Ben Broadbent, deputy governor of the Bank of England, gave a speech this week in which I agreed with some (but by no means all) of what he said.

His argument was summarised in this statement:

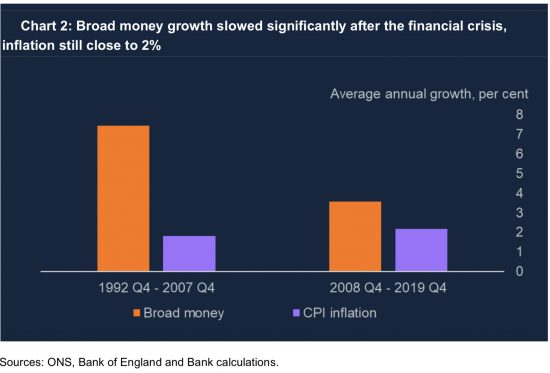

Certainly the very strongest claims – that QE inevitably leads to rapid growth of commercial bank deposits (M4), on a par with that in the central bank's balance sheet; and that this, in turn, inevitably leads to excessive inflation – are not well supported by the evidence. Broad money grew more than twice as rapidly in the first fifteen years of inflation targeting (when there was no QE) than in the decade or so after the financial crisis (when there was lots). And average inflation, in both periods, was close to 2%.

In effect, the argument he made was that the creation of new money by the Bank of England under cover of the quantitative easing process, did not result in inflation.

He developed this thesis using several charts:

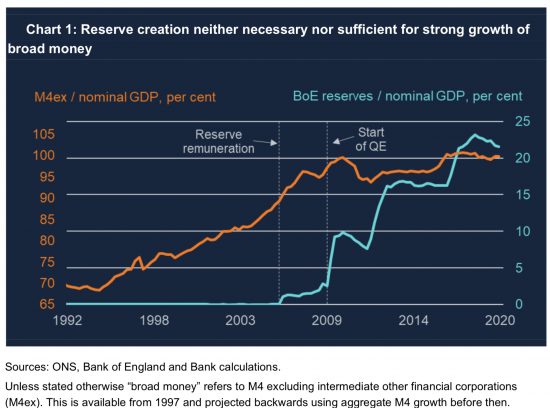

The argument made, based on this chart, is that the growth in central bank, base, narrow or reserve account money (they are, effectively, all the same thing, with all of it being constrained within the Bank of England inter-bank settlement cycle through the central bank reserve accounts) is not related to the growth in commercial bank or broad money, which is what is actually used in the economy in which we all operate. It's a notable and appropriate suggestion.

Broadbent reinforced the claim by suggesting that the global financial crisis changed the pattern of money creation, but doing so did not result in inflation:

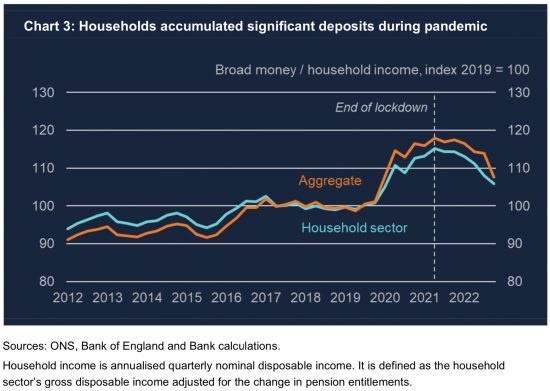

The point he then noted was that the impact of Covid was that some in society did save using broad or commercial bank-created money:

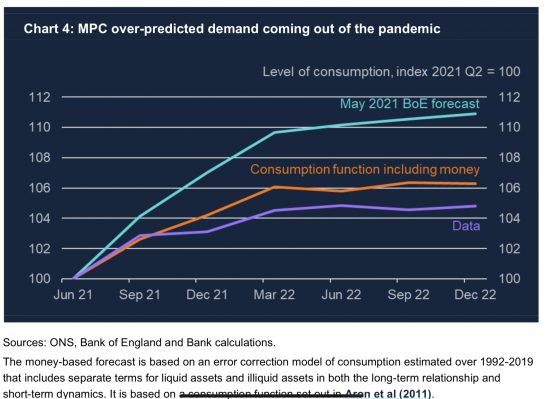

What the Bank then expected was that people would then spend that pent-up money. This is what those who claim the QE created inflation also suggest. However, as Broadbent notes, that tendency to spend was much smaller than expected:

