I was approached by David Burke of the Daily Mirror yesterday to comment on this data in the context of the new pension tax reliefs supposedly created to induce doctors who had retired after their pension pots exceeded government-set limits to return to work:

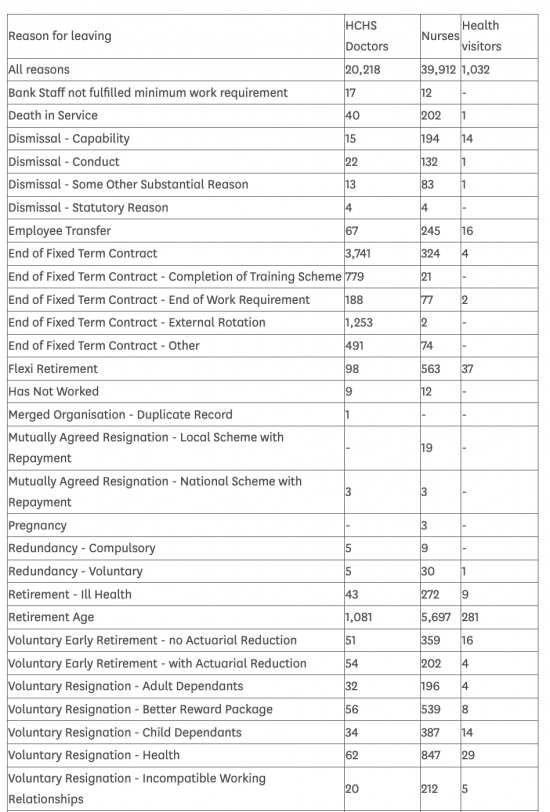

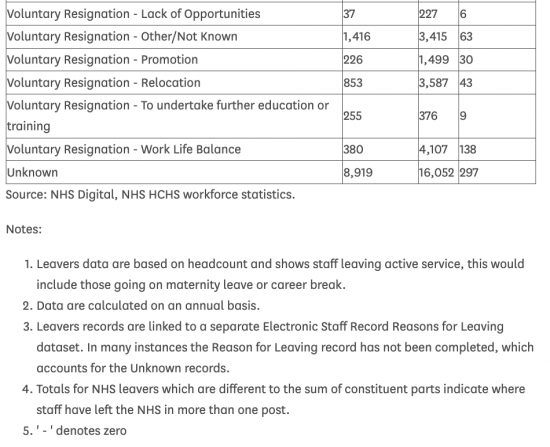

The data provides no support for the argument that doctors are leaving the NHS because of their pension arrangements. They may be, because 8,919 out of more than 20,000 departures are for unstated reasons, but pension matters are only referred to twice with regard to actuarial adjustments, and there are only 105 such cases in all. That figure is insignificant in that case.

As a result, I pointed out that:

If [the government] don't know how many doctors are retiring for this reason, why did they change the pension policy for everybody to keep 105 doctors in the NHS?

The Guardian also picked up the story, taking quotes from me straight from The Mirror:

It looks like they used the fact that they know doctors are leaving for this reason to provide a pensions bung to the wealthy.

They haven't got an evidence base for this policy, and that's good enough to say it can't have been for retiring NHS doctors.

Let's put it another way. The government saw an excuse to increase tax giveaways to the very wealthy and took it. £1 billion could be found for them, but not to settle wage disputes on a proper basis. You cannot make hypocrisy on that scale up.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Indeed, a sledgehammer to crack a nut….. but a sledgehammer that conveniently helps a few friends.

One could just pay older doctors with already good pensions their salary but without a pension contribution. Not sure of the details but along the lines…. “if you are over 50 you can get £100 pay with pension contribution or £110 without”.

As you noted, this IS an issue for some folk because they are getting demands for cash today for the fact that the Present Value of the future cash flows exceed some arbitrary number. Surely, this could be ameliorated by allowing the tax due to be postpone until cash is actually received under the pension.

In short, it is a version of “never let a good crisis go to waste”.

There were so many ways to solve this, all of them easy

But the option of a bung was chosen instead

The pensions statistics up to 2020-21 are here. https://www.gov.uk/government/statistics/personal-and-stakeholder-pensions-statistics/private-pension-statistics-commentary-september-2022

See section 7 for the lifetime allowance.

