The indications are that the world is beginning to understand the complete and utter economic mess that will be the lasting legacy of 2026.

Trump and Netanyahu might have created conflict for personal gain, but its cost for everyone else is going to be considerable.

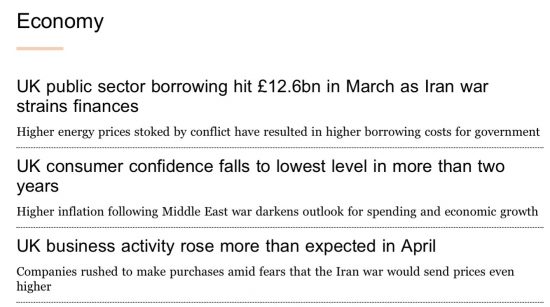

These adjacent headlines were in an FT newsletter this morning:

What they suggest is that this war is having an almost inevitable reaction on both consumer and business behaviour, with both moving downwards as a result, with the consequence being seen in the state sector through the automatic balancing process required by the sectoral balances (the linked glossary entry explains that these are, if you are unfamiliar with them).

If consumers spend less, as falling confidence suggests is likely, and businesses see a downturn in activity and, as a result, invest less, the unavoidable consequence is that the government will have to borrow more. This is what the sectoral balances suggest is inevitable, and they represent an unbreakable accounting identity that must always hold true, a fact seemingly unknown to almost any Chancellor in history.

This, then, is not something the government can avoid. As a matter of fact, it has to happen because the savings in question have to be located somewhere, and in this context, the government is the borrower of last resort or, in other words, the entity that must ultimately accept those saved funds via the commercial banking system and the central bank reserve accounts, with them then becoming a liability upon its balance sheet.

There will be much discussion in the media, almost all of it utterly uninformed, about what the government must do as a consequence of this increasing level of state borrowing.

Expect demands for austerity.

Anticipate attacks on social security.

Anti-migrant rhetoric will increase.

Presume that essential services will be described as unaffordable.

Accept the fact that there will be much gnashing of teeth around the rising cost of government interest payments, although nothing will be done to curtail them when there are options available for the government to do so.

But do not anticipate anyone quietly explaining in the mainstream media that if the economy beyond the government decides to save, as will inevitably now be the case giving the rising level of threats the people will feel to their financial security, it is both beholden upon the government to accept their deposits, which then become described as government borrowing, and to manage the resulting situation in the best interest of society at large.

This obvious statement of fact and requirement will be missing from public debate over the coming months. Understanding and explaining this is, then, the foremost task of those who read this blog, because by doing so, each and every one of us can create change in the economic understanding of how the government must face and manage the challenges that now exist.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Anticipate attacks on social security.

And we’re off… With today’s disgusting front page of the Daily Snide, with Fartrage demanding an end to the Social Security ‘culture.’

I have not seen that

And please can someone state that the biggest factor in the rising benefits bill is our pensions bill, not the disabled or migrants. I’m not saying we shouldn’t pay pensioners, but it’s an inevitable rising bill and the discussion should instead be about a more progressive tax system that claws back from richer pensioners to address this. I would suggest merging NI and income tax for a start along with the other measures you suggest for equalising tax on unearned income.

The hike in NI payments on lower paid workers is still having a huge effect on the service sector and jobs and I suspect costing more in benefits as people who would have worked part time are now more expensive to employ.

We desperately need a more positive narrative as people are rightly panicking and based on what is being said and this government’s track record, with good cause. Now is the time for a safe pair of hands, instead we have a rabbit in headlights and a ridiculous amount of time focusing on the Mandleson debacle and how long Starmer can last.

Thanks all round for the good advice to spread more valid explanations to reduce the influence/power of these unquestioned deceits.

Might this deceitful collusion between politicians, senior civil servants, and the main stream media be an instrument which increases tendencies to autocracy?

“Cartel conduct hides realities and stifles improvements.” [From Ausralian Competition and Consumer Commision]

So with money (savings) disappearing into the government coffers, the government COULD spend some of it back into circulation, as investment, targetted support for vulnerable individuals and SMEs? (while keeping an eye on inflation, and adjusting taxation priorities to aid redistribution but limit inflation). It could even have a look at interest rates?

I’m trying to think of omnibus-friendly explanations.

Whereas the government will say they have to make things worse, by removing MORE money from circulation by austerity cuts?

Everyone on the omnibus is now very angry.

If it uses it as capital.

The government both could and should spend money into circulation if individuals and businesses spend less (and by implication save more).

But I think it a tad misleading to say that the government could spend some of the money deposited with them into the economy. That, sort of, panders to the idea that government can only spend money they receive in taxes or borrowing, which is categorically not true. They can spend, or not, completely independently of whether they receive taxes or deposits. The issue is whether their spending may run the risk of causing inflation. That risk, and its consequences, are much overstated. Firstly, government spending may well create growth via the multiplier effect. Secondly, some inflation is inevitable whenever there are economic changes in the economy; inflation is a mechanism by which the economy adjusts to such changes. An economy without change, therefore without inflation, is a dead economy. At the present time, with the economy poised to tip into recession, government spending is needed to mitigate the recession and, hopefully, initiate growth. In such circumstances the multiplier effect is likely to be large and the risk of inflation very small.

You are right to want to clarify this, because the distinction matters.

The point I am making is that money can be deposited with the government in specifically sponsored arrangements to be used as capital for investment, much like any other structured investment vehicle. That is entirely feasible, and it is part of what I am proposing: a shift so that savings are channelled into productive use, rather than speculation. Denying this possibility is to deny reality. Please don’t do that.

