Peter May, who pretty much runs the Progressive Pulse website these days, even though I am its director, wrote a really important blog on Friday. As he noted he'd had another letter from the Treasury to an MP on the subject of whether or not it creates money using quantitative easing. This was as follows:

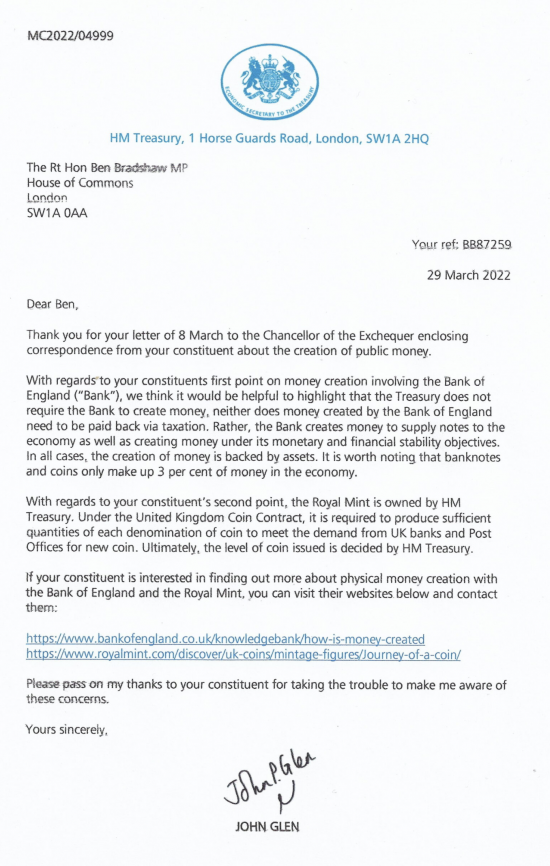

Another interesting letter from HM Treasury:

As Peter noted:

They say:

….the Treasury does not require the Bank to create money, neither does money created by the Bank of England need to be paid back via taxation. Rather, the Bank creates money to supply notes to the economy as well as creating money under its monetary and financial stability objectives. In all cases, the creation of money is backed by assets.

So we have some money created by the Bank of England which does not need to be paid back via taxation. Just simply for monetary and financial stability…

Presumably we could increase the ‘national debt' purely on the basis of “money created by the Bank of England [which does not] need to be paid back via taxation.”

That is surely progress.

So that indicates, I suggest, that at least some money is not part of the supposed ‘national debt'.

That again is progress (if philosophically dubious!)

But backed by which assets?

What are these?

Unsurprisingly, I have asked for further clarification.

I wanted, in particular, to consider the claim that all the money that the government creates is asset-backed, as that is a very strange claim to make, especially as the Bank of England's own webpage on money creation, linked in the letter, makes it clear that commercial bank money is not asset-backed. It is instead an arrangement backed by mutual promises to pay, which it explains. Why then is government money so different, as John Glen MP claims?

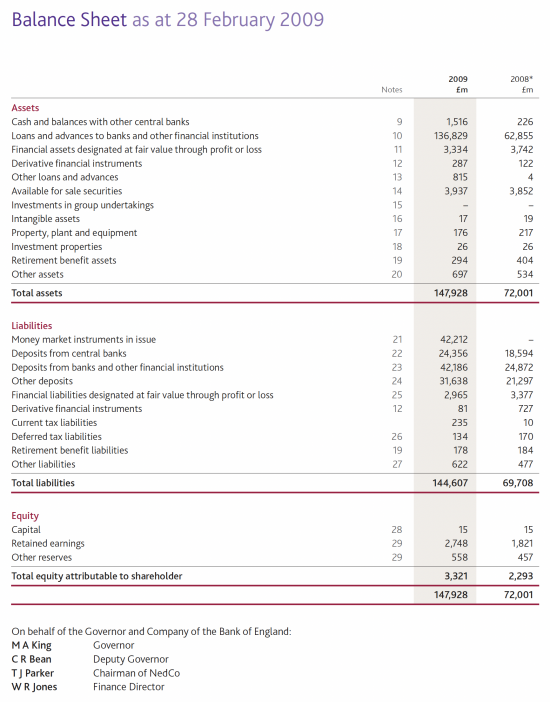

Some evidence helps. First, the Bank of England's balance sheet in 2008 and 2009:

