The FT has noted research by the Resolution Foundation this morning, reporting that:

The overall boost to UK savers' incomes from higher interest rates outstripped the impact of increased mortgage payments on households, according to new research from the Resolution Foundation think-tank.

They added this detail:

Real income from savings rose by £34bn over the period — more than offsetting the £18bn rise in debt interest costs. The boon accounted for three-fifths of all household income growth since the last quarter of 2021, the research found.

Three observations follow. The first is that this adds to my belief that interest rate rises have fuelled inflation by increasing the disposable income of the moderately wealthy, likely more elderly population, who have an inclination to spend.

Second, it makes clear just how little of the impact of interest rate rises has already arisen - and how much more is to come, supporting my suggestion that recession is likely as a result of them.

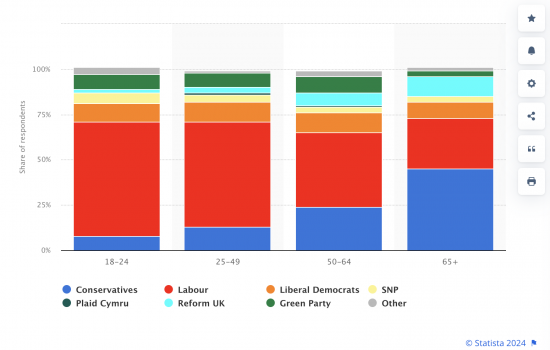

Third, there is a political dimension to this. We know that the wealthy tend to be older. So too are Tory voters. As Statista has reported, voting intentions in a general election in the United Kingdom in September 2023, by age group, were as follows:

Interest rate rises are very clearly to the benefit of the only age cohort displaying core support for the Tory party. Why would they want to change that?

Which leads to another question, which is why is Labour not saying it wants to see rates fall? I wish I knew.

In fact, there is so much about that chart that begs so many questions of Labour that one wonders where they are on the political planet. Or is it that they simply think that they have the young, like the left, in the bag, and so are spending all their time playing to the old? If so, why? Taking their existing support for granted when there may be ten months to go to an election really does not seem like a very good idea when the party seems determined to say nothing about what it will do for anyone. This election is not over yet.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

The wealthy own property, bonds and equities. They all fell and quite dramatically with the rise in interest rates. The wealthy (to use a generic term) much prefer lower interest rates as the assets they own are worth more. What you say in isolation is true but it doesn’t explain the full picture. And to be honest this is very much your style of commentary.

OPlease note how I defined my terms – making clear that this issue did not realte to the very wealthy but to those with moderate savings

But you chgose to ignore that, of course

Jacob – what a teapot you are, eh.

Go back to the cupboard where you belong.

What you have pointed out for a long time now, and ignored by Jacob in his comment is this perverse redistribution of wealth from the neediest in society – Seemingly the only agenda is to redistribute wealth to those not in any need, and most likely to vote Tory, so that they can squeeze in that extra golf holiday and feel pretty smug about it in the process. While hard working individuals, families and small business have been crippled by this mind-boggling state sponsored incompetence.

Deja Vue

Back in the 80’s when Interest Rates were in the region of 15% it was exactly the same with Dixons as then was reporting that HiFi’s and Camcorders (remember those!)were being snapped up by pensioners who were benefitting from what was in effect a huge transfer of income from mortgage payers to savers.

Clearly the bankers have learnt nothing.

Now of we were to use tax instead of interest rates to control inflation…………..