I posted this video on YouTube this morning:

In case the link does not work, you can watch the video here.

This is the transcript:

Inflation always goes away. Now, that's an extraordinary claim to make, but I can show you it.

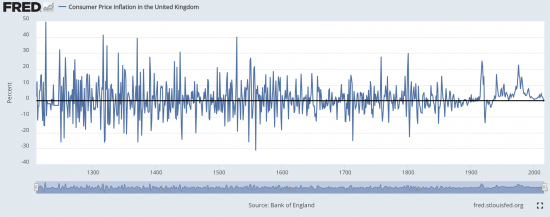

This chart, produced by an American central bank called the St. Louis Fed - which always produces amazing economic statistics for those who want to look at such things - is actually a reproduction of research undertaken by the Bank of England, which shows the inflation figures in the UK since before 1200. I don't mean before midday. I mean literally from 1200, 800 years ago.

What you see is that the chart shoots up and downwards in the early eras on the left hand side, and gradually it tapers down so that these days we have much smaller oscillations when it comes to inflation.

The peaks are smaller than they used to be, and there are almost no negative troughs, i.e. we don't have periods of deflation in this country now. But the critical point I want you to note is, that after any inflation spike, there's a downturn.

Now historically, that downturn was almost invariably a period of deflation. In other words, real prices fell.

Now that, in the last century or so, is not the case. After a period of inflation, real price. changes fall, but prices don't go back to where they were. So, over the last century or so, we've had a period of steadily rising prices. But it's still true that after any period of inflation, really quite quickly, excepting periods of world war, prices return to relatively low levels of inflation.

And the critical point to note is that all that happened when we didn't really have a central bank who did anything whatsoever to control inflation.

The Bank of England might have been created in 1694, but it didn't get a mandate to control inflation until 1998. So, for the vast majority of the time that that chart was being plotted, there was no central bank raising interest rates, trying to control inflation, setting a 2 percent target, or any of that other nonsense that Governors of the Bank of England now talk about.

And yet inflation went away, anyway. And that's because markets always correct for the panics that create inflation in the first place.

Inflation is almost always created by a panic. There's a shortage caused by plague, pestilence, war, you name it, something's gone on in the world. Trade has broken down, and therefore there's a shortage and prices go up.

Once we get over the panic, we realise that actually the world did not end as everybody thought it would.

Remember the toilet roll crisis of March 2020 everyone went out and bought toilet rolls as if there were never going to be any available ever again. Well, it's exactly that sort of panic multiplied by an enormous factor that creates the shortages in world markets when a big event like the outbreak of war happens and market traders panic and try to buy things as if there will never be wheat, oil, gas, fertilizer, or anything ever again.

There were toilet rolls after March 2020. There has been oil, gas, wheat, fertilizer, and everything else since March 2020. The prices, once the traders realised that they had simply panicked inappropriately, went back to normal. They didn't necessarily go back to the price that they were in March 2020, but they certainly returned to a very normal level.

Inflation went away.

We did not need interest rate rises.

We did not need austerity.

We did not need the Bank of England telling us that none of us would do a pay rise.

We did not need them to say to the government that they should not be spending because they had to pay interest - extra interest - instead.

No. We just needed to wait for the markets to stop panicking. But instead, we had the Bank of England doing something quite different. They put in place policies that were designed to exploit the situation where inflation had started so that the wealthy became wealthier because money was moved from most ordinary people who pay interest to those who have very large sums on deposit.

That, again, is something we do not need again. Inflation goes away. It's a lesson we have to learn. And until the bankers do that, frankly, we shouldn't be giving them any power over our economies at all. Because they use that power wholly inappropriately and against the public interest.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Hi, I’m interested in what role Goodhart’s Law might play here: “When a measure becomes a target, it ceases to be a good measure” (https://en.wikipedia.org/wiki/Goodhart%27s_law). This means that, since 1998 at least, because the BoE is dicking about with its control levers in response to inflation, then inflation is subject to the normal inflationary influences *and* the BoE interventions (thereby ceasing to be a good measure of anything). I have myself seen some impact of this from my work, in the chemical process industry, where extreme scrutiny on in-process specifications (i.e. targets) of various quality and efficiency measures led to er… ‘unfortunate’ reporting practices at the spec limits that could be picked up by the right (very simple) stats treatment.

Loving your videos, btw, even if they make my brain hurt sometimes. I’d really like you to be on the panel of ‘Any Questions’ (that’s the one on Radio 4, not the one on BBC 1) some time, or to be interviewed on Today etc. Maybe even have the chance to do your own edition of “Analysis”. Your thoughts need a bit more exposure.

Thanks Nigel

I have been on Today, but not of late

I have done Denate Night in Scotland – the equivalent of QT

I certainly agree with you there Nigel. Targets are not a good idea. That one set by the Scottish government relating to emissions reductions being an obvious example and missing it led to the withdrawal of support from the Scottish Greens.

Measure who you are doing by all means.

“Measure who [?] you are doing by all means.”

Freudian slip? 🙂

I visited the BoE Museum last week and was alarmed to see this exhibit on prominent display

https://youtube.com/shorts/-buQKq675zM?si=BOf67oowlaLi3D7x

Very odd indeed…

And so misleading

It suits their agenda though. And most of the British (nay global population) think it sounds plausible enough. Who are we to argue!

It is to me, far more revealing of the frankly quite potty BoE mindset, than it is odd. Pull a lever, and ‘laws of (financial) nature’ that are never adequately explained, still less demonstrated, come into operation. That is the implication of this tawdry plaything. The effects of the “shocks” do not appear to be explained.

