This is a guest post from, Dr Tim Rideout of the Scottish Currency Group, with whose work many here will be familiar:

It is regularly claimed that the Royal Bank of Scotland, Bank of Scotland and other banks operating in Scotland will leave Scotland at the first hint of Independence.

Let us consider the Royal Bank of Scotland.

Firstly, we need to understand what is meant by The Royal Bank of Scotland (RBS). It is usually implied this means what is now called Natwest Group Plc (and which was RBS Group until 2020). The Group, though is NOT a bank, but simply a holding company that owns a large number of individual banks. The biggest bank in the group by far is Natwest Bank Plc, which is and always has been a London based bank registered in England. Natwest Bank Plc was purchased in a hostile takeover by the Royal Bank of Scotland in 2000. After the takeover RBS Group Plc was established as a holding company and thus Natwest Bank and RBS became banks owned by RBS Group. There are other banks such as Coutts & Co, Ulster Bank and Isle of Man Bank. The only Scottish bank within Natwest Group is the original Royal Bank of Scotland, which is still based at the registered office on St Andrew's Square in Edinburgh as it has been for decades (though this has moved to the very grand bank branch rather than the office building that was sold off).

Secondly, we need to realise that the many component banks in the group are all legally separate and distinct companies. They have their own banking licences and file their own annual accounts. Natwest Bank has always been English and since the 1920s has been based in London. This means the Project Fear line that Scotland could never support or rescue the Natwest Group is a deliberate lie. Each bank in the group is the responsibility of the jurisdiction where it is registered and operates. So Natwest Bank has always been and would be in future the responsibility of the UK government and the Bank of England. The US Citizens Bank, which was part of the Royal Bank of Scotland until it was sold, was the responsibility of the US Federal Reserve, thus it was the Fed that provided it with emergency funding in 2008. As stated earlier there is only one bank in the Natwest Group that is registered and operates in Scotland, and that is RBS Plc (Adam & Co is just a trading name and not a stand-alone bank). So post-Independence it is only RBS Plc which would obtain a banking licence from the Scottish Reserve Bank, be regulated by the SRB and have the SRB as Lender of Last Resort. Whether the brass plate of Natwest Group Plc is in Gogarburn or London is irrelevant as it is not a bank and is not eligible for any such funding.

Thirdly, the Project Fear line is that the Royal Bank is simply too big for Scotland to be able to regulate and support if in financial difficulties.

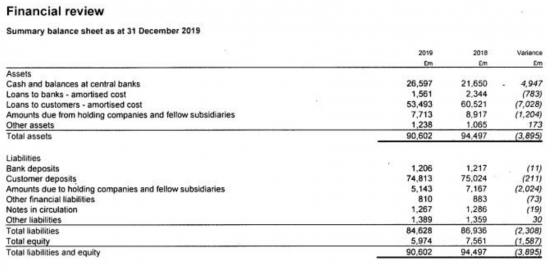

The table is from the latest RBS Plc accounts filed at Companies House. It shows the Balance Sheet as at the end of 2019. What this shows is that RBS is a medium sized bank with total assets of £90.6 billion. That is a small part (11%) of the overall Natwest Group balance sheet of £800 billion. In comparison Clydesdale Bank Plc had assets of £38 billion in 2015. As a result of branch closures and re-structuring within the Natwest Group, then it is now the case that RBS Plc has very few branches or business outside Scotland. Would RBS be too big for the Scottish Reserve Bank to rescue? The answer is a clear NO. Scottish GDP is around £170 billion (rather erratic at the moment due to Covid), which would make the RBS balance sheet equal to 53% of GDP. The total HMG funding by buying new shares provided to RBS Group in 2008 was about £43 billion at a time when the balance sheet was over £1.5 trillion. Equivalent funding to the current RBS Plc would be about £3 billion. In practice there is no limit to the S£ that the Scottish Reserve Bank could provide in emergency funding if it wished to do so. In the worst possible total collapse of RBS Plc the SRB might be called on to repay the depositors' deposits of £75 billion. However much of that would be recovered from the assets and in particular the repayment of loans to customers.

Fourthly, it is worth noting the Bank has cash assets of £26.5 billion. Most of this is on deposit at the Bank of England in what is called the Reserve Account. The central bank acts as banker to the commercial banks so those banks hold their own money (as opposed to customer funds) in their Reserve Account at the central bank. After Independence then this £26.5 billion will be exchanged into the new Scottish Pound and will be held on deposit at the Scottish Reserve Bank instead of the Bank of England.