The numbers have been going up (in part due to the allowance being cut in steps from £1.8m in 2011-12 to £1m in 2016-17) but as things stand something like 8,000 lifetime allowance charges are reported each year and about £400m paid so about £50,000 each on average.

How many of these people are doctors? And even if they are all doctors, is this an acceptable price to get them back to work? I don’t see many other public sector employees being offered £50k bungs.

Thanks

A few more points.

A person paying the new annual allowance of £60,000 into their pension for say 50 years would accumulate a pension fund of £3m (without growth). Or indeed they could get a fund of say £1.2m after 20 years and just retire early.

The annual allowance tapers away for anyone earning really large amounts – tapering to £4,000 for people earning over £240,000 as things stand, and soon to be tapering to £10,000 for those earning over £260,000. So the increased annual allowance really only helps some people in a relatively narrow band of income, who have enough earnings to make the contribution (or have it made into an occupational pension on their behalf) without the annual allowance being tapered away.

A person can contribute more than the annual allowance if they are not bothered about paying marginal tax on the excess (that is, they lose the tax relief on the way in) but the funds continue to grow within a tax-free wrapper. That might be attractive in a regime without an overall lifetime allowance, particularly given the potential inheritance tax exemption.

But I’m, really struggling to see that many people might be motivated to come back to work by the prospect of making a few more years of pension contributions.

To put this in context, anyone earning over £183,000 was in the 99th centile for income in 2020-21. The top 1%. And that is only counting the half of the population that pay income tax. So that is 0.5% of the *people* in the country. If is really extraordinary that we need to throw money at this thin and already comparatively wealthy slice of the population.

Agree with all that

And remember pensions are just savings

They can be done without tax incentives

“And remember pensions are just savings”

It is a very strange kind of saving in that you pay tax when you take your “savings” out. Unless you get some relief when putting money in it can be a way to double tax the same income.

You might gain some tax free growth and even the ability to draw out a lump sum, but unless you are getting the relief on money paid in you will need a very substantial amount of growth to avoid being automatically worse off for your contribution.

The best approach would be to limit contributions rather than leave people such as doctors in a situation where they are unable to control contributions made by an employer and they then receive a penalty which in some cases is higher than the amount they earned for doing so.

Most savings in the U.K. are tax incentivised

Pensions are normal, not exceptional

But £55bn pa is an absurd sum to subsidise them by

And they remain ‘just savings’

My goodness – the figures are staggering.

Thanks for sharing.

How about removing the biggest bung for the wealthy namely property being free from CGT. If we are to make homes more affordable to more people then this tax break to the wealthy should be removed asap.

It look like thousands of NHS staff are leaving because of short-term contracts. If consultants already have a £1 million + already in their pension pot they are still wildly above the pension levels of the rest of us. To endure the present stress levels of another few years at work is clearly unnatractive for them.

Do you think they earnestly believe that what they are doing is ideologically the right thing to do for society (as opposed to cynically abusing their power for the interests of their own class)?

In other words, do they think neoliberalism is right and it works (regardless of the evidence to the contrary), or do they know it doesn’t but creates an effective smokescreen for a deliberate and planned robbery of the public good?

I call into evidence Hanlon’s razor: “Never attribute to malice that which is adequately explained by stupidity.”

Can this be adequately stupid?

They think we are stupid

Actually, they are

But they have grabbed power and we let them. So they’re right: we are stupid

Interesting this information came out of a question from Streeting given just six months ago he said he’d do the same as the Tories: https://www.theguardian.com/society/2022/sep/03/doctors-pensions-labour-would-abolish-cap-says-wes-streeting.

It’s really hard for them to separate themselves from the Tories when their opposition to Tory policies are along the lines of we’d reverse the cut but then apply it to a select few people to stop them leaving their essential jobs, even thought they aren’t leaving because of the cap.

It’s easy for the Tories to take your policies and add their spin on them when your policies are being designed to appeal to Tory voters.

Streeting has since clarified that he was talking about a bespoke exemption specifically for doctors which might cost a few tens of millions, not a billion.

