My old friend Prem Sikka, who now sits in the House of Lords as Lord Sikka, drew my attention yesterday to a couple of answers that he had received to the questions he had asked the UK Treasury. I am glad that he did, because they are deeply relevant to some of the work that I have done over time.

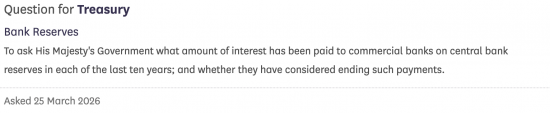

The first question that Prem asked was this:

This is the reply:

The second question, which was connected, was this:

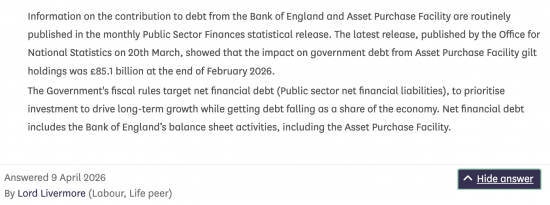

The reply was as follows:

As Prem understands, and as the Bank of England has always admitted, the Bank of England Asset Purchase Facility, to which these figures relate, was created as part of the quantitative easing programme put in place by Alistair Darling in 2009, when he was Chancellor of the Exchequer, and which was enthusiastically embraced by Conservative Chancellors of the Exchequer from 2010 until 2021, by which time £895 billion of funds had been created by the Bank of England so that it might repurchase from financial markets government bonds previously sold to financial institutions by HM Treasury.

The whole operation was, as I have often described it, a sham. The issue and repurchase of the bonds in question was a fabrication intended to disguise the fact that the UK Treasury can, whenever it wishes, create money for public benefit if the government thinks it appropriate to do so, and there is, as a consequence, no dependence by the state on taxation or borrowing to fund UK government expenditure. QE was, then, a massively contorted, wholly inappropriate disguise, put in place solely to pretend that modern monetary theory is not a correct explanation of how the UK economy actually works.

As is clear from the information supplied to Prem, the cost of this wholly unnecessary programme has been phenomenal. To date, interest paid to the UK's commercial banks on the funds that the Bank of England injected into the UK economy, for which these banks acted as a conduit, and which it was said they deposited with the Bank of England when they were in fact gifted the sums in question, has been £85 billion of wholly unjustified interest payments to date.

The vast majority of this sum has been paid, as will be noted, since the Bank of England decided, wholly unnecessarily, to increase the Bank of England base rate from 2022 onwards, with the supposed goal of tackling inflation in the UK economy, on which those interest rate increases did not, and could never have had, an impact, because the inflation in question was imported from international commodity markets, where prices were inflated as a consequence of the actions of financial speculators, some of them undoubtedly based in UK commercial banks, who artificially inflated commodity prices after the onset of war in Ukraine.

As Prem's second question and the related answer show, these payments were made by inflating what is described as the UK national debt, about which UK politicians, the Treasury, and many financial commentators are obsessed. The total value of those payments now exceeds the probable value of all notes and coins in circulation in the UK economy.

What is worrying is the fact that if these funds had been spent more appropriately, many of the recent cuts to social security, health, education, and housing budgets put in place by both Conservative and Labour governments would have been completely unnecessary.

Alternatively, and to pursue a theme from this morning's video, defence could have been funded to the level that those inappropriately obsessed with the subject now demand, without ever having to consider cutting social security expenditure.

We still have the opportunity to reduce these payments. It is entirely possible for the UK Treasury to demand that these interest payments on these central bank reserve account balances cease. Even if it were decided that some needed to be paid as part of an ongoing interest rate policy, the potential savings would still easily exceed £10 billion a year. When the defence budget is only just over £60 billion a year, it is not hard to see what the impact of such a change would be.

In that case, the obvious question that needs to be asked, and which Rachel Reeves has always refused to answer to date, is what is the justification for these continuing payments, which represent a straightforward and unearned bung to the UK's commercial banks, from which it would seem they have been unjustly enriched every year of late, at cost to the most vulnerable people in the UK economy who have suffered restrictions on the amount that the government has been willing to spend for their benefit as a result?

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

“Back in the day”, reserves were typically in short supply so it was actually banks paying to borrow from the BoE. Then, in the crisis, the BoE (first) cut rates to zero and (then) started buying gilts. That gave us a huge level of reserves (each £1 spent to purchase a gilt created £1 of reserves)… but as rates were zero it meant very little interest was paid.