Finally, could the Royal Bank leave Scotland? The answer is a definitive NO. That is because almost all of its business and branches are in Scotland. After Independence foreign banks will not be allowed to operate in Scotland unless they establish a Scottish subsidiary, register as a bank with the Scottish Reserve Bank and hold sufficient reserves at the SRB to meet our regulatory requirements. If RBS left Scotland it would effectively close down as it would no longer be able to serve its clients in Scotland or carry out most of the current business.

We have already noted that where Natwest Group has the brass plate is essentially irrelevant as it is just a holding company. Corporation Tax is paid at the operating company level so for the year ended 2019 RBS Plc paid £338m in tax. After Independence that S£338 m would be paid to the Scottish Government. Would Natwest Group seek to transfer staff and group facilities from Gogarburn to London? That would not be a sensible business strategy due to disruption and to the significantly higher wages and other costs that would be incurred in London. In addition the Gogarburn building belongs to the Pension Fund so the rent remains within Natwest Group.

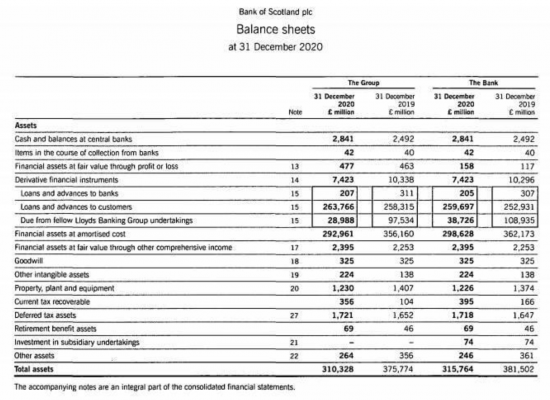

Another large bank in Scotland is the Bank of Scotland Plc. This is owned by the Lloyds Banking Group , but as with RBS the Bank of Scotland remains a legally separate company with its own banking licence. Surprisingly, you can see from the 2020 accounts below that BoS is actually over three times larger than RBS at £310 billion of assets. This is because it includes what was the Halifax Building Society and its very large mortgage book. The majority of that relates to properties in England. On Independence the Bank of Scotland would need to separate out the non-Scottish business into a rUK bank, probably by reviving Halifax as a legal entity. That would probably leave the Scottish part of Bank of Scotland at about £50 billion or so. The Clydesdale Bank Plc has assets of the order of £80 billion, but that includes the Yorkshire Bank and what was Virgin Money. Virgin Money is now the main trading name, but Clydesdale Bank Plc is the actual legal entity. As with RBS then neither the Scottish part of the Bank of Scotland or the Clydesdale could leave Scotland as that business can't be moved without simply being lost entirely.

To conclude, it is not possible for any of the banks that operate in Scotland currently to ‘move' out of Scotland. If they wish to keep their Scottish business and continue to generate profits in Scotland then they can only do so via a company registered in Scotland with, in due course, a banking licence from the Scottish Reserve Bank. The only other option would be to leave Scotland by either selling their Scottish operation to another operator or by closing it down. As the operations are profitable then closing them down makes no sense at all, so if they genuinely don't want anything to do with an independent Scotland that would leave a sale of the Scottish business. That just changes owners while leaving the Scottish operating company essentially unchanged.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

There are two points that are worth consideration in this context.

1) Before the crash the RBS balance sheet was over £2Trn; one UK bank. What does this tell us about the relative position of the UK economy and its financial sector? The major UK banks are larger than the UK economy. Mark Carney, then Governor of the BofE, pointed out on the 10th anniversary of the Financial Crash (2017), that on current trends, the UK financial sector could double in size to be 20 times as big as UK GDP within the next 25 years.

2) The SCG analysis reminds us of the strange, muddled contingent relationship in Britain between the recording of registered offices, economic reality and the reporting of economic data. The decision about a brass plate may feed into official economic data – including GERS. Huge changes in reporting could occur simply through the contingent capture of data referring to a single corporation, and nobody would know (save through an ex-post recording of a ‘post-balance sheet event’ that is never specified but appears in adjusted data in future years. These unspecified amendments are constantly being made).

The British state has not been set up to record accurately the economic activity of Scotland; that is just a fact that is itself falsely described by acknowledging that an independent Scotland would not produce data in the same form: Scotland’s economic data is not being properly recorded or allocated – that is reality. This is frequently denied by Unionists but it remains an inconvenient fact that merely records the endemic official indifference to Scotland which has very serious practical consequences in the depth of our continuing ignorance about Scotland, the Scottish economy and Scottish society. The fact that the Scottish Government operates this system simply reminds us how deeply committed it is to a primitive form of ‘status quo’ managerialism; which began as a perceived political necessity and has become a self-perpetuating reality, but is now fast dissolving into a text-book case of Obsessive-Compulsive Disorder.

