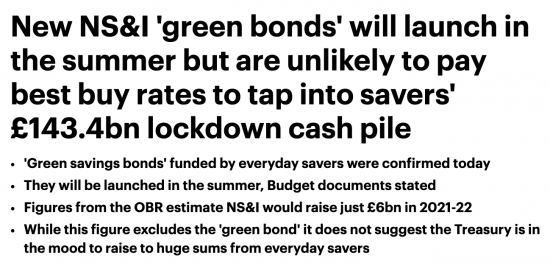

I take this from the Daily Mail:

In other words, by offering a miserly rate of interest the government is confirming it has no interest at all in really raising any useful money for green investment.

I estimate that if these bonds were to be the only bonds permitted within ISAs and if a rate of 1% was paid (which is easily affordable, given the cost of ISA subsidies already incurred, now put to social purpose) that something like £70 billion a year could be raised.

There is one easy conclusion to reach. They Chancellor is not trying. He takes an E effort.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

“I estimate that……”

Not really an estimate is it. What you’ve done is just take the amount invested into ISAs and then say that everyone should be FORCED to buy these green bonds. Seriously high quality analysis.

Apart from the authoritarianism of forcing people into certain investments, forcing people to invest in something – especially something with returns so abysmal – will make them look elsewhere or simply not invest at all.

No one would be forced to buy anything

Having access to tax relief is not a human right

It is for government to decide upon

I am suggesting how that power should be sued for social advantage

That is the right I have

You say that nobody would be forced to buy anything. But then say that these bonds would be the only permitted investment in ISAs. And if you want any form of tax relief on savings, again, only through these bonds.

So basically you are forcing people to invest in these terrible investments or pay more in tax. What a great choice. You even allude to the fact that you are forcing people to invest in these things by arguing for more government power and control. Very authoritarian. Do you even read what you write?

“I am suggesting how that power should be sued for social advantage”

So very glad that you don’t have any power, and are just someone mumbling away from their armchair.

“That is the right I have”

You have the right to say whatever you want within reason. The rest of us all have the right to take what you say, read it, laugh so hard it hurts at the sheer hubris of it all then assign it to the to the bin of loony ideas where it belongs.

Thankfully we live in a democracy, and any party that tries to force all savers to invest in something which is near guaranteed to lose them money in the long term, or be forced to pay a lot more tax on their investments, will never get a sniff of power.

So you think conditions should not be attached to tax reliefs?

Tell me why that is?

And why the state should not decide what those conditions are?

Kevin

If you had one iota of real intelligence, you would realise that the ‘green sector’ has a huge capacity for growth in technology and take up.

Growth of use and provision means in growth in investment returns doesn’t it?

Or does your personal bias come before the basic facts of investment?

BTW, the British Government has NEVER not paid back its returns on bonds. NEVER. So why shouldn’t they run such a scheme and guarantee it?

Now compare that to say the most recent events of 2008 where the Government had to bail out the ‘wonderful’ private sector by printing its money?

Do us all a favour Kevin and go back to school.

Agreed. Derisory effort.

But, I wonder what the Daily Mail stance will be? Many of my friends and neighbours belong to the “Daily Mail reading classes” and DO care about green issues and DO want 1% on their money. Heart and pocket are aligned and that might matter.

On a separate note, I got an e-mail inviting me into the “NS&I Community”. Not sure what it is about but I am guessing it is a way for them top understand savers better. So, I have joined and the first thing I see is a question about my attitudes to environment and recycling….. so I am posting questions like “so, what are they doing with our savings?” “Why can’t my saving be mobilised to help green the economy?” etc.

Doubt it will go anywhere but who knows.

Interesting ….

I can’t help feeling two things have been conflated here.

I know you believe that it is right for governments to use the way in which they apply taxes to pursue what they see as social good; it is the case that various UK governments over the past 25 years have used this ability by creating ISAs (and their predecessors) to incentivise personal saving. Whether or not you agree politically, it seems to me a reasonable decision for various reasons (though personally I think the annual allowance is no longer proportionate to any “rainy day fund” objective).

I also know you agree that it is desirable for society to move away from fossil fuels and other polluting activity, and thus there is an expectation of governments to provide a lead in that. One way is by earmarking money to invest in “green” projects, and I happen to agree with you that it is highly desirable to do so in ways that engages the public through retail savings vehicles as well as via corporate loans. The retail side will need government support to succeed, but the government’s input need only be a fraction of the public’s; it is likely to include guaranteeing the investment (proposed by it being part of National Savings), making the return competitive (we have not yet seen an actual proposal) and potentially giving it a tax advantage (and again, we haven’t yet seen whether that is on the table).

However you seem to suggest the second aim should supersede the first, whereas I see them as independent and able to co-exist. Obviously if you abolished ISAs you might force some of that money into the new “green bonds”, but wouldn’t it be more honest to encourage people to make a free choice — but be incentivised by a competitive rate and tax benefit as well as the ethical benefit?

Mind you I saw somewhere — possibly here — that the budget doesn’t increase the total limit on NS&I (i.e. what the government is prepared to guarantee) so there would be a problem if it was too competitive. However, ever the cynic, I anticipate a high profile announcement when these bonds are actually launched in the summer so Sunak may have held back details simply to gain maximum personal publicity then.

My answer is sim9le

We have a glut of saving

We do not need then unless they are applied for social gain

So why offer tax relief for absolutely anything else?

Government bonds have never – and will never – offer “best buy rates” as the Mail seems to think they should. Money lent to the government has greater chance of being repaid and therefore interest rates will also be lower.

Also, the link you provide shows no explanation of how £70bn would be raised. The linked blog post states that annual tax relief on ISAs amounts to £70bn, but that is an entirely separate matter from how much the population would invest in these green bonds at a given interest rate. You have no idea how much savers would be prepared to put in at 1%. Finally, if your proposal is to continue to allow an income tax exemption on the interest paid on these green bonds, you won’t actually reduce the annual £70bn foregone in tax relief (which, as I say, is separate from how much savers will invest). In fact by paying over the typical market rate for government bonds you will forego even more money.

Let’s stick to a simple observation

I am suggesting a 1% interest rate

I am suggesting it in an ISA

I am suggesting it is the only fund in ISAs

I am suggesting – because it is true – that tax incentivised saving is intensely popular

Now, what have I got wrong?

And why not £70bn?

There is £1.6 trillion in cash saving. Why not more than £70bn?

Truth if any were needed that Sunak is another in a long line of lightweight chancellors.

It is a good thing that the issue of what is getting done with our savings is raised. Most of us have various pensions, savings in funds, etc with little to no idea of where our money is being spent. I do try and take an interest but it’s pretty hard to find out. Even “ethical” funds don’t necessarily match what a saver might feel is ethical.

While this initiative may be a damp squib it has raised your question of should ISAs be tied to investments of social merit which is a very good question.

We’re in this weird dystopia where no one wants their money spent on chopping down rain forests but we invest blindly creating a fiduciary duty on the fund manager to maximise profits which could well come from chopping down rain forests.