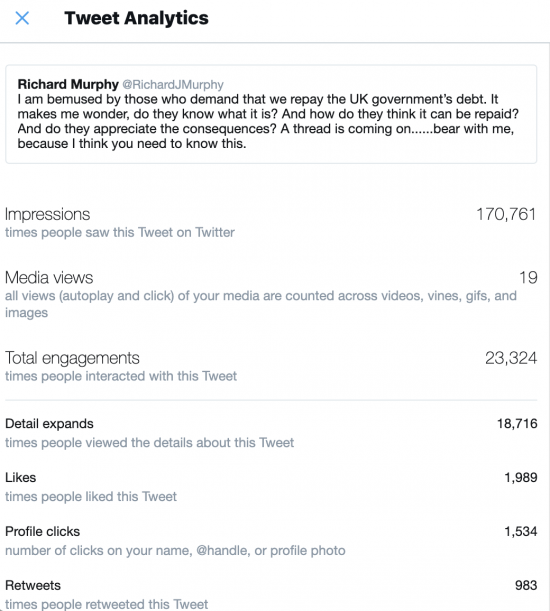

There has been some discussion on here as to why I have been writing long Twitter threads (up to 4,400 words long) and have then been reposting them on the blog whilst retaining the slightly odd constraint that each paragraph has no more than 280 characters in it.

The answer is quite simple, and that is that this has the greatest impact. Yesterday's thread has had this Twitter impact, so far:

Even some way down the thread engagement remained high - at several thousand per Tweet. That meant people worked their way though it.

Compare that to the blog where total reads of that post, so far, have been 531 out of total reads yesterday of a little over 4,000.

Now, 4,000 was low for any day this year: the daily average reads is around 8,700 this year, giving a total of nearly 3.1 million reads to date in 2020.

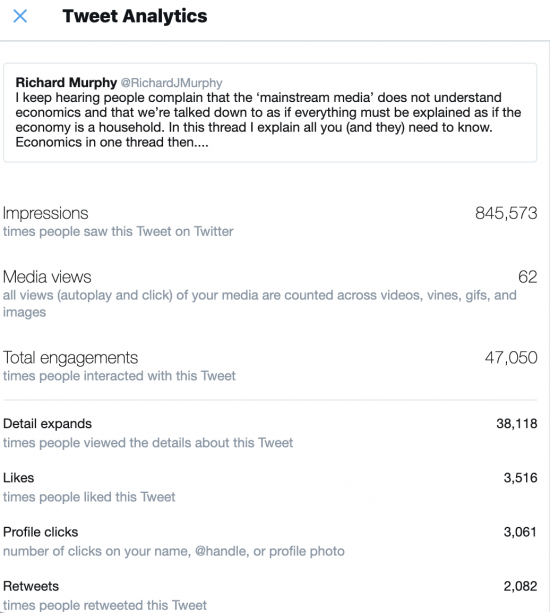

But then compare that to the impact of the thread on QE from a week or so ago:

Of course, 845,573 people did not read that tweet. Byt 47,050 probably did. And more than 3,500 liked it and more than 2,000 shared it. That's a reach the blog simply has not got.

I am not going to overburden Twitter followers with threads of this length all the time: that would be absurd. They also take some time to develop. Yesterday's took a week to write, on and off of course. But I don't just write for fun; I also write to have an impact. And Twitter is a place to get that, it seems. So, for the cynic suggesting I was wasting my time there, I think otherwise.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

It was a very long post and probably one that is worth me revisiting again but re-reading sections of it rather than the entire article.

These topics are detailed by their nature and not something that can be explained in a headline or phrase. So, I’m grateful for those who take the time to put something together to explain things. I want to learn and understand so that I am better informed.

So, thank you, Richard. Keep up the excellent work. And, Merry Christmas to you.

Craig

Thanks Craig

You have made a salient point about reaching out through social media and I congratulate you on your sagacity.

Richard, a happy Christmas to you and yours and let’s hope a more normal 2021. If you think that Twitter will broaden your coverage, go for it, it is no ones business but yours.