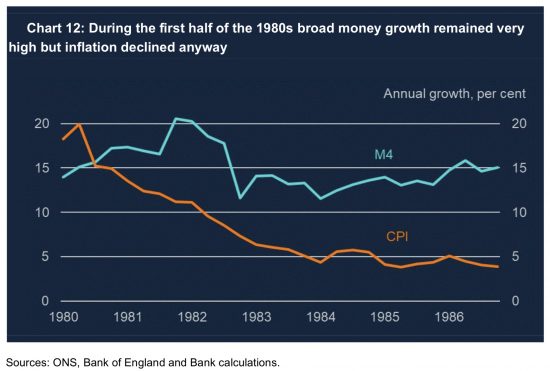

Broadbent then used a New Keynesian, and so deeply neoclassical, explanation for what did happen in the macroeconomy. From this he concluded that, firstly, it was external shocks that created this inflation and, secondly, like Huw Pill, he thinks we must accept that we are worse off as a result. I do not agree with the reasons he gave, but what I do agree with is his conclusion that central bank money creation, let alone broad money creation, is not closely (if very much at all) linked to inflation. His Chart 12 provided support:

Money supply growth was high. Inflation was not. At the very least, the velocity of circulation of money dropped dramatically. The obvious explanation for that is growing inequality. He did not say so.

Where I do agree with Ben Broadbent is that there is no obvious evidence that QE did in any way result in inflation. I think it is time to dismiss that argument.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

House price inflation = good caused by excessive QE

Everything else inflation = bad because now nobody can afford the stupid QE experiment of massive housing inflation.

Simple thankfully Andrew Bailey and Huw Pill are just as transitory as inflation.

Actually, QE was not used to promote house price inflation. Specific funds were advanced to achieve that

Did the QE not end up supporting the commercial banks balance sheets thus allowing them to lend larger sums to support the housing market. I thought the govt help to buy schemes encouraged house builders to put their prices up and the banks were then able to lend these higher amounts due to very low interest rates and decent reserves.

But there were specific schemes to do this is my point

Exactly what Martin D said. This money was used to boost up house prices. If it was not meant for that then Andrew Bailey should have had a word with the commercial banks and made sure that this was stopped.

Or should we be more scared of our current situation based on another fund that has caused unsustainable house price inflation whilst QE was surpressing everything else until the Dam broke?

you are saying we are yet to see the problems that QE will cause and this other fund that caused this current crisis is nothing compared to what is coming?

Well over £100 million was provided by the government exactly for housing market lending.

And as for the rest of your comments – if they related to some evidence base (which like the first they do not) it would help

Unless you add to debate you are not useful here and right now I am not sure what addition you are making bar offering right wing scaremongering

What this looks like is a banking sector floundering to explain phenomena it has neither the theory nor the tools adequately to explain, and is falling back on a fragile base of understanding to rationalise the inexplicable; presumably to defend a plausible air of authority they are unable to justify. It is rather a mess.

To some extent, yes

The theory in this was weak

The Longer Andrew Bailey stays in his job the worse off people feel.

I can produce a chart to back this up.

My understanding of QE is that it was distributed badly because it was aimed at bank stability only – it did not result for example in (say) loans to consumers at lower rates or anything like that to help recover the wider economy.

It filled pot holes in banking’s accounts and got the money moving again. It might have also shored up the wealthy and helped the value of their assets.

Which is why I think Broadbent doesn’t want QE to be associated with inflation – so that the state can continue to bail the banks/rich asset holders. It’s also a tacit acceptance therefore that 2008 could happen again – in fact it is isn’t it but on a smaller scale.