For those who challenge this, then they can fix this easily through living up to the virtue of transparency: release all the data, all the detailed assumptions, and every single calculation used to produce GERS.

To be picky about it in 2008 RBS Group was still a holding company for lots of individual banks so there was never one bank that had a £2 trillion balance sheet. As things stand now I am not sure if it was deliberate or just a co-incidence but Natwest Group has removed almost all the bits of RBS Plc that were outside Scotland, so the former Williams & Glynns RBS branches in England are now almost all closed or converted to Natwest. So in this case we can see almost exactly what the stats are, so for example the P&L shows around £400m of Corporation Tax paid by RBS which would got to Scotland after Indy.

All of the £2Trn was for companies registered in the UK, and therefore in terms of ‘Project Fear’ was the responsibility of the UK, if support and rescue was required. At the same time the RBS-Nat West total excludes the balance sheets of all the other UK banks, which compounds the scale of the UK problem by the scale of the City of London UK banking sector, which is huge; therefore the scale of requirement to ‘support and rescue’ all these banks in adversity falls wholly on the UK; a vast, contingent and unknown scale of liability, almost incalculable at any given point (‘too big to fail’); far beyond the relative risk position of an independent Scotland. The same principle of a financial sector out of porportion to the scale of the domestic economy applies, ‘mutatis mutandis’ to the UK, but with far greater force and carrying far, far greater risks for the UK.

We saw that horror show rehearsed in 2007-8. It remains as a permanent contingent liability for the whole UK, and it is worth remembering that the UK possesses a track record of regulatory supervision over that risk which is wretched, poor forecasting of emerging financial crises, and long term risks that remain high. Scotland is better out of the casino. All this was brought about by ‘Big Bang’ in 1986, which handed the City of London the great Scottish banking system to envelope culturally, turn its institutions into City predators or prey, and then destroy. Three hundred years of the great Scottish contribution to banking has effectively been comprehensively and permanently destroyed. The only real creative and secure future for Scottish banking would be independence.

The argument is made that the HQ in Edinburgh of RBS will move, and it is that which represents the real loss to Scotland; but the truth is RBS is already a London Bank in all real respects of management and control (and has been for at least a decade), beyond the mere illusion conjured by a brass plate and some real estate.

Richard, I doubt very much Scotland would not permit foreign banks to operate in Scotland without being regulated by the Scottish authorities. That would exclude Scottish consumers and businesses from doing business with UK and European banks.

Even if that’s a result you wanted (which I doubt) it wouldn’t be legally possible if Scotland joined the EU. RBS could move its headquarters and place of regulation to e.g. The Netherlands, and “passport” into Scotland.

You may wish to speak to a regulatory expert and rework this article

No one is saying that a foreign owned bank would be barred from operating in Scotland

I don’t think you have read the article

You said:

“If they wish to keep their Scottish business and continue to generate profits in Scotland then they can only do so via a company registered in Scotland with, in due course, a banking licence from the Scottish Reserve Bank.”

Which would be contrary to EU law, because “passporting” means the Scottish must accept an EU registered bank that’s regulated in the EU.

Again: I don’t mean to be insulting, but you clearly do not understand how cross-border regulation of banks works. Why not speak to someone who does?

You are aware of the fact that this almost invariably has does not happen, aren’t you?

People remember the Icelandic banks with a reason

And you are arguing hypocritical s not actualities

I suggest you fund another play pit to play in: this one is for those who deal with the real world

Foreign banks will be welcome to operate in Scotland but that will mean establishing a Scottish subsidiary if they want to be providing services in the S£. If Scotland does re-join the EU then that won’t happen probably until at least four years after Independence so there won’t be any passporting before then. There is nothing to stop people in Scotland opening bank accounts where they wish so they can have a Euro account with an EU bank. Anyone who wants to keep a sterling account will be able to do so but they will be moved to the rUK part of their bank. So for example there will be Santander (Scotland) Plc working in S£ and Santander (UK) Plc working in Sterling.

And to think RBS or the new bank as it was called might have failed in 1745 had it not been for their brave cashier, John Campbell.

https://www.natwestgroup.com/heritage/history-100/objects-by-theme/times-of-turmoil/cashiers-diary-1745.html

This is the kind of stuff you get when someone without experience of financial markets starts writing about financial markets. It’s basically all wrong.