On a slightly different tack, just when I thought that the “mystery of the disappearing bank loan” was laid to rest, my subconscious mind intervened. I fully understand – from your video – that there is a “debit” loan account and a “credit” customer account, and, “when the customer comes to repay the loan the credit, of course, disappears and so will the debit disappear.” Clearly, for customer to repay the loan, the full amount of the loan plus interest must have been paid into the bank’s account. What I would now greatly appreciate, is: how and where are the customer repayments recorded by the bank? As is required. You explained in your video that both the debit and credit bank entries are now zero, and yet the bank has received the full amount of the loan and that must be recorded somewhere.

The loan. creation is Dr loan account, credit current account

When the customer spends it is Dr current account, credit someone else’s account

When they repay it is cr loan account, dr current account

If the current account is not to be in overdraft then to keep it in balance there must have been an entry to credit it and debit someone else – their employer, maybe

So, where is the money now? With whoever owes that debit

But there is also the debit left over in all this with the person who the money was spent with

Spends create deposits

There is always a balance and all balances

Thank you for that explanation, and I am sorry to be so rusty but I am in my 15th year of retirement. There is a world of difference between reading a set of accounts and actually creating them.

Back to the issue. I hope that we are agreed that, at the end of a – let’s say £1 million loan – the borrower has repaid the loan and now has his/her property/whatever; the bank has received £1 million plus interest. If you disagree I would appreciate it if you could explain why.

BTW, if you find my persistence curious or annoying, may I just say that getting an answer to “the meaning of life” is easier than to this particular question.

But, as I explained the bank received the payment because of a strong of transactions, all of which balance

In themselves these transactions balance – but the payment to the third party enabled by the initial loan is still out there – and balances the system

They created a new deposit which was a credit in an account and ultimately that balances the debit that cleared the loan – in the system as a whole

You’re trying to view a system as a single transaction – which does not work

Richard, thank you again. However, you appear to be answering the question I asked before the last: that is to say “the bank created money doesn’t disappear.” I have shelved that as dispensable. My question this time is, “when the bank loan is repaid does the full amount of the loan end up in the bank.”

Your answer, about the transactions balancing seems, to me, to confirm my question. The original loan is still out there – as you say – and this is balanced by the loan repayments which are recorded as a credit at the bank.

Nothing ends up ‘in the bank’

There is no such thing ‘money in the bank’

The only question is who is the double entry with now?

This is the but you are not getting

The “economics in one thread” thread last week was excellent. I’ve shared amongst some friends who have moderate interest in politics but little interest in economics and it really hit with some of them.

To quote 1 friend “Imagine being that clever. To understand it but also to package it up in a twitter layman thread”

High praise!

Thank you

But not clever…..just a lot of effort

Most of my knowledge of economics comes from reading your emails and blogs and following up links. I don’t do Twitter but I find your long threads amazingly interesting because of the punchiness and the logical progression of the argument. It’s a bit like a Powerpoint presentation but without the waffle and padding.

The rest of your output is not bad too (that’s the supreme compliment from a Glaswegian).

I am amused

Thanks!

Thank you again.

“Nothing ends up ‘in the bank’ There is no such thing ‘money in the bank’.”

I notice that Barclays Bank bank has assets of just over £1 trillion; I assume that most of that started out as money in Barclay’s Bank.

I do not wish to argue with a chartered accountant the ins and outs of bookkeeping. But, it defies logic for a bank to create – say – £1 million – from nothing and lend it to someone (I realise that that is one process) then receive £1 million in repayments (plus interest) and not to have made any money.

I think, but I’m not sure because, as I explained this is not my bailiwick, that the/my problem arises with the initial £1 million debit to the loan account. In reality the bank has not debited it’s loan account at all, it has merely recorded the creation of £1 million for a loan to a third party.

The last is true

Doesn’t your comment concede a breach of double entry rules? The one that says something like for each transaction both entries must be equal?

Nothing breaches that