There was no QE for ‘main street’ as the American public noted – so how could QE possibly be associated with inflation anyway?

The QE did not permeate throughout society at all, because we had austerity whilst the people who caused 2008 got QE.

That is why I think that you are right.

Inflation happened after QE. It’s how inflation is measured that is wrong. And that’s convenient for central banks and government politicians because historically it makes them look financially responsible when all along they have been anything but.

It’s delusional to think that if one prints more money inflation will not result (unless you rapidly reverse that QE). One can dress up the numbers with economic theories, charts and financial qualifications until the cows come home. But fundamental logic cannot be denied: if there’s more printed money out there in the real economy, prices somewhere go up (or the value of our currency goes down, ie inflation by a less conventional route)

Property prices have ramped up significantly more than inflation (in terms of how inflation is measured) for many many years while the pound did not sink significantly. In other words that QE money has been chasing property (and stock market assets).

Those house price rises have been conveniently blamed on the lack of availability of housing. Houses are normally bought with borrowed money. House prices will only rise above inflation if there’s more money available to crank up the price. And that’s exactly what lenders have facilitated.

You can’t buy a house if you can’t access money, or enough money, to buy it irrespective of shortages. House shortages will play a part, but the significant rises are due to cheap money.

QE has made cheap money possible for lenders. End of. (Since the days of Thatcher, Conservative governments have been selling the notion of owning your own home. While this has not necessarily been a bad mantra, the fiscal side of this has been managed in a reckless and irresponsible way by governments on both sides and we are now paying the price, along with other failed economic policies, through high inflation. It was bound to happen sooner or later. It’s been like an elastic band. The tension has been building for decades and politicians have conveniently ignored the warning signs because it would have been politically unpopular to make the real necessary fiscal decisions. I mean can you honestly believe that Alastair Darling did not see the 2008/9 crash waiting to happen? If he didn’t, he was sleeping on the job. I foresaw it and that was just reading financial literature.)

Ludicrously low interest rates have allowed banks to lend QE money at significant wage multiples for years and allowed governments to pretend that our economy is healthier than it is. Assets and overtly large cheap mortgages have soaked up the inflated money, preventing that money getting into the rest of the economy to allow a more normal economic cycle.

And while wages and prices of most other goods and services have not registered significantly in the current measurement of inflation in past years pre the Ukraine war, a huge amount of that QE money is now stored as debt in the property market (and stock market) reflecting the view of growing inequality as asset rich organisations and individuals capitalised from the flawed application of QE approach.

The real inflation genie is now out the bottle because real assets which we import from elsewhere in the world, assets which we all need like food, commodities etc, not overinflated housing, have risen in price (relative to the devaluing pound) suddenly.

But our overvalued houses are worth nothing to everywhere else in the world That has exposed the folly of tying value into fixed to the ground assets in your own country through QE debt, assets which we cannot export to combat domestic inflation. Had we channeled QE into real wealth creation/exporting/growth in wages over the last 10 years in particular, while keeping interest rates higher, we would not be seeing the sudden domestic and stubborn rise in inflation and poverty to the extent that we are now seeing. I’m not saying we wouldn’t have seen a spike in inflation, but because the value of the pound would have been higher, it would not have been so severe.

Mortgage and asset holders are and will continue to feel the short to medium term pain as wages now rise to offset necessary increases in responsible interest rate rises put in place to try to control inflation. In other words wages should have been rising faster than they did, for the last 10 years in particular, but didn’t have to because of cheap and copious amounts of QE money being channeled into assets and the value of the pound staying artificially high, just delaying the inevitable inflation we’re seeing now.

Nothing is free, and the blatantly exuberant borrowing and spending of western economies over the last 20 or more years is finally coming home to roost.