Leaving aside that RBS has stated publicly they would relocate to London, they also have well developed plans to do so in the event of independence. So too would Aberdeen asset management, Bailie GIfford, Kames and Standard life.

The only thing left of RBS in Scotland would be the retail bank, which is not hugely profitable.

An independent Scotland would be far too small to support even the standalone RBS balance sheet of £90bn. Which is over 50% of GDP. Given the liabilities are in Sterling, a Scottish reserve bank would be totally unable to rescue it. It could print as much S£ as it wants, but when you have to cover Sterling liabilities all that would be achieved is a massive devaluation of S£ as it would been to be sold to but Sterling – and that is before you consider the S£ would likely devalue heavily without such additional pressure.

Rideout is also totally wrong when he says that somehow the SRB would inherit £26.5bn of reserves which are currently placed at the BoE. The transaction is between the BoE and RBS, and no other entity has any claim on those assets.

Basically post independence, Scotland would lose almost all of it’s financial sector. The country would not be able to support the balance sheets of the Banks as it currently stands. This would dramatically increase the funding costs of these banks and would force a move to London. The case would be similar for the asset managers and insurers. In addition, market access from Scotland would be far more difficult, given it would not be in the EU or be a member of any of the financial markets treaties the UK is currently party to. Over time it would regain some access, but in the meantime financial institutions would be forced to relocate to maintain their businesses uninterrupted.

All that would be left in Scotland would be a few smaller retail banking operations, which are barely profitable. There is nothing to keep the rest of banking operations in Scotland when market access will be far more difficult, funding costs will be far higher and legislative and regulatory hurdles will be huge. The only thing keeping the Scottish finance industry strong is it’s being part of the UK.

By all means, write articles full of fantasy like this one, but the reality is that independence will cost Scotland most of it’s financial industry, and the tax revenues, investment and balance sheet that goes with it. That is before you consider all the support industries and jobs which go hand in hand. Of the approximate 7% of GDP directly attributed to financial services in Scotland, the current estimates are that 4-5% of it will be forced to relocate.

If you think that is a good idea – please go for it. London is going to be the beneficiary. But at least be honest about what you are saying, rather than putting out garbage like this.

The paradoxes in your claims prove you have not thought them through

First, the very small retail bank if it was all that was left would not require £90bn of support you claim is required

And of QE created course the reserves can all be removed – but then Scotland has no liability for any debt then

My suggestion is that you go and start thinking about this before writing nonsense

And also wonder why all banks would want to turn their bank in a country like Scotland. That has never happened anywhere else

Tell me why it will happen in Scotland?

Oh, and I very much doubt you are in finance….and I feel sorry for your employer of you are if this is the ability you take to work

Standard Life and Aberdeen Asset Management merged some years ago

I notice you haven’t bothered to post my response. I’m guessing that only comments that agree with you, or at a bare minimum don’t show up your and Rideout’s total lack of knowledge get through?

If your only claim that made sense was that I know nothing about finance you clearly have nothing useful or accurate to say because that s very obviously wrong

Trolls are not welcome here

It aint all over till the Fat Lady sings.

The first thing is that we have no idea exactly what the Scottish Finance Sector will do in the event of Independence unless it happens.

Secondly there will still be a market for Financial Services in an independent Scotland, clearly there will be players that will want to profit from that market, even if it isnt any of the existing players.

Precisely

An interesting synopsis by Tim on the latest “Disaster” to befall an independent Scotland – As with most of these politically motivated “too wee, too poor” arguments, the telltale is a “Scotland” tag to the company name to scare the Jocks, inevitably someone will appear to furnish the missing “too stupid” in comments.

Nobody knows who will be operating in a new Scottish economy let alone any other in 5 years time, nor frankly do many care what the name is except the politicos promoting Great British X.

None can predict the scale of Scotland’s new economy with any degree of accuracy, but the continued existence of GERS suggests it is and will be in remarkably rude health.

Any preferring an indignant flounce to profits will not be in position long.

An interesting perspective on Kate Forbes the Scottish Finance Secretary on growing up in India, her faith and how another independence referendum will be fought

BBC – R4 Political Thinking – Nick Robinson – The Kate Forbes One.

https://www.bbc.co.uk/sounds/play/p09j7xy1

(duration 35 minutes)

Listened

I recommend others do…..

What did you think?

For me, the worry is not what happens to the company registration but to the jobs.

I work in financial services and the majority of my customers are in rUK. I don’t expect an immediate withdrawal from Scotland but I can see a drip south, as when people leave their replacements are hired in new locations.