Precisely because I wanted to make clear that raising more funds from those with high incomes and wealth in the UK did not require a wealth tax I deliberately chose to defer any discussion of inheritance tax in the Taxing Wealth Report 2024 series until many other taxes and issues had already been touched upon.

It is now time to correct that. Over the coming days and weeks a series of notes will be issued on inheritance tax reform to add to the suggestion already made that domestic residences be taken out of the scope of this tax and that they be subject to capital gains tax on last disposal instead.

In this introductory note I set out the reasons why even these are limited in scope: although inheritance tax is flawed, debate on finding additional revenue does not require its replacement as yet, although it may do in due course.

Background

Inheritance tax is the only tax in the UK that is supposedly charged on wealth.

If reports from opinion pollsters are to be believed, it is also the most hated tax in the UK[1].

Paradoxically, inheritance tax is also one of the taxes that a person is least likely to pay in the UK. In the tax year 2020/21, which is the last for which reliable statistical data is available, just 3.73 per cent of all estates in the UK were subject to an inheritance tax charge[2].

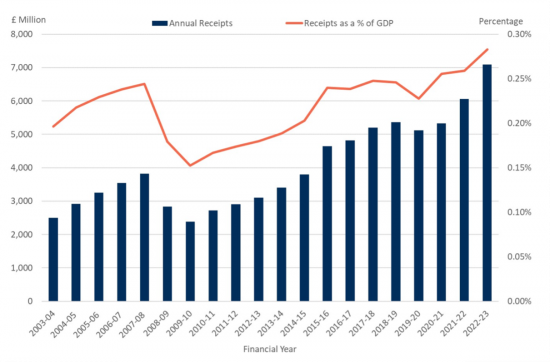

In the last year for which reliable tax collection data for this tax is available (2022/23) the tax yield from inheritance tax was just over £7 billion, which sum amounted to less than one per cent per cent of UK tax receipts as a whole. Both amounts were records, as the following chart indicates[3]:

Annual receipts of inheritance tax and receipts as a proportion of GDP

HM Revenue & Customs has suggested that recent increases in yield are likely to be due to a combination of recent rises in asset values and the government's decision to maintain the inheritance tax nil rate tax band thresholds at their 2020/21 levels up to and including 2027/2028. Even so, revenue remains modest, overall.

That said, increasing revenues might suggest that concern about this tax is unjustified. There are, however, good reasons to think that inheritance tax is not working as it should.

The problems

Firstly, as a proportion of UK wealth the amount of inheritance tax paid is miniscule. Current estimated UK financial wealth is, according to the Office for National Statistics and in particular its wealth surveys[4] approximately £15,221 billion. The failure of this tax to make any significant inroads into wealth or to tackle wealth inequality suggests that it is poorly designed, inappropriately targeted and highly avoidable by some. That means that the tax is failing to address issues with regard to vertical tax equity and inequality in the UK. It may also be creating horizontal tax inequity.

Secondly, inheritance tax's treatment of the taxation of former domestic residences, either on death or in the years prior to it, is inequitable. Since property prices vary enormously around the country applying a consistent tax rate of tax on the value of particular asset if above a fixed sum does appear to be particularly unfair. For that reason, a note in the Taxing Wealth Report 2024 series suggests that the inheritance tax charge on former domestic residences should be replaced with a capital gains tax charge on the final disposal of a former domestic residence by a person tax resident within the UK, with certain caveats and conditions attached. The inheritance tax anomaly relating to these assets would be removed as a consequence.

Third, there are significant reasons for concern when this tax appears to be quite effective in imposing charge upon the estates of those with smaller estates primarily made up of lifetime savings and domestic residences but appears to be particularly ineffective when taxing the estates of the wealthiest.

Inheritance tax is in need of reform.

Recommendations

The obvious long-term solution to this problem is to replace inheritance tax with a lifetime gifts receipts tax, which would be substantially more equitable. However, in view of the wide range of other recommendations already been made in the Taxing Wealth Report 2024, a series of more modest recommendations will be made here. They will be:

- To take domestic residences out of the scope of inheritance tax and make them subject to capital gains tax on death or last disposal. This issue is addressed in the capital gains tax section of this report.

- To review inheritance tax business property relief.

- To review inheritance tax agricultural property relief.

- To review inheritance tax charges on personal pension funds.

- To review the use of inheritance tax reliefs on gifts to charities and related issues.

- To review inheritance tax rates and allowances.

Each of these issues is addressed in a separate note within the context of The Taxing Wealth Report 2024.

Future work

Whilst the Taxing Wealth Report 2024 is limiting itself to reforms that might make sense in the short term and which can be adopted in isolation, this does not mean that future work cannot address the significant weaknesses within the structure of this tax, including:

- That the basic logic of a tax on death, charged irrespective of who inherits (charities and spouses apart) makes little sense. A tax on the receipt of gifts would make much more sense and promote greater equality.