You really need to understand money

I hate to say it, but it is clear you don’t

You claim it is delusional to think QE could not create inflation

But when run with austerity you wholly miss the point

I am still wondering why I am posting your comment. I think I must be generous today

QE was invented to stop massive deflation why else did they do it. However they have done it for too long and like most Central bank policies especially the experimental one like this one it over shot. We have had too many Zombie companies for too long, this causes inefficiencies and bottle necks and this has most certainly contributed to inflation. More recently Chinese lock down caused bottle necks and the factor certainly news papers do not talk about is onshoring by all Western countries. This process will take a few years and 2% inflation target is unrealistic in this economic evolution for now- Furthermore Chinese working population has been reducing since 2012 this has caused some wage inflation which has affected the world and will continue to do till India steps up properly.

As Danny Blanchflower and I note, QE was intended (after 2009) to counter austerity

Since austerity continues we still need it

But an Austrian economist – who else uses the absurd term ‘zombie company’? – would not understand that

I am not a scholar so I look for simpler solutions .I find it better to measure a person or organisation by what they do or do not do and not what they say..example .. transitory.

The B of E print and sign a promise they can’t keep. In collusion with govt. They raid and borrow on behalf of the public purse.

In 1916 two Sovereign pounds paid a tradesman for a week.

In 2023 the same two Sovereign pounds would approximately do the the same .

Instead We require £800 of these “earth pounds or token pounds” issued by the Bank of England on behalf of Govt to pay that same wage because they have inflated its purchasing power away to almost nothing.

They have even changed the definition of inflation from the original “increase in the monetary supply”. To suit their cause… Anyone for QE?

Try not to deal with promise breakers.

I know my understanding is naïve but my wallet is thinner as I pay £1 for three miniature Mars Bars today. Half a week’s work in 1916.

We live in a complex world

Pretending there are simple solutions is the basis of populist politics

That generally makes them a bad idea

Probably trying to justify the interest rate hikes.

Housing loans were over £300 billion in 2021 for e.g. so £100 million from government you quote as explanation for a market bubble seems disingenuous. The graphs omitted so many factors; technical innovation and market liberalisation, globalisation, all anti inflationary and supportive of an increased money supply.

Disingenuous appears pretty strong

You do realise that banks could create their own money too?

So the way I see it but it doesn’t seem to have explained is that the covid furlough QE for a majority was not an addition to money supply – it was there to make up companies that weren’t paying wages Bcs the economy (for a number of sectors) stopped – in that sense this QE was purely replacing a money supply lost – how could that be inflationary in the first place?

Correct

I think it is perhaps money that was not earned and I said this before I was given money to pay others. Money I recieved never really directly helped me it just paid for my usual outgoings whilst it was dropped by 20% income and taxed by 20% so a 40%+ loss It meant although it kept my debtors sweet I still needed to work to keep myself from losing the plot and also so I had nominal income money and there was no shock in money supply.

This meant what I normally did in the economy which was productive was closed and I worked doing something else that could not sustain my standard of living was not particularly anywhere near as productive and I waited to go back until it opened again to do something productive.

I don’t think we can however ringfence house prices off what we have seen is a rise in house prices due to QE but when the whole political illness struck the Furlough QE accelerated this faster and further but also because of the “Work From Home” and how that vhange also radically impacted many business revenues and commercial real estate beyond any recognition,

Richard Murphy, it is a mathematical certainty that debasing a fiat currency will, eventually, lead to inflation. Basic maths for anyone competent. 2008 QE ended up in banks which resulted in a 40% increase in the value of stock markets around the world. It was essentially ring fenced but very clearly caused the rises weve seen in recent decades. Look at QT axnd recent effects.

Yes, a different mechaniism was used to inflate house prices, but, it is still the expansion of the money supply, just not via the sale of long dated bonds. Watch this space when the QE of 2020/1 finds its way to the coal face. It just depends where that money finds a home.

Youre understanding really does not warrant the attitude you display in your responses. you wouldnt last 5 minutes debating this with competent economists.

It is a mathematical certainty that if money creation and the velocity of circulation are perfectly inversely correlated and real trade is a constant you are wrong using a theory you no doubt subscribe to.

Please don’t call again