Now we have large reserve balances AND high rates so the issue of paying interest on these reserves matters.

Can we just stop paying interest? No, all that would happen is that banks would buy gilts instead and drive (short dated) gilt yields down to zero…. making it impossible to run monetary policy.

What we CAN do is require banks to hold a minimum level of reserves (which would attract no interest). Deciding which bank should hold what might be a bit problematic but it is the way things used to be done in the 1970s but I am unfamiliar with the details – even I have not been in the markets that long!

Finally, QE (for good or bad) is a complete red herring in the discussion about remuneration of reserves. Whether QE or “Ways and Means” (Government overdraft at the BoE) there would be excess reserves. For what it is worth, I thought QE (a mere shuffle of papers between two parts of government (BoE and HMT)) was an elegant way to allow “monetization of debt” without serious political pushback or change in the law (remember using “ways and means” was against EU Law).

Thanks

I hestate to contradict such an experience person as Clive, but using the Ways and Means was specifically allowed for the UK only under Protocol 15, paragraph 10 of the Consolidated TFEU. A very valuable exception.

You are correct. Thanks.

It is interesting that no party has studied this and used it as a platform from which to pressurise the government. It would carry a lot of heft with the public. I can only assume they are all warned off by the Treasury that “measures” will be taken to ensure this does not become an election issue.

In a properly functioning political economy – including the MSM – this should be in all the national newspapers – not just on a blog like this – excellent as it is.

This is the REAL failure of our country. It has nothing to do with the ‘people” it is a complete political failure of those elected to manage the country, let alone that it appears to me that the rich have captured the money making capacity of the state for themselves and which renders us as an ‘undemocracy’ in my opinion.

Agreed

Surely there must be enough MP’s who understand this – to keep banging away and asking/demanding these bungs to the banks should be stopped . Paying interest on government-created money should be paid to government, and not to private banks. Such interest is apparently not paid in Japan, ECB etc.<p>

Whenever ‘there is no money’ comes up – that should be the immediate response- ‘yes there is – what about the interest on our money paid to the banks?’ . But there is never any such discussion – the ‘fiscal rules’ are sacrosanct . This is censorship – ‘managed consent’. Far more chilling than 1984.

.

Agreed

I did write to Tulip Siddiq (my local MP) asking why we don’t tier the CBRA interest rates, she passed the question on to the Treasury and received this response:

“The Bank implements monetary policy by paying interest on reserves held at the Bank by the banking sector. Paying interest on reserves is an important part of the transmission of monetary policy to the real economy, which is crucial for achieving price stability. By paying interest on reserves, it allows the Bank to control short-term market interest rates in the expectation that these market rates transmit through to borrowing and savings rates for firms and households, and subsequently impact the real economy, and aim to keep inflation at the 2% target.”

So they just completely ignored the tier question and regurgitated their dogma. Like talking to a brick wall.

Full response here:

https://drive.google.com/file/d/1DaUtfenCuzxtlUlM8zfC2caGjdEFNZSh/view?usp=sharing

Matthew, I too asked my MP to write to the Treasury who replied –

“The Bank of England has operational independence from the government to carry out its statutory responsibilities for monetary policy and financial stability. Monetary policy, including quantitative easing, is the responsibility of the independent Monetary Policy Committee at the Bank of England.”

Everything about QE has always been directly subject to Treasury approval. The claim made is directly untrue.

I responded to an article in newspaper today (which said Chancellor needed to remove triple lock on state pension to help fix the alleged budget hole). Kept it simple as my understanding of this is basic!

‘More generous (or less mean) support for people of all ages, who need support with everyday expenses like food and heating, is fair and ethical, as well as being rational; apart from keeping people healthy, most of it is spent and boosts the economy.

That cannot be said for the huge sums paid to commercial banks as part of the QE system. The Band of England credits the government to meet their agreed budget, the government spends, then taxes. Obscuring this basic system in the QE machinery results in a huge waste of money. This was all put in place in 2009, it should be dismantled. More than £10 billions could be saved annually.’

Good work

Everything in our society is a massive con.

I know as much about the economy as the average person in the street. But I can’t help but feel that after the 2008 crash when the banks were bailed out, why as an alternative, weren’t they allowed to fail and the money be given to the public instead? I guess as a universal basic income? As my understanding is then, people would spend it on things that made the economy turn, rather than it be extracted into the ether or used to ballon asset prices (buildings). In my head, instead of “trickle down”, should it not be “trickle up”?