- That the rates at which the tax is charged are too inflexible; a progressive scale would make much more sense.

- Arrangements for long-established trusts still mean that some property falls beyond the scope of this tax.

These, however, are issues for further attention in due course and are, as a result, beyond the scope of this current review.

Footnotes

[1] https://www.hl.co.uk/news/articles/archive/britains-most-hated-tax

[2] https://www.gov.uk/government/statistics/inheritance-tax-statistics-commentary/inheritance-tax-statistics-commentary

[3] https://www.gov.uk/government/statistics/hmrc-tax-and-nics-receipts-for-the-uk/hmrc-tax-receipts-and-national-insurance-contributions-for-the-uk-new-annual-bulletin

[4] https://www.ons.gov.uk/peoplepopulationandcommunity/personalandhouseholdfinances/incomeandwealth/bulletins/totalwealthingreatbritain/april2018tomarch2020

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

I have issues with the whole inheritance tax situation. It seems to end in a polarised ‘debate’ between those who are totally against it and those who consider all inheritances should be taxed. Not sure that I agree with your proposals either Richard! As alternatives I wonder if IHT should be paid by beneficiaries taking into account their assets before receiving anything. If you already owned a property you would pay more than someone who did not. Also think some sort of upper limit on property including land would be a better option. Above the limit, you would pay additional tax. At the moment we have owners of large landed estates who I gather do not pay IHT whereas smaller landowners may do so. Business and agricultural reliefs are useful in preventing the loss of businesses or farms, which is why an upper limit might be more equitable.

Your summaries of your report and its suggestions have been very clear for the most part. Here if I understand it would seem clearer to say that inheritance tax will be abolished and all inheritance treated as an income from a gift. Presumably beyond your proposed limit tax would be at the recipient’s marginal income tax rate. Is this what you propose? If so it seems like the other suggestions eminently sensible.

Please accept my apologies that I have not found time to read the full report if that makes all clearer.

I am not saying what you suggest, at all

I am saying inheritance tax should be replaced by a tax that takes into account the position of and number of the recipients of an estate and how much else they might have received in life – but definitely not that it be treated as income. I think it would have to be a separate tax.

The Duke of Westminster inherited just under £10 billion and paid little tax because it is in a trust. I don’t know enough to comment but I imagine this is one area which could be reformed.

I don’t see the second problem as a problem. A similar house, in a different part of the country, that’s worth a lot more, gives the heirs a bigger inheritance, so why shouldn’t it incur a lot more tax?

… Unless you mean that it’s easier to avoid tax on assets other than one’s own home by giving them away (as a “potentially exempt transfer”) as then surviving for at least 7 years? So that a person with the same total assets, but with a larger proportion of them tied up in their main home, has less opportunity to avoid IHT? That could be addressed by bringing all PETs back within the scope of IHT (like the old Capital Transfer Tax that preceded IHT). Or by moving to a lifetime gifts receipt tax, as you suggest; but abolishing PETs might be a shorter-term move?

As I said on the post on charging CGT on main residences, I think exempting them from IHT is creating opportunities for tax avoidance. A strategic advantage of your proposals for horizontal tax equity is that they remove a motive for avoidance, by converting one form of income into another, or income into capital gains, because they will all be taxed at the same rates anyway. I think it’s unfortunate to create motives for avoidance re main residences.

Why are you *not* proposing taxing unrealized CGT at death on assets already within the scope of CGT? Wouldn’t that raise fewer issues than doing the same thing for main residences?

Charging CGT on all unrealized gains at death could then be combined with cutting the rate of IHT, or at least cutting the starting rate to a lot less than 40%, but perhaps having tiers with higher rates for larger estates.

On the longer view, perhaps one reason why IHT is unpopular with ordinarily rich people is that they know it’s almost entirely avoided by the super-rich – e.g. the newspaper proprietors, as opposed to the newspaper readers. Which violates vertical tax equity. The question should be: how do we get the newspaper proprietors to pay, too? Perhaps UK-located assets (e.g. real estate and businesses) over a certain value should be subject to IHT even if the owner is not domiciled here? But, as you mention, assets held by trusts may be harder to catch.

My proposal taxes the actual gain, not some random part of it. What is your problem with that?

I’ve no problem with taxing the actual gain on people’s main homes. You could say I have problems with 2 things:

1) *not* taxing unrealized gains at death on second homes, BTL properties, and other assets already within the scope of CGT. I would like these to be taxed even if gains on main homes remained exempt. But it would be more important to do so, for consistency, if gains (including unrealized gains) on main homes were to be taxed.

