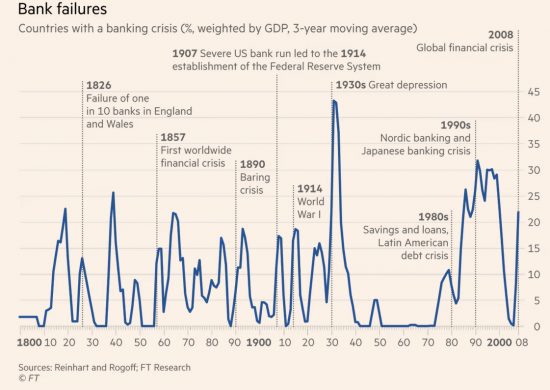

This chart was in the FT yesterday.

I note it because there was one era when bank failure virtually disappeared. It was the post-war Keynesian period. How very strange that we dumped that in favour of instability. Could it be that those who profit from chaos could not withstand the good order it supplied?

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Credit controls, that is why we had stability.

Monetary policy works by increasing/reducing the supply of credit to the economy which, in turn raises/reduces activity which ultimately influences inflation (well, that is the theory and it might even be true much of the time).

Since the rise of neo-liberalism and the fetish for “markets” most governments around the world have controlled the supply of credit by raising/lowering interest rates – the idea being that governments should have no say how credit is allocated… merely set the price. We can see the result.

Using Credit Controls allows:

(1) the overall supply of credit to be controlled directly rather than through the uncertain “price mechanism”

(2) new credit to be directed to useful areas and away from overheating areas

(3) and generally gives more flexibility in policy making.

Agreed

I like the argument. In 2023, after forty years of neoliberalism, what is the mechanism?

The easy question…..

Keynesianism: is that where you restrain government spending during periods of above average economic growth even running surpluses, and overspend when the economy is in recession.

Should have tried this in the 2002-2019 period.

You think 2002 to 2019 was one era?

What planet are you on?

Starting work in the 1970s and being an early riser I soon became acquainted with the daily Radio 4 report on the state of the Markets. The Fruit and Veg markets that is, (it may have included Smithfield and Billingsgate but it is the fruit and veg I remember). Constant worries in Birmingham about the state of the Evesham asparagus crop seemed a frequent topic.

How much healthier would the economy and the British people be if that was still the case.

Instead, in roughly the same time slot the BBC now broadcasts 15 minutes about markets, only now it is all about Banking and Speculation and with complete contempt for the truth and the English language this is called the Business News.

FarMing is earlier …..

I couldn’t be sure Richard that why I framed it like I did.

My memory is that I remember it being introduced by Jack de Manio or one of the other old-time Today programme voices but I would not bet money on it.

There is a name from my past

Jack de Manio…..

I cannot resist it, Richard.

Far Ming is a very beautiful typo…

Ha ha….

I’ll see your Jack de Manio and raise you Horace Batchelor.

You’ve got me there

Horace Batchelor … from Keynsham

Spelt K E Y N S H A M

See also Bonzo Dog DooDah Band

That should have lost everyone but those of a surrealist frame of mind!

You are right

A remarkable chart. Most market players (in just about any market you care to think of) hate market stability since this reduces the possibilities for profit. A cursory glance at stockmarket gyrations tells you all you need to know. Energy markets – ditto. Looking carefully at the chart, it would seem that instabiulity took off following the end of Bretton-Woods.

Market instability will work against the great (greatest) project of our time: de-carbonisation. You need low & stable interest rates for that – because WACC (weighted average cost of capital) has a big impact on the cost of energy. An unstable finance sector (it ain’t an “industry”) is the very worst thing you can have. WACCs for renewables used to be 5%ish, I dread to think what we are looking at now.

I am the son of a father whose life was turned upside down when his engineering firm was bought out by some American investors and asset stripped into oblivion in the 1970s.

The chaos you describe, enabled by the stock market and the banks has always been to me just a legitimate means of daylight robbery and chaos is part of their weaponry.

I remember the period of the ’70s when this chart starts to rise again. It was when we came home from work but had trouble opening the front door because of all the junk mail trying to foist unwanted credit cards on us.

Prior to this I remember that credit cards were the American Express cards that only corporate business people had, ordinary people were not eligible.

The average joe in the street may have had hp agreements for a new three piece suite or washing machine otherwise you saved up, you couldn’t do your weekly shopping on tick, like now.

Isn’t Neoliberalism a blessing, for the lenders that is.

Today If you don’t need a credit card and use it, you pay it off each month, no problem.

If you can’t afford it but use it anyway, you get they privilege of paying nealy 35% interest when you can least afford it. Usury in action.

Tom

Pensioner in despair for the younger generation(s).

Well observed. I take it the little spike in the late 1970s is the ‘secondary banking crisis’?

Commercial banks simply cannot be trusted to put the security of the system first. The graph is illustrative, and all the spikes merely show that even in a pre-digitial, pre-global world central banks could not prevent the resolution being a bumpy ride. Spool forward to today. The defence of the system of commercial banking we posses,s is that in our well regulated system the risks are low, and the central bank, acting promptly, can ensure the stability of the system.

This, I believe is no longer a sustainable argument. The modern development of derivative trading, shadow banking and the sheer speed of the digital age (and I am not even thinking of developments in quantum or AI driven derivative trading with operating peeds in nanoseconds – somebody always wants to be ahed of the game; it was said Rothschild’s greatest success was having the fastest intelligence, pre-arranged, on the outcome at Waterloo); now means “prompt” can never be prompt enough to secure the system before disaster strikes. The muddled arguments about CBDCs being presented by the BoE are merely illustrative to me of a deep intellectual problem the central bank has not solved. Meanwhile the real world of commercial banking, and the innovative use of time to make profits, waits for nobody.

Perhaps the real lesson of SVB is that, unlike Northern Rock, depositors are no longer prepared to hang around in a queue to take their money out. They are more acute. Which means the bankers will innovate something else to stay ahead. And so it goes on.