There are other alternatives, such as allowing doctors to opt out of mandatory pension contributions.

I expect most of the problems could be solved by reversing the almost halving of the lifetime allowance in April 2012 and putting it back to £1.8m. Annuities may be out of fashion, but with annuity rates currently around 6%, that equates to a pensions income of over £100,000

But if doctors are not leaving because of the lifetime cap then neither change will make a difference, and we should leave the cap as it is.

Agreed with the last

I seem to be alone here in thinking that the LTA did need raising. Not only was it at a level which affected some ordinary salaried jobs, it had different effects according the type of pension scheme someone was in (DB or DC) which has no logical basis. Far better to limit the tax relief using the Annual Allowance, and it was unnecessary to raise that as well.

I think that incentivising pension saving is a legitimate thing for governments to decide to do. But if they are going to do it they should do it fairly, and I would prefer them to limit tax relief to the basic rate taxable income (so an AA of the basic rate band, currently around £38,000). Any pension contributions beyond that would come out of taxed income – but importantly be taxed at source in the normal way, not triggering unexpected demands.

As you say, pensions are just a form of savings, albeit with some limitations on access. That being the case there is no reason why they should not have the same liability to inheritance tax as any other savings assets of the deceased. Its only apparent purpose is to provide a tax loophole for wealthy people able to organise their finances to exploit it.

I think it is true the LTA has been a concern of quite a number of doctors approaching their sixties. While those that have gone for complete early retirement may be small, others have adjusted their working hours or their contract. Several consultants known to me have technically resigned before hitting the LTA but then taken a new non-pensionable contract to continue working; they would presumably come under the 8.919 “unknown”. The fear of these doctors is getting a tax bill out of the blue that they couldn’t anticipate and hadn’t budgetted for – these are people who have happily managed their tax obligations over decades by being in an occupation where tax is removed at source by PAYE.

You have to answer a single question, Jonathan

Why is it more important to subsidise the wealthy, as this measure does in large amount than to help those in real need in small amount, which is what the same government does

If you can answer that then you have a case. Without an adequate answer to that there is no case for increasing the LTA

What was needed was a way to not peanlise people for past savings, and to let them carry on outside a pension fund, enjoying the benefit pension membership would have otherwise cost their employer

I pretty much agree with what you write.

What I was trying to say, though perhaps not very elegantly, is that it is a legitimate political decision to tax in ways that promote what they see as desirable objectives. This should (in my opinion) include reducing wealth inequalities, and regional inequalities – and encouraging saving for retirement is reasonable to include as such an objective whether or not you personally agree. The issue is to do so fairly.

Having a Lifetime Allowance created the disparity that it was – when interest rates were aroung 0.5% as they were recently – equivalent to a much higher DB pension than a DC pension based on a similarly valued annuity (I haven’t checked the current situation). I see no fairness in that, given employees don’t have a choice about their occupational pension scheme. However I completely agree that if tax relief is used to promote pension saving it shouldn’t be used in ways that disproportionately benefit the wealthy, that is why I suggested the LTA be replaced by a modest Annual Allowance with relief available only at the basic rate and any pension savings still existing at death to be subject to IHT like any other savings.

Thanks

I think the sensible solution would be to allow doctors to opt-out of the pension scheme if they have reached the LTA, perhaps with a 10% additional pay.

I believe a number of doctors might be affected based upon the fact that a DB pension scheme calculates the LTA based upon 20 times the accrued DB Pension. https://www.gov.uk/tax-on-your-private-pension/lifetime-allowance. So if the had an accrued pension of £53,650 any additional pension would be taxed at 20 X Increase in Pension X 0.25 or X 0.55 if taken out.

I believe the NHS pension accrues at 1/54, so if a consultant on £108k, who has reached the £53k accrued pension cut-off, works an extra year they would pay £2k X 20 X 0.25 = £10k tax.

This may well affect a small number of highly trained / paid consultants, so this is a sledge hammer to crack a nut and a simple opt-out would have sufficed (or even a small increase in LTA).

The disgusting thing about removing the LTA altogether is that pensions will now become a vehicle for very wealthy people to shield money from inheritance tax.