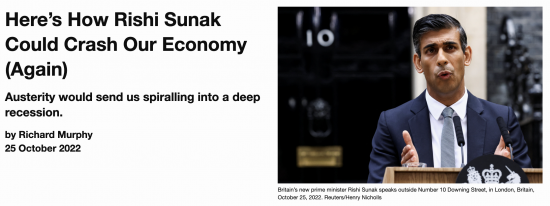

I was busy writing elsewhere yesterday, with four articles written for other media.

Two are out. One is on Novara Media:

I concluded this one by saying:

The other was on AccountingWEB where I was asked to write my fantasy budget. To quote a couple of bits, I suggested:

I added:

As to my proposals, go to AccountingWEB to read them.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Brilliant alternative budget Richard. I wonder if Starmer will read it? (I know Sunak won’t).

If Starmer does read it, will his neoliberal spectacles prevent him from understanding it?

Well if you are happy seeing sterling at 0.8 to the dollar and the inflationary consequence then its spot on.

Why will it be at 0.8 to the dollar?

Explain?

if dollar yields 5% and the fed are fighting inflation thereby protecting purchasing power it is more attractive to hold than pounds yielding 1% where the money supply is increasing and where controlling inflation and protecting purchasing power is not a priority. This applies to bond investors at all points of the yield curve. Any US entity receiving pounds in trade will immediately convert back. This picture will be mirrored across virtually all FX markets. As a consequence inward investment will be affected. Add to that the inelastic demand we have for energy in dollars then the inflationary consequences are obvious.

So you think that is enough to influence value, and real trade is not?

What a worrying state of play

I disagree with you. There is not enough hot money to actually drive that change

Inward investment is not “hot money”. Nor is institutional and pension fund asset allocation. You ideas would crucify sterling and heap more inflation misery on us all.

You think millions unable to afford homes and children without food is better?

What world do you live in?

“You think millions unable to afford homes and children without food is better?”

Wow.. where are these millions of people. And i personally don’t want to have an economy like Turkey…

Just read the news

I have one question. If IR’s were reduced to 1% what would be the likely effect on house price inflation? I assume mortgage rates would then be reduced closer to the 1% figure than they currently are. I just fear that we are a country that uses low IR’s as a good old excuse to keep up massive house price inflation. The history of the housing market of the last 40 years shows this to be the case. Restraint is not a word that the participants within it, i.e. the banks, estate agents, builders or sellers of property understand. Without a credible policy to create more affordable housing or a policy that in some way restricts house price inflation, in isolation low IR’s will just inflate the current bubble ever higher. That’s what history tells us.

We can reduce house prices by reducing the multiples of income allowed for mortgage loans

We do not need to crush people financially to do that

I think this is a key point – interest rates are not the only way to control credit creation. We need methods to differentiate between productive and unproductive lending. The whole thrust of banking regulation over the last 13 years has been about making banks safer and taking collateral has been central to that…. without any thought about how that might impact the supply of credit to the real economy. (One could say that the taking of collateral has delivered some collateral damage!). Banks need to be encouraged to favour lending to SMEs over mortgages.

With regards to imposing a 1% policy rate I am not so sure. First, I think it is too low – with an inflation target of 2% I would happy with 2% for short rates, 3 – 3.5% for long rates (although with a sensible system of credit controls I might be persuaded to go lower). My fears are that lower rates would put upward pressure on house prices and, less importantly, downward pressure on GBP. Second, I think many at the BoE know raising rates is not a great idea but feel forced into it by being blamed for high inflation (by the government wishing to blame anyone for everything). I think a more conciliatory and a co-ordinated approach would be better than picking a fight – I think you might be surprised at their response.

I have learned you deliver the shock first, the reasoned arguments after wards on things like this

We are moving in the same direction.

My problem here is believing that banks have the skill set to make such judgements effectively and prudently. Apologies, but my first thought was a metaphorical snigger. Outside the BofE charmed dealer circle of bond management and standard institutional passing the buck from banks to investment and pension funds; in the ‘commercial’ world, the commercial banks have long relied on using property as the almost only collateral that interests them (it really couldn’t be much easier for them than that), and they still spectacularly fail on an epic scale, with monotonous regularity.

What are the grounds for your confidence thay can do this, it requires real skill sets, not just in the technical process, but the economics of business, and the personal psychology; the judgement of people? Frankly, I think it is beyond them, without blowing it spectacularly. In my business experience, I rarely saw it manifested in the executives I met. Actually it is more likely they just will not lend; the only risk free option which they will move toward, even if shuffling crab-like as they seek safety, perhaps with a polite, apologetic shrug. We should not ask institutions to do things they are incapable of delivering.

Sorry – because of the way I see comments when moderating I never know what you are replying to

What issue is it you are addressing?

Sorry, Richard I can see it must be confusing; I am confused reading multiple comments to different comments quite often. I was responding to Clive Parry’s well made point; but I have real doubts about the capacity of the chosen vehicle, actually to deliver it. The £85,000 protetction for UK bank creditirs provided by the Government, in my opinion tells you all you need to know about commercial banking. Nobody else would ever be awarded such grace-and-favour protection from their own, historically domenstrable folly.

Agreed…

Ooops, atrocious editing of my hasty added comment; but I hope you catch the drift.

Whilst I am sympathetic to your aims, is there not a significant risk that by reducing the BoE rate to 1% there will be a run on the pound? Isn’t this the equivalent of Truss’s mistake? However much we dislike the financial markets they are not under your control and will react .

