Earlier this week, I noted the problems with the management of UK companies by Companies House, the failed regulator that supposedly has charge of this sector.

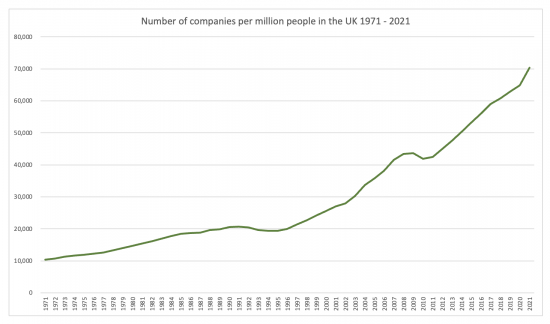

To put the issue in context, I plotted this chart yesterday:

Data is from Companies House and the Office for National Statistics.

The growth is absurd. There are now more companies incorporated in the UK each year (801,000 in 2022-23) than there are live births (fewer than 700,000).

There are a number of explanations. Tax is one of them:

Note the downward pivot in rates in the mid 1990s at the time the number of incorporation began to rise.

There is also an accounting dimension. As I noted in a 2014 report on the use and abuse of limited liability companies, the relaxation of accounting requirements has also had a major impact on this issue.

The 1967 Companies Act required that all companies place their full accounts on public record.

The 1985 Act allowed for abbreviated accounts to be filed.

But, more significantly, between 1993 and 1999 the audit requirement for most small companies was abolished, massively reducing the cost of running them and basically leaving the whole sector unregulated since Companies House does almost nothing whatsoever to enforce UK company law. That, followed by some tax folly by Gordon Brown early this century, sent company use ever upward.

The chance that a change promoted by low tax and low regulation has not been significantly abused is a long way from zero. That is my concern.

This is an issue I will be returning to because the currently proposed reforms by the government are far from adequate.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

I agree something fishy is going on here. It never ceases to amaze me that the first thing these new small companies do is buy themselves a new car that also doubles as the family vehicle.

In faiurness, most don’t

Really?

When I think about the people I know who have ‘gone solo’ a new vehicle was always present (an SUV usually) after the inception but if you’re operating with more knowledge than me then fair enough.

Company cars by and large make little tax sense these days…

810,000 new UK companies each year.

Companies House needs an expert system that can categorise such companies & their directors. Some (a minority?) will be genuine. Others (many? most?) will be vehicles for nefarious activity of various sorts. There is no doubt that there will be patterns and automation/computers could easily identify such patterns. Leaving the open question: what to do in the face of gov’ laisser faire.

There are reforms in progress

If the law passes directors will have to prove their identities

But the chance of any real enforcement by an agenncy that does not think it has a regulatroy role is limited

We have a long way to go to reoslve this abuse which politici9ans bizarrely think is a sign of economic virility

If you want to get an idea of the crazy registrations going on at Companies House, can I recommend following Graham Barrow on X (formerly Twitter) @graybrow53

Graham’s The Dark Money Files is an excellent and eye opening podcast. He recently gave an example of 8 different companies being registered by 8 different people at 8 different addresses all in the same postcode and all describing the subscriber as “Engineer”. There is engineering going on but not in the traditional sense!

Also I would think a lot of companies were set up to procure bounce back loans for non-existent businesses.

When I worked in local government on recovering rate debts setting up limited companies and then putting them into liquidation was a common tactic to avoid paying business rates. There were certain accountancy firms which would facilitate this and would get annoyed when I turned up at creditors meetings. Of course these companies never had any assets

Agreed

I saw that

The last flat I bought I put through a company, so yes it was solely for the purposes of tax efficiency.

It would be much better if the taxation of individuals and ltd’s was in line so I didn’t have to go through this charade. Structuring a company, keeping accounts and doing filings is ultimately a deadweight loss on the economy.

With enveloping that would seem to have been a very odd choice

I am far from a business or financial expert. I am a victim of a failed funeral company, and after reading this article and your article about ‘freeloading’ it seemed to ring many bells about what I discovered from looking at company house with regard to the number of companies the directors of these companies have had (some 30 plus) which failed, prior to accounts etc… and after asking them questions about how many companies someone can set up and fail before alarm bells ring, was told basically… as many as they like, no one looks in to it. This particular company had 19 million at one point, and no one seems to know specifically where it all went, but it was not on funerals, the trust fund the money was meant to held in …. well, it appears it wasn’t.

That is an industry in urgent need of better regulation.

I am sorry you lost out.

Introducing more regulation is all well and good but without expeditious enforcement it may overall have limited effect.

Simply making it a little bit harder for fraudsters to operate might cut out a few low-level operators but it is doubtful it can deal with most of the sophisticated ones who cause material damage.

Often tweaking systems means the fraudsters react and adjust to outflank the new regulations which are an occupational hazard. You then have to play catch up with the new environment you have created by deciphering what the fraudsters are now doing. Then train people to adjust to the new ways the fraudsters are operating.

However, if you are not going to proactively and routinely target the sophisticated fraudster, it risks being sticking plaster stuff in addressing the low hanging fruit cases. To have impact and change behaviour proper resources are required for enforcement and reform is needed to the justice system that currently moves at a rather pedestrian pace.

Enforcement backed by automatic information exchange of data from banks is key