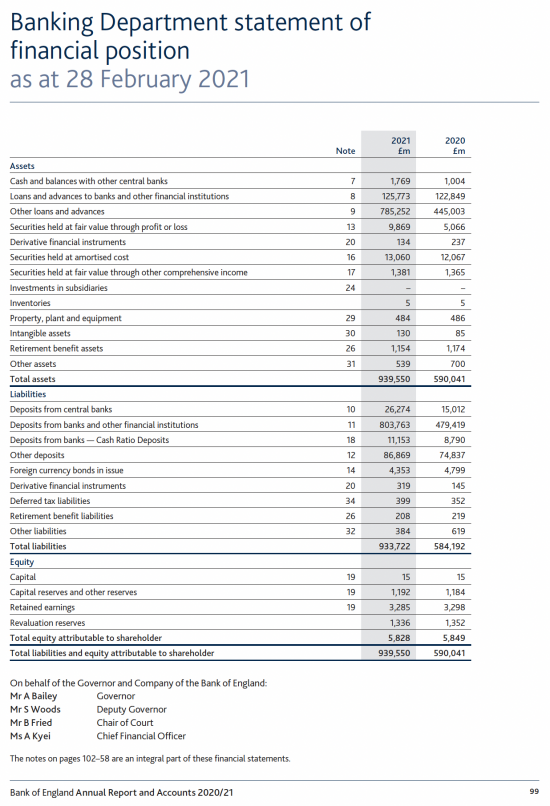

Now contrast those 2008, pre QE and financial crisis, figures with 2021, which is the latest data available:

To add important colour, I also add these notes:

So, let's be clear about the differences between 2008 and 2021.

Net assets have grown from £2.3 billion to £940 billion.

Repo funding has stayed almost exactly the same (£136 billion in 2009, £63 billion in 2008 and £126 billion now).

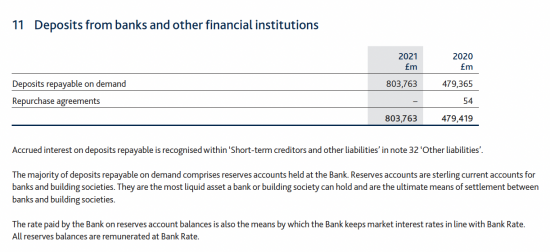

But other loans and advances have grown from £4 million (yes, million) to £785 billion and sums on deposit (the central bank reserve accounts of the UK's clearing banks and related financial institutions) have grown from £25 billion to £804 billion.