It is not “alarming”, either; it simply looks quite mad. It is, however an appalling deceit. It is set up as if it was an experiment (like a public, educational ‘Science Centre’); a tube containing liquid under pressure, and a force dispensed by a lever. But it isn’t an experiment; it is no better than a pre-set fraud, to illustrate assumptions the BoE could never prove have any merit whatsoever; based on real science.

The BoE has never conducted a genuine scieintific experiment in its history. It has more often than is reasonable to expect made bad decisions; and failed to learn from history either.

I see that the Swiss Central Bank reduced interest rates in March on the basis that inflation in Switzerland was falling

But no surprise that this was not widely reported in the UK main stream media.

Depending on where the market disruption has come from to create the price rises , there must be a case for taking short term action – to maintain basic living standards for lower income groups

Maybe selected controls on key prices, rents etc. , windfall taxes on excess profits etc

As you Richard – and others – have long argued – interest rates rises do not control it – and often only makes it worse.

But we shouldnt give the impression that just because it will eventually correct itself – (subject to market distortion by monopolies) , inflation doesnt matter.

Action may well be needed , but not the cultish ‘blood letting’ interest rate fetish.

Agreed

Regulation and fiscal policy works

Interest rate changes do not

From 1200 or so, when that data set starts, money was on the silver standard. Henry VIII’s Great Debasement was about silver coinage, not gold. By the 19th century we were on the gold standard. True, off that from 1914 to 1925, then off again in, erm, 1932? After 1945, Bretton Woods which tried to do much the same thing.

The point about such varied fixed value standards for money being that they create that anti-inflationary pressure. Because you’ve got to change your interest rates, or at least damp down the inflation, in order to be able to maintain the gold standard.

So, up to about what, 1979 (?) we’ve got that process that kills inflation. In concert with this post-1945 we’ve got Chancellors deciding the bank rate and they do so by trying to mix and match growth and inflation. Not well, but they tried. So over that period we’ve also got a countervailing force against inflation. Well, some of the time.

But apparently inflation just goes away without anyone doing anything even under a silver, gold or Bretton Woods style monetary system.

Seriously Richard, this is a very weak critique.

I post what you say

And if you really think international exchange rates or interest rates had the impact you claim over the periods you are looking at I seriously suggest you change what you are smoking – because they did not

Why? Because shocks remained universal, at least amongst major trading partners as they tended to all be at war simultaneously, usually with each other.

Money supply issues also moved in parallel.

And international banking was virtually non-existent.

So, you are projecting the post 1980s world of free capital movements onto an era when that did not exist.

Tell Tim Worstall he has got it wrong, again as I bet you plagiarised this.

Everything I say stacks, I suggest. Sometimes you need to stop making excuses and look at the evidence.

James, that is a terrible summation of monetary history and the Gold standard, or silver standard.

First, Britain suspended the use of commodity convertibility, and had an inconvertible currency 1797-1821. When it returned there was a threefold standard; gold specie, gold bullion, and gold exchange. The return of gold convertibility (and the first clear gold standard in 1821) was not a great success. Second, by 1825 Britain had in consequence experienced a boom, followed by what is probably the worst financial crisis in its whole history in 1825. There is a comic element in the gold standard in this period; Nathan Rothschild was profitably shuffling gold back and forward to Paris for the Governor; but when the crisis struck the BoE was scraping around and eventually using unexpected finds of notes to stave off disaster. The reasons for the 1825 crisis are still disputed (economics can’t provide a decent explanation, even when it knows the outcome; thus the economics profession’s serious failures are not simply explained by a failure to predict – ie., science; or to forecast – ie., muddle through; but even to understand the history, where it fails).

Third, the problems in 1825 were multifold, because the level of understanding was poor, the information asymmetries ran riot, the lack of transparency and disclosure of key information (by the BoE most of all) was deplorable; not least the inability of the BoE to understand that it required a ‘lender of last resort’ role (difficult, when the BoE is both the sovereign state’s bank, and a private bank operating in its own interest).

Finally, the Gold Standard in Britain was officially canonised in 1844; but that didn’t begin to end the problems. There was a banking crisis in 1847. The problem with a gold standard is easily seen; as soon as a real crisis hits hard, ie., when the Standard is supposed to command authority; what actually happens is – the gold standard is swiftly suspended. That is standard procedure. It is there when you don’t need it, and disappears as soon as you do. Commodity standards are required where there is a chaotic international trade market and nobody trusts anybody else’s currency. It worked best in the pre-industrial world when state’s operated internationally, and principally to fight wars. It was a search for a common, generally agreed price where chaos otherwise reigns; but it has two signifiers, one as ‘money’, the other as ‘commodity’, and they may not be the same. It is a very bad way to operate a modern monetary system; and was in the ninettenth century.

Thanks John

Much appreciated

“But it’s still true that after any period of inflation, really quite quickly, excepting periods of world war, prices return to relatively low levels of inflation.”

What happened between 1969 and 1994? The average rate of inflation in the UK was 8%. That’s 25 years. It averaged over 12% in the 1970s. Is that your idea of ‘really quite quickly’?

You were around then. Did you not notice?

If there was a world war, I must have missed it.

Was 8% disastrous?

Real wages and total national income grew

Would that have happened otherwise?

Real incomes have been stagnant since 2008 with low inflation until late 2021, from which they gave not recovered. Which would you prefer? Why?

The inflationary spike in Germany of 1921ish was brought down by Streseman refloating the economy with a complex series of loans and US and UK not forcing the payment of reparations.

The spike in Austria was brought down by Ignaz Seipel with a whole new currency and stringent spendin cuts with a credit negotiated from the League of Nations.

So doing stuff does work.

But that stuff was not austerity and interest rate rises