Why not tax the banks on their windfall profits and return that money to the poor in a hike in Universal credit or some other means?

Tax by all means

But you ignore the reality that high interest rates will deliver devastation for millions

What would you prefer? Some inflation or millions with no home?

You must have had fun doing that fantasy budget, Richard – and it was fun to read, but I was surprised by some absences as well as concerned about how some presences were presented.

Absences first. Where was the new taxation policy on excess profits, for example, but by no means uniquely, among the energy companies or the banks? In present circumstances, should you not also have been bringing forward (that is the jargon, is it not?) a scheme to provide emergency suport to SMEs in relation to their energy ccosts. (If, as you’ve often stressed, they go under – and you do address their danger from current IR policy – huge negative consequences flow to spending and to ordinary society.) And last, but by no means least, where had the Brexit gremlin got to in your opening list of causes of our current economic discontents? I rather thought it should have featured near the top, perhaps with a nice line about how your ‘rt. hon. friend’ the Trade Sec. would shortly be addressing the House in a supplemenary statement ‘designed to mitigate the disatrous lack of opportunities with which that had burdened the country.’ (I can but dream – but, come on, you had the floor!)

Presences presented (or not?). I wondered particularly about the order of your ‘speech’. How you are ‘heard’ would surely matter in these nervous times almost as much as what you said. So, might it have been worthwhile spelling out, from the start, the positive boost to the viability of businesses, especially real terms producers, of the increases in wages, benefits and domestic spending power which ‘this statement will lay out’. (‘Madame Deputy Speaker, one of my honourable predecessors, much loved by the benches opposite, proposed to “fortify the Revenue”, by himself drinking brandy at the Dispatch Box! I shall do so instead with the aid of the vast majority of the consumers of this country.’ etc.)

{Oh dear, this fantasy stuff becomes catching. ‘Let me recommend to the Members opposite a “cakeism” – where everyone may not only eat cake but all shall have the money to pay for it.’}

And a last serious point, but prehaps really the first, shouldn’t it have had a title – and, of course, a punch-line right at the end? I’ll resist the temptation to coin one myself, but would urge you, as you craft it, to find a line whose shortened version (or even acronym) needs to be tamper-proof against the evil machinations of tabloid headline writers!

(A tag such as ‘a Budget for stability, wealth and growth’ would be all over the red tops as SWAG before any poor ‘chancellor’ regained their seat – and one which prouldy proclaimed its catch-phrase as ‘Green and sustainable’ would be GAS in equally short measure.)

Nigel

You are right: none of these proposals are complete. This could be read in 8 minutes: a budget takes much longer, so I had to be selective. Sorry.

Over the various versions now out I think you will find the issues you mention covered. There will be more chances to do so now.

Richard

Sadly Sunaks budget will not even register the bottom 50% or even 10% of the population. Because he doesn’t see them at all. Inflation and lack of price controls on non discretionary spending for this group will likely economically crush them.

What might the economic and political price to pay?

Slightly off topic, but this article “The fantasy economics of the Nobel Prize ” by Steve Keene is interesting:

https://iai.tv/articles/the-fantasy-economics-of-the-nobel-prize-auid-2279

It is very good

The Conservative spin is now that in PMQs today Sunak was on “the front foot”; and for the first time in some weeks ormonths, the back bench MPs were loud in support. Think about that for a moment. Yesterday it was the theatre of sombre humility. This, we were being persuaded, was the new, serious Conservative Party.

It didn’t last long. Less than a single day (but then, we have a Cabinet, literally of Conservative rejects, recycled again; and in some cases, again or again, or in one case in less than a week for breaching the Ministerial Code; that in the past, finished careers).. At PMQs a front foot PM responding to questions by attacking Labour (Johnson used to do this, reducing ‘bringing the Government to account’ by reducing it from comedy, through farce to a clown-fest); the back-benches in their old form, braying like donkeys: as if nothing had happened. Seriousness didn’t last long. The cut-through question (did the security services race the Braverman.

reappointment with the PM, he just evaded, and left us all to guess).

Serious? No. Integrity? No. Evasive? Yes. Cheating the public of the General Election to which integrity entitles them, like a beacon light in the midst of shoddy political double-dealing? Yes.

Agreed

Richard – in responding to “derek” saying your proposals would tank the pound, you say “So you think that is enough to influence value, and real trade is not?”. My understanding is that “trade” is only a tiny proportion ( I have seen figures of 5 – 10 percent quoted) of global F/E movements. Isn’t the vast majority of it merely seeking the highest returns?

But the vast majority of the excess is hedged and so very largely net neutral

I know how I’d like to tackle Sunak – preferably low, and at high speed. Enough for him to ask to be substituted, take an early shower and go home and play some other game he is suited to.

It is a government of duffers of which he is No.1.

This got stuck in my head today. Seems a suitable theme song for Rishi Sunak.

https://youtu.be/Wt6M6ggQbZQ

I have forwarded this article to my MP Anneliese Dodds commending it and asking her to forward it to Rachel Reeves. All your readers and followers should send it to every MP.

Thanks

All I can say is ‘Oh for a government high street bank’.

Now wouldn’t that put the cat amongst the pigeons?

Or should it be ‘vultures’?

I didn’t know that websites on accountancy had such deep social issue articles – really good. It doesn’t all have to be right but would get the real economy moving for the majority. It is detailed enough to be tweaked as the situation changes.

“You think millions unable to afford homes and children without food is better?” How I agree.