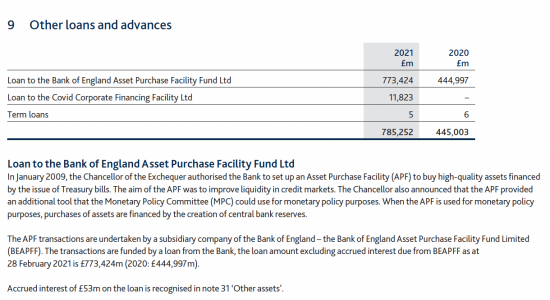

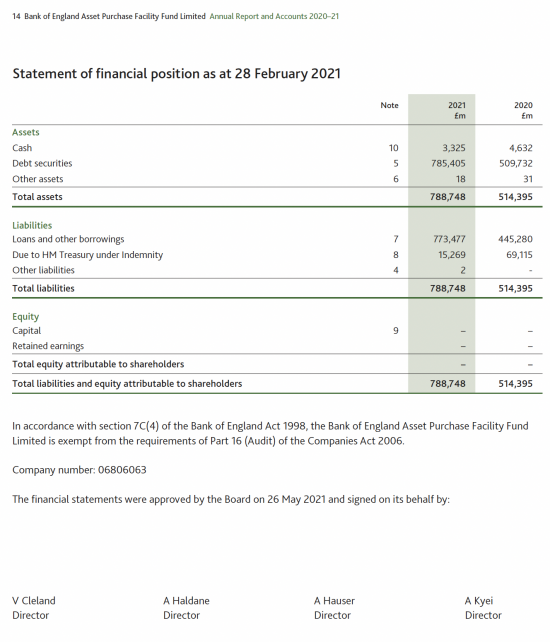

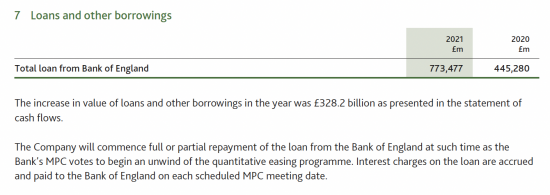

Money is a liability on the Bank of England balance sheet. It is not an asset. In other words, the new money supply since 2008 was £779 billion (£804bn less £25 billion). So what is the asset that backs this? It is the loans and advances of £785 billion, which note 11 shows was almost entirely lent to the Bank of England subsidiary company, Bank of England Asset Purchase Finance Facility, whose accounts are illegally (in my opinion) not consolidated in the Bank of England accounts, an action that can only be justified if it is not really a subsidiary company of the Bank of England but is instead under the control of the Treasury (which it is easy to argue that it is).

What do the accounts of this company show that it did with the money? Like the accounts of the Bank of England, these are available here, the most recent being for February 2021 at present:

Again, some notes help:

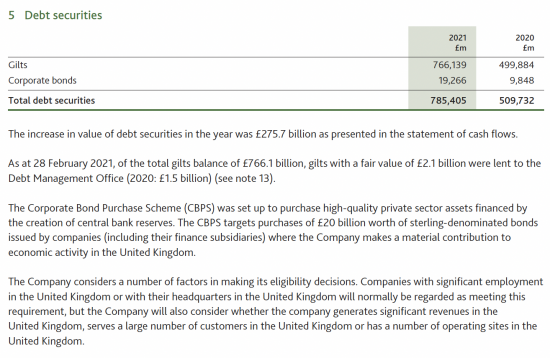

So, the APF (as it is called) used the sums lent to it to buy government gilts. These are its assets.

In that case if the company's accounts had been consolidated with those of the Bank of England what we would see is that new money created by government spending (the sums on deposit from the commercial banks held with the central bank, and effectively representing quantitative easing balances) were backed by government bonds. In other words, the only backing for government-created money was a government promise to pay, in the form of bonds. There was no other asset involved at all; there was just a promise to pay, which is what all money is.

How then can John Glen claim that the money in question is asset backed? The simple fact is he cannot. The money is just backed by a government promise, and that is all. In other words, the money is made out of thin air.

I hope Ben Bradshaw MP might go back and say:

Dear Mr Glen

Thank you for your letter of 29 March 2022.

I have noted your claim that all government created money is asset-backed. I have also noted the analysis of this claim on the Tax Research UK blog, which shows that the only asset that has backed the issue of new money by the Bank of England since 2008 has been the acquisition by that Bank of government bonds through its subsidiary, the Bank of England Asset Purchase Finance Facility Limited using the quantitative easing process. There is no evidence of any other asset backing on the Bank of England balance sheet.

Might you, in that case, explain what you meant by asset backing for this government created money?

Might you at the same time explain why the Bank of England does not consolidate the results of its subsidiary company into its own accounts? Is that because it is agreed that this subsidiary company is actually under the practice control of the Treasury, which guarantees all of its liabilities and has an absolute claim to its income?

In that case would you also agree that the only asset backing this newly created money is, in fact, a government guarantee?

I look forward to hearing from you,

Etc.

I leave it to Peter May to decide what to do.