Simple: our economy would have completely failed and any saver would have lost their money, with the government at risk of picking up the bill. Only a system redesign can prevent this happening again.

Much as I am loathe to write anything that might be seen as favourable to Reform UK, this issue was raised by Richard Tice more than once in mid-2025. See: https://bmmagazine.co.uk/news/reform-uk-clashes-with-bank-of-england-over-interest-payments-to-lenders/ (June 2025) and a Telegraph article in Sept 2025: https://www.lyddonconsulting.com/richard-tice-of-reform-uk-is-wrong-the-bank-of-england-should-not-stop-paying-interest-on-financial-institutions-reserves/ It is not clear if there has been follow-up since then.

I think they drafted a bill on QE last year.. On the day it was introduced, the Reform UK Ltd leader, MP for Mar-a-Lago South was visiting the Great Healer over the pond. He didn’t bother voting on it anyway. THAT’S how serious they are. And the sponsor Rupert Lowe split from Reform to form the even more nasty Restore.

https://www.taxresearch.org.uk/Blog/2025/01/13/reform-wants-to-destroy-government-and-the-economy-as-we-know-it/

I’m sure it was raised as a form of extortion, “Give us money, or we will end this lucrative arrangement.” The City is a major Reform sponsor after all.

I’m not sure what rate of interest is paid on CBRA’s but to be fair it should be the same as the commercial banks are paying their account holders who are the recpients of the newly created money. In other words the net revenue for a commercial bank as a result of creation of the CBRA’s s should be nil. I’m writing this listening to R4 news, Evan Davies has just said “commercial banks get their money from deposits”. We have a long way to go.

There is no reason for this interest, at all.

This interest on what is actually a current account was not paid from 1694 until May 2006. What it actually does is discourages banks from putting their reserves into gilts, so will tend to reduce demand for gilts and thus increase the interest rate. If the BoE should control interest rates by buying or selling gilts. I think the ‘monetary transmission ‘ stuff is a red herring and not even Clive managed to explain how it was supposed to work in a way I could understand.

Noted

Just to add to/clarify my comment on Tice’s remarks, I have no interest in praising him for raising the issue (and indeed, it’s questionable whether Reform UK is serious about it); what interests me is that even though the issue was raised in a fairly prominent fashion by a not insignificant political figure, hardly anyone from any other party seemed to find it worth looking into (which is a bit odd when you consider the huge sums of money involved). Why not? After all, Labour has paid plenty of attention to the views of Reform UK on some other issues. There could be various reasons, including (1) there is no evidence that voters care about this issue (in contrast to matters such as immigration, asylum etc) – hardly surprising given that voters are not aware of it (2) few politicians understand it (I seem to recall that when Tice was asked on the Today programme why other people weren’t making this suggestion, this was the reason he gave). But if MPs can’t be bothered to inform themselves about fundamental matters of finance, that seems a gross dereliction of responsibility. In any case, the apparent lack of interest across the political spectrum is pretty damning.

My sources tell me that ministers do not understand this.

Fra Pacioli is very good on this and points out that the Fed and the ECB have handled the same problem differently from the BoE, which is an international outlier. And the NEF argues that the banks’ windfall can simply be taxed back if it’s too much trouble to change the underlying nonsense.

https://open.substack.com/pub/frapacioli/p/the-multi-billion-pound-budget-scandal?r=7dnd50&utm_medium=ios

A lot of this goes over my head, I’m afraid, but one thing puzzles me: why are people “obsessed” with the National Debt? Is it really that important? Quite a lot of us receive pensions etc. which are part of that so-called debt, and we are glad to have them.

No, it is not that important unless you want to constrain the size of government, which is a neoliberal obsession.

Simply because it is called a ‘debt’. My parents were terrified of the idea of falling into debt, and would have had no notion of why such a thing should be different for the government.

It’s the same reason why I’ve suggested Richard should remove the word ‘overdraught’ from his explanation of how a central bank can create new money without creating a very frightening debt which must be repaid with interest.

I absolutely agree, Kit. I have said the same thing, and also I don’t like “Borrower of Last Resort”. But I can’t come up with a better way of rephrasing it in a sentence. I only wish I had Richard’s impressive command of linguistics.

I wish I was better at it