2) excluding the main home from the estate valuation for IHT. Perhaps IHT can be replaced with something better; but as long as it’s there, this exemption seems inconsistent.

I get that the 2 things I don’t like to some extent offset one another. But not at all exactly. Some people would take this as an invitation to get into complex tax planning re CGT & IHT when deciding what property to buy/sell/live in. By treating all assets (main home or not) similarly, the opportunity for this tax planning disappears.

I note your point 1, but it effectively means abolishing CGT and I am not going that far here.

Re main residences, my proposal will increase tax due. Is that your issue?

I assume “it effectively means abolishing CGT” should read “abolishing IHT”?

I realize that you’re trying to come up with a list of relatively small reforms here, and the alternative approaches I’ve suggested are perhaps too big. Though I think the same may apply to your approach to charging CGT on main residences, too. Can this one really be done as a small reform?

No, I have no issue with your proposal for main residences increasing tax due.

On IHT reform generally, I am puzzled by the level of hostility some show to this tax. There is only one point that is often made against IHT that I think has much validity, viz. that it’s unfair because the very richest are able to avoid it. Perhaps the way to raise IHT’s popularity is to focus reforms on making sure that the very richest actually pay it, in full. Including actual billionaires. If they aren’t even domiciled in the UK, charge them on the value of their UK-located assets. If we could do this, it would broaden the tax base of IHT so much that we could also reasonably cut the rates it’s charged at.

I did mean IHT, not CGT

If you struggled like hell to buy a house in the South in 1974 and still live in it because you need to be near other family who need care and the cost of downsizing is simply extortionate its grossly unfair to dump the estate with IHT or indeed Capitol Gains Tax …

At no point have the owners earnt or paid more than 20% Basic Rate Income Tax and they most certainly are not wealthy now surviving on pension

Its not possible for such people to set up a trust and in any case there are taxes on a trust .

Hence IHT whilst claimed to only hit 3% of population those whose estates are stung cannot by any stretch of the imagination be considered wealthy

They simply struggled and went without and have cared for and maintained a house and garden they love .

So why why why should their estate shoulder the burden of 40%IHT

Tell me why the heirs of sauch peole inherit coniserabe unearned wealth tax free?

What is your logic for that when the sum in question will never have been taxed?

I would agree with Helen Jones on this one. I think there should be a level below which people can pass on property untaxed – unless the beneficiaries have substantial assets themselves. IHT reform or other reforms are needed so that say the heir to the Duke of Westminster cannot get assets of ten billion or so! Reforms have to be fair and proportionate.

They can – that is built into what I am saying.

Only a gain is taxed.

the gain should be adjusted for inflation and then taxed.

Tell me why it should be adjusted for inflation when that just puts significant amounts of untaxed pounds in some people’s pockets, but not others? On what basis do you justify the discrimination?

How is it discrimination to be taxed on the purchasing power ?? Discrimination against who exactly?

Discrimination against those who are excluded as a result

But you clearly do not care

I wouldn’t bother to reply if I was you

Wow.

I’ve just noticed how housing has come into this?

Thatcher has a lot of us salivating like Pavlov’s dogs when we think of houses as a store of wealth? My God. I though they were just places to live! Silly me!

It just goes to show what has happened to wages and pensions doesn’t it? And then rents. And how working people pay more of their income in tax than the wealthy?

What a mess. But no, we must not touch houses!! Oooh no!

I back Richard because I’m more interested in the effects that the uncollected inheritance taxes end up going?

Like – into political contributions to corrupt our democracy to keep inheritance tax low?

Like – inheritance is actually unearned wealth in a world that does not want to pay decent wages and support?

Like – being used as investment cash in goods and services that hurt us and our planet?

Like – being used to purchase and extract other people’s wealth in privatised public services and takeovers?

Like – funding ‘think tanks’ that peddle lies about economics, money and environment.

Like – adding to inequality?

Like – enabling tax avoiders to arbitrage taxes and go ‘low tax regime shopping’ in places that actually need more tax, creating competition between jurisdictions to effectively bleed themselves dry.

And finally, just look at what some of the people who have inherited wealth get up to will you, starting maybe with the right proper self justifying, self interested, self centred charlie we’ve got as king at the moment?

Thanks PSR. Appreciated

Havent got round all Richard’s – property tax/inheritance tax etc – but Danny Dorling seems worth worth considering :

https://www.dannydorling.org/?p=7352

on property/land taxing – and international comparisons.

He certianly is not going with Labour’s simple ‘we’ll build our way out of the housing crisis’.

Thanks

Stefan Collini has a piece on Tax in the new LRB – will send link when I get it

One obvious point is that the price of houses and land has increased massively, far beyond the rebuilding cost of most properties which makes Inheritance a much bigger issue than it was in say the 1970’s & 80’s.