Thanks for reading this post. You can share this post on social media of your choice by clicking these icons:

Ben Bradshaw is a perfectly diligent MP but unfortunately economics and finance, as he has sometimes admitted, is not his forte…

As I find you get ignored if you write to the Treasury direct, I need him to keep firing the ammunition while keeping some grasp of its makeup.

I therefore concentrated on very, short simple and open questions as to what these assets were?

And whether, as they were backed by assets, perhaps they were not part of the national debt?

I think your more technical letter is most likely to be the reply to that…

As I really cannot see how John Glen gets out of his asset problem – particularly as he says:

“In all cases, the creation of money is backed by assets. It is worth noting that banknotes and coins make up 3% of money in the economy.”

-which seems to imply that what the Royal Mint produces is asset backed too!

Dear all finance ministers of monetarily-sovereign nations,

The game is up. We all know the Treasury is in negative equity. No amount of smoke and mirrors or bare-faced denials can disprove this notion. And that’s fine. We know this to be fact and – crucially – we desire it to be this way. Your deficit is our surplus.

Now that awkward conversation is out of the way, may I suggest you pull out the proverbial finger and get started on delivering vibrant, caring, green economies with decent jobs and pay for us all to prosper.

Did you need reminding that is your raison d’être?

A pithy answer to the question of what gives sterling (or USD, SGD, AUD, JPY, DKK, NOK, SEK etc) value is the fact that individuals and businesses have to pay taxes in those currencies, depending on which country you live. A longer answer is I have to pay taxes in GBP, so I invoice clients in GBP. When I visited Denmark, I had to spend DKK because Danes have to pay taxes in DKK and so on for the other examples

True. If the promise to pay isn’t an asset, I guess we need another term. I recall you said that taxes and the promise to pay ratify the value of fiat currencies but it is true that they are not backed by tangible assets like gold

The worst thing is that the ‘promise to pay’ or shall we say in our case ‘the factual ability to pay’ by our Government seems only something the rich and Tory chums are allowed to benefit from – not the man and woman in the street.

Many thanks Richard, Peter, et al for a truly brilliant thread! I anticipate eagerly the response from John Glen this time! Having made his claim about ‘asset backing’ in his response and now seeing the actual bank accounts, how will he get out of that one? Having to admit there are no assets and only the promise to pay, the whole argument the Government makes about money and debt, etc., is proven to be invalid. Wow, am I looking forward to seeing that and then for every media outlet to have to share this.

Brilliant thread which must place John Glen and others that spout the falsehood of ‘asset backing’ firmly on the ropes! I anticipate eagerly the response from Mr Glen which then must be shared by all the media. It’s high time the truth is out in the open and every media outlet’s economics editor must be corrected.

Perhaps John Glenn should ask Jacob Rees-Mogg for the official explanation of ‘asset backing’. He seems happy to tie himself in knots to explain every other Tory con trick.

Whilst fiat money is not backed by “assets” it IS backed by the productive capacity of the economy and the “promise to pay” is based on the state’s ability to ensure that needs are met. Maslow’s “hierarchy of needs” is relevant to understanding what those “needs” are.

If the currency in use in an economy cannot be used to acquire what people need then it loses its value – the value of money is inseparable from the creation of “use value” . It’s a yin and yang relationship. Shortages of what people need means prices go up (inflation; loss of value of the currency) and they may then swap their currency for another in order to acquire what they need from elsewhere (which affects the exchange rate of the currency).

The holder of a quantity of the currency holds a claim to a share of the collective real wealth produced in the economy commensurate to the quantitative value of the money which the “bearer” holds. The “promise to pay” is essentially a promise that claims to a share of the collective wealth will be redeemed.

Our Website uses cookies to improve your experience. Please visit our Private: Data Protection & Cookie Policy page for more information about cookies and how we use them.

Many thanks, Richard

Ben Bradshaw is a perfectly diligent MP but unfortunately economics and finance, as he has sometimes admitted, is not his forte…

As I find you get ignored if you write to the Treasury direct, I need him to keep firing the ammunition while keeping some grasp of its makeup.

I therefore concentrated on very, short simple and open questions as to what these assets were?

