want this privilege to themselves because it is a continuous stream of rent for them.

While government creates money by running a deficit, it trickles into peoples pockets through direct wages and benefits, or by indirect means in services and health, and as used to be the case grants for businesses and tax breaks for training and employing people.

This lessens the need for borrowing and debt. I believe this is why the City lobby government to cut back, it encourages borrowing.

Chuka is worrying (I believe), because he is not just showing a lack of understanding, but maybe having swallowed some City propaganda.

Having said all this however, I believe in what Lord Adair Turner and Martin Wolf have said, that in addition to deficit spending, we should create helicopter money, or overt monetary finance, and do what Steve Keen suggested, make people pay their debts with it. It is private debt that is killing the economy and causing poverty, not public debt.

https://www.google.co.uk/search?q=graph+of+private+debt+uk&espv=2&tbm=isch&imgil=c3sNoDpuNzRygM%253A%253BFpmTjlm4PKLhDM%253Bhttp%25253A%25252F%25252Fmakewealthhistory.org%25252F2012%25252F01%25252F10%25252Fbritains-debt-problem-its-not-the-government%25252F&source=iu&fir=c3sNoDpuNzRygM%253A%252CFpmTjlm4PKLhDM%252C_&usg=__0F8azb9Xuo4CkbB4pbl4WhlLpO8%3D&sa=X&ei=or0EVN6xA-220QXm-4HQDQ&ved=0CCkQ9QEwAw&biw=1022&bih=498#facrc=_&imgdii=_&imgrc=c3sNoDpuNzRygM%253A%3BFpmTjlm4PKLhDM%3Bhttp%253A%252F%252Fmakewealthhistory.files.wordpress.com%252F2012%252F01%252Fbritains-debts.png%3Bhttp%253A%252F%252Fmakewealthhistory.org%252F2012%252F01%252F10%252Fbritains-debt-problem-its-not-the-government%252F%3B467%3B393

The debt is not down – borrowing is up and continues to rise. There is apparently record employment (stop laughing at the back there) but spending is at rock bottom.

So where is this apparent growth coming from? As said before, a clue comes from the £1.4 trillion in household debt.

If there is no real investment and there are billions of pounds of cuts to the public sector, jobs are lost, the government loses tax revenue and then has to pay out benefits to the jobless. If cuts to public spending continue and there continues to be little or no investment, GDP shrinks and the only way to balance the books is to cut public spending again, but this just leads to a falling GDP again, meaning that the only way to balance the books is to borrow.

This is the lesson taught by Keynes and why the Great Depression in Britain lasted so long. Spending cuts crippled investment and this contributed to a deflation death spiral that only world war II got us out of.

Europe is gradually catching onto the fact that spending cuts only make recessions worse, not better. It is junk economics!

@ Steve0!!

You do understand the difference between a deficit and the national debt don’t you? I’ve been say the deficit has been falling. Whilst there is still a deficit the nominal amount of debt will still be rising.

The deficit looks like it is increasing right now

But let’s not worry about details

Er, yes. The deficit is the gap between what the government gets in taxes and what it has to spend on public services and the like.

Cutting the deficit by cutting spending does not work. If there is no corresponding growth, GDP will shrink and more borrowing will be needed to balance the books.

It is impossible to get rid of public debt and create growth by cutting spending. It always has been.

You got it

@ Richard

No, the deficit is still decreasing. It has been since the peak at the end of 2009. Check Eurostat if you don’t believe me.

@ SteveO!

“Cutting the deficit by cutting spending does not work. If there is no corresponding growth, GDP will shrink and more borrowing will be needed to balance the books.

It is impossible to get rid of public debt and create growth by cutting spending. It always has been.”

I see you haven’t bothered to read my earlier posts. Spending is being cut, the deficit is falling and yet we still have excellent growth. You and Richard say this is impossible – yet its happening in the real world as we speak! What does that say about your and Richard’s claims to the contrary?

The deficit is currently rising: tax revenues are falling this year

Looks like election bookeeping at the moment.

A large portion of the reduction in deficit seems to have been due to increased stamp duty.

Wage stagnation continues. Inflation continues (which is good for gov debt).

Working benefits continue to rise, seemingly outstripping not-working benefits.

Pension credit continues to rise, albeit slower now (no word yet on winter benefits).

It is certainly the oddest recovery, not only for this economy but also when compared to other countries.

Productivity continues to stagnate: Very worrying for an economic recovery.

How long it can continue to recover in the face of high imports, low exports, and poor productivity is a question.

I have to assume some creative can-kicking is being started. Whose boot will be kicking it after the election is something else to think about!

My question is: why, if the economy is recovering, the government is still cutting billions from public spending?

The boom in house prices is what is largely propping up this economy.

Ideology aline explains cuts now

“I see you haven’t bothered to read my earlier posts. Spending is being cut, the deficit is falling and yet we still have excellent growth. You and Richard say this is impossible — yet its happening in the real world as we speak! What does that say about your and Richard’s claims to the contrary?”

That you are grossly exaggerating the size of the recovery. Bogus self-employment, zero-hours contracts and temporary jobs count as an “excellent” recovery now, does it?

And what a curious recovery it is; Spending is at rock bottom due to wages being held down, there is little to no investment and manufacturing output is falling. What is driving this blip? Could it be credit fuelled due to a government-created housing bubble? Probably yes!

More people are having to use food banks, tens of billions are being cut from public spending, with much more to come, yet we have an economy of robust health, apparently. Despite Mr. Osbourne’s claims that he is cutting borrowing, it continues to rise.

After world war I, there were huge cutbacks in order to cut the war debt. The economy bombed and didn’t fully recover until world war II. After world war II, instead of cutting back, war spending was kept up in peacetime, the debt over 250% of GDP, in fact. This led to one of the biggest booms in our history.

Until the early 1960s, The debt to GDP ratio never fell below 100%. There is so much rubbish talked about the national debt. The ConDems claimed we would be in serious crisis unless we cut the debt. That is false. The only reason the debt rose in the first place was sue to the government bailing out the banks. They claimed that no one would be willing to roll over our national debt. As the finance sector relies heavily on government gilts, I doubt that very much.

As I have mentioned several times before (and I am going to mention it again) the national debt is never paid back, has never been paid back and indeed can’t be paid back. The debt is rolled over each time by issuing more bonds. Taxpayers only pay the interest on that debt.

The government is lying when it says it can’t afford a fiscal stimulus because we are too heavily in debt. We can afford it easily. Interest rates are on the floor at the moment, so there would be no problem paying back the interest on that debt.

Of course, pointing to the allegedly high public debt provides a fig leaf for the government to roll back the state; selling off large chunks of the NHS, cutting pensions and benefits and closing vital public services.

As for the “recovery”, and at the risk of repeating myself again, wait until interest rates start to rise.

POOF! 🙂

Poof indeed

You may in fact be a little too generous

You do seem able to generate an interesting exchange of views within the economics spectrum, Richard and it does help us all see a broader picture.

The link below does of course refer to the US economy but the same principles apply equally here. Can we persuade BoE and the Treasury to try it?

http://www.alternet.org/economy/why-fed-must-act-now-get-money-hands-ordinary-americans?paging=off¤t_page=1#bookmark

A Green New Deal would help do that