That sid, it is important not to misrepresent how government spending in general works.

It is misleading to suggest that the government spends the money routinely deposited with it as gilts into the economy. That risks reinforcing the idea that government can only spend what it first receives through taxes or borrowing. That is not true. A currency-issuing government can spend independently of both.

The real constraint is whether spending risks creating inflation, and that depends on the availability of real resources.

In practice, when individuals and businesses choose to save more and spend less, government both can and should spend more to maintain economic activity. In those circumstances, the multiplier effect can support growth, and the risk of inflation is low.

It is also worth noting that some inflation is a normal feature of a changing economy. An economy with no inflation would be one with no adjustment, and therefore no dynamism.

So the argument is twofold:

* savings can and should be directed into productive investment, including through government-backed special purpose vehicles from both ISA and pension savings

* and government should use its capacity to stabilise and support the economy, especially when private demand is weak

Confusing these two points leads back to the very misunderstandings that need to be avoided.

Thanks Richard for the very helpful clarification. 🙂

I’m testing if I’ve learned my lessons well…

would the reduction of the BoE rate of interest stimulate growth by sending a different msge than ‘tighten your belts’ or wld this now seem to be an act of stupidity in the pending doom of upcoming correction?

I realise that for the BoE to behave in this way wld cause confusion as it wld herald a seismic paradigm shift- that wld spook everyone- and cause Richard to splutter over his breakfast!

You have learned part of the lesson well, but I would frame it differently.

I have long argued that interest rates should be at net real zero — in other words, no real return to holding money and no real cost of borrowing it. Money should be a means of exchange and saving, not a mechanism for extracting rent.

So I would welcome lower rates for that reason.

But let’s not pretend that rate cuts, on their own, create growth. They do not. They are still a blunt tool.

The UK’s real problems are weak investment, poor infrastructure, inequality, low productivity and a lack of strategic planning. Interest rates cannot solve those issues.

What lower rates can do is remove an unnecessary burden from households, businesses and government borrowing costs, whilst reducing the subsidy currently paid to wealth holders.

Growth then requires what it has always required: sensible fiscal policy, investment and planning.

That would not make me splutter over breakfast. It might simply make me wonder why it took so long.

I will do my best but I work in a public sector that moans collectively about a lack of money for services whilst individually moaning about their taxes which they think pays for it. Dealing with that is like hopping through treacle, let me tell you.

The cunning of unreason is everywhere.

Agreed

On the Newsnight panel last night – Matthew Syed (who has presented some fairly creative and whacky ideas on his Sideways radio 4 series) , has now turned into a shrill propagandist against our ‘unaffordable debt’ – ‘we are paying more on interest payments than on defence ‘etc etc – with absolutely no challenge.<p>

He can be a very cogent and dogmatic speaker , with no one on the panel offering a challenge to his diatribe against banks bail out in 2009, the covid furlough scheme, winter fuel payments etc etc , and saying government mustn’t do it again in the Iran war crisis.<p>

When will the BBC ever have Richard on a Newsnight panel who will have a quiet – or maybe not so quiet – word of explanation?

He needed to be asked to one very simple question, which is what does he wish for? His proposal is for a failed state. Is that what he desires?

I’m definitely going to try and explain this to people, at every opportunity!! Maybe get some key points printed on a sweatshirt.!? Re.govt borrowing. Only half joking as well. I probably need frequent reminders myself.

The government seeks to balance books by cutting spending in a down-turn. All this does is impose further pain in an already painful period, and maximise the number of households and businesses pushed to bankruptcy.

The government needs to learn that it needs to be counter-cyclic. It should be aiming to smooth peaks and troughs, spending into a downturn and cutting spending or increasing taxation in an upturn.

It also needs to recognise some things are lagged. The pension triple lock ignores it as it will boost pensions based on inflation during an inflation spike, and then boost pensions based on wage increases that are only catching up with the earnings lost to inflation, covering the triggering and the derived lagging indicator. The same applies when inflation causes the BoE to raise interest rates and then they use wage inflation to keep them higher for longer.

Some are stretched out. Early in a shock like the impact of the Iran War some consumer activity may not slow as quickly, because some households and businesses have some reserves and can weather a shorter-term impact. However, if nothing is done early, then not only may things deteriorate faster than expected if the shock remains (as seems likely), but even afterwards the loss of those reserves means that slow and limited support causes sluggish activity while regaining that buffer.

Once the government understands its role stabilising economic cycles and neither under- or over-correcting by considering immediate and lagging indicators together not separately it might do better. The response to the Iran War – considering plug-in solar, considering targeted action on energy prices and energy auctions – suggests they’re starting to learn, but they have a long way to go.

You’re absolutely right Richard. We have a responsibility and should take every opportunity we get to challenge current thinking to the best of our ability. We may stumble and we most likely won’t get the message over with the clarity you display but I don’t think that matters too much. People are angry and are going to get angrier, so I think just even being a signpost to another way will help

Re getting the msge out, I was at a 50th wedding anniversary on Saturday and to mingle we had an A4 sheet of prescribed Qs in boxes eg, who speaks a foreign language fluently, who lives in Scotland etc, what are your interests since retirement, etc.

Everyone I spoke to got the “I’m into political macroeconomics” conversation!!

I spoke to the Scottish resident at one point who was a retired financial services guy. “Yes, I know of Richard Murphy”, he said. And yes, he understood and agreed with him.

result!

Thank you!

Might the phrase “An increase in government banking activities” be an acceptable/appropriate alternative to “An increase in national debt”?

Yes