And whether, as they were backed by assets, perhaps they were not part of the national debt?

I think your more technical letter is most likely to be the reply to that…

As I really cannot see how John Glen gets out of his asset problem – particularly as he says:

“In all cases, the creation of money is backed by assets. It is worth noting that banknotes and coins make up 3% of money in the economy.”

-which seems to imply that what the Royal Mint produces is asset backed too!

Let me think of alternatives

Economics and finance is not the forte of ANY of the MPs in my opinion.

While our mob of hopeless ineffectuals are floundering around trying to pretend our fiat currency’s backed with assets, the Russians are actually linking the ruble to actual gold. Interesting times ahead then, one imagines https://www.bullionstar.com/blogs/ronan-manly/russian-ruble-relaunched-linked-to-gold-and-commodities-rt-com-q-and-a/

The Russians are limiting their fiscal space in so doing. Not a clever move on their part.

I don’t think they’re making their currency commodity backed. It’s something more devious than that.

Dear all finance ministers of monetarily-sovereign nations,

The game is up. We all know the Treasury is in negative equity. No amount of smoke and mirrors or bare-faced denials can disprove this notion. And that’s fine. We know this to be fact and – crucially – we desire it to be this way. Your deficit is our surplus.

Now that awkward conversation is out of the way, may I suggest you pull out the proverbial finger and get started on delivering vibrant, caring, green economies with decent jobs and pay for us all to prosper.

Did you need reminding that is your raison d’être?

Sincerely,

Everyone whose head is not in the sand

🙂

A pithy answer to the question of what gives sterling (or USD, SGD, AUD, JPY, DKK, NOK, SEK etc) value is the fact that individuals and businesses have to pay taxes in those currencies, depending on which country you live. A longer answer is I have to pay taxes in GBP, so I invoice clients in GBP. When I visited Denmark, I had to spend DKK because Danes have to pay taxes in DKK and so on for the other examples

But there is no asset

True. If the promise to pay isn’t an asset, I guess we need another term. I recall you said that taxes and the promise to pay ratify the value of fiat currencies but it is true that they are not backed by tangible assets like gold

We agree

The worst thing is that the ‘promise to pay’ or shall we say in our case ‘the factual ability to pay’ by our Government seems only something the rich and Tory chums are allowed to benefit from – not the man and woman in the street.

Many thanks Richard, Peter, et al for a truly brilliant thread! I anticipate eagerly the response from John Glen this time! Having made his claim about ‘asset backing’ in his response and now seeing the actual bank accounts, how will he get out of that one? Having to admit there are no assets and only the promise to pay, the whole argument the Government makes about money and debt, etc., is proven to be invalid. Wow, am I looking forward to seeing that and then for every media outlet to have to share this.

Brilliant thread which must place John Glen and others that spout the falsehood of ‘asset backing’ firmly on the ropes! I anticipate eagerly the response from Mr Glen which then must be shared by all the media. It’s high time the truth is out in the open and every media outlet’s economics editor must be corrected.

Perhaps John Glenn should ask Jacob Rees-Mogg for the official explanation of ‘asset backing’. He seems happy to tie himself in knots to explain every other Tory con trick.

This is how I see it:

Whilst fiat money is not backed by “assets” it IS backed by the productive capacity of the economy and the “promise to pay” is based on the state’s ability to ensure that needs are met. Maslow’s “hierarchy of needs” is relevant to understanding what those “needs” are.

If the currency in use in an economy cannot be used to acquire what people need then it loses its value – the value of money is inseparable from the creation of “use value” . It’s a yin and yang relationship. Shortages of what people need means prices go up (inflation; loss of value of the currency) and they may then swap their currency for another in order to acquire what they need from elsewhere (which affects the exchange rate of the currency).

The holder of a quantity of the currency holds a claim to a share of the collective real wealth produced in the economy commensurate to the quantitative value of the money which the “bearer” holds. The “promise to pay” is essentially a promise that claims to a share of the collective wealth will be redeemed.