Clearly if we were to make house prices closer to the historic average of about 3x earnings I suggest that IHT would be much less of an issue.

Secondly I suggest that we need to look at how we as a society can set up mechanisms that allow owners to sell there business’s on retirement and allow the business’s to continue trading as at the moment many small business’s dont survive the death or retirement of the founder.

I think the last is interesting

Isn’t that, primarily because those small businesses were not really businesses. Just jobs for the owners. And without the owner’s input there is no business. For example a small business offering tech repair. The business owner is the only one who knows how to diagnose problems properly and how to deal with them. They may employ a couple of people who work under their close supervision, but without the owner the work cannot be done.

Richard – another well developed approach. I like the rumination- “a progressive scale would make much more sense.” That adds to the politically feasible part and it recognizes the need to reduce inequality. Another such consideration would be an exemption level. Fewer people tax combined with progressivity, is much easier for politicians to sell.

In Canada everything is deemed sold at death unless there is a spouse. And everything in the tax deferred personal retirement fund RRIF is taxed at personal income rates.

However personal residences are left out. But of course the income properties, cottages, chalets … are included.

Question that have bothered me for a long time:

Is it possible to make a rough estimate of:

a) the total amount of sterling that exists across the world originating from the B of E and authorised sterling issuing banks?

b) how much of this is effectively removed from circulation by investment at any one time?

c) how much of this avoids taxation?

A) Yes. See money supply estimates.

B) I am not sure why you think investment takes money out of circulation. It is saving that does that. Savings data is available.

C) I am not sure why you think these issues are related.

Sorry, I thought investment was pretty much the same as savings in terms of taking money out of circulation

Not at all

Investment is active I.E. creating or building something

Saving is passive I.E. putting money in the bank, buying a share, or whatever.

At the risk of being in minority of 1…

If we want people to achieve their potential then it’s sort of up to them to make something of their lives and not their mums and dads job. They will “inherit” from them anyway albeit, if they are lucky, by being loved, valued, nurtured and coached. If lucky they will still have a massive head start in life.

So, inheritance – generally I’m against it.

Now I do value my dad’s marquetry pictures, and my wife’s uncle’s hand made furniture. But I particularly dislike the notion of a guarantee that some of the estate will be protected if people need care – the general taxpayer protecting someone else’s inheritance doesn’t sit right with me. I constantly have to remind my FA that my objective is to use my money for my old age and not pass it on. I think Bill Gates might agree with me.

So what about the stuff we have left over when we die?

(1) Property, as with social housing, if it’s your main residence when your parents die you can keep it (this is a change I have long advocated for social housing)

(2) Effects, yes have keepsakes, the rest to charity or the skip – we of a certain age have done this.

(3) Money, all society needs to do is recompense those who for no fault of their own have a poor start in life (the playing field will never be entirely level). Anyway my proposal would be something like this;

Remaining life expectancy x (the difference between your parents income and the average income – measured annually), if there is a negative result then treat as zero. If the estate cannot support it then the state should be in loco parentis and grant you that amount of money. If you are a minor this will be held in trust.

The older you are the less you get.

If the house is your main residence you can stay.

Otherwise the whole lot goes – each generation has a safety net and makes its own way in the world; the house becomes part of the social housing estate and the money to general taxation.

BTW this is only my opinion, in a holistic political economy policy would be worked out by negotiation (participatory) including a large proportion of randomly selected people (to make 1 persons view = any other view, and keep democracy safe). My personal views therefore would just go into the pot along with everyone else’s views. I may be radical but I have to be defended and advocated my views and reach an accommodation with everyone else; what I don’t do is go into a small group (party) then enter a competition to win control of the state so I can impose my view on everyone else whether or not it’s a true majority.

There is no chance of political traction for this

I work in the land of what is poossible

Of course I understand, surely the simplest approach would be (1) raise the threshold so its not an issue for “middle England” (2) close all the loopholes so that those with big estates cannot escape .

Point 1 would have the effect of stopping the inheritance tax avoidance industry which is massive so expect a lot of lobbying

Point 2 treating it as a capital gain as you suggest can be part of maki git inescapable

Regarding point 1. The cut off point is a big issue given house price inflation. I never understand houses as and investment (unless you are a landlord), a home is a home and if all houses are expensive you a relatively no better off. I assume your proposal is targeting when the gai becomes liquid and going to someone who already has a house – could also be seen as a windfall I guess.

Regarding point 2. It has been said that we will not get political change until the very rich start messing things up for the merely rich – which we may be witnessing.

Perhaps the narrative on the proposal needs to be clear i.e. its not that its easy and raises money thats critical but why its fair.

I do not accept your political logic