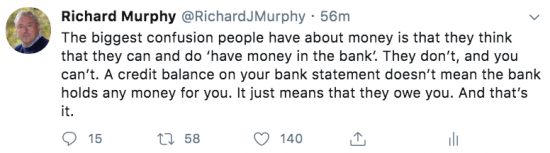

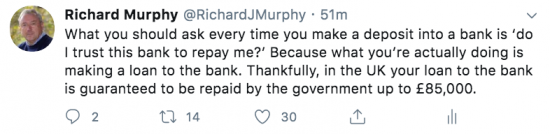

For the first time in months I went out for a coffee this morning, with an iPad of course. And these tweets happened. They are in the right order, top-down.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Thank you Richard,

Whether you write on Twitter or on your blog, I want you to know that I think that you are an excellent writer on these issues.

Thanks

I feel lucky to live at a time when publishing is possible in this way

I honestly think there was never a good understanding of Keynes’s thinking. His central theme was that because the future’s uncertain our economies are therefore by definition always in flux. Life fights hard to make that flux palatable even to the point of trying to lull us into a state of believing that the flux isn’t important hence economists developing their Neo-Classical theories to help us sleep sound at night. Politicians are in the business of selling myths that vote for them and all your dreams will be sweet hence they have a natural affinity with the Neo-Classical economists. You might summarise the plight of the UK as a collective refusal to confront reality, a refusal to acknowledge that economies which are central to our lives are always strongly in flux!

Very good

Rather than the Treasury borrowing from the Bank of England I prefer they divvy up money creating activities. The Treasury creates “inactive” reserves (gilts) – the BoE activates them creating “active” reserves. J.D Alt uses the respective terms “future” and “current.”

http://neweconomicperspectives.org/2019/10/the-peoples-money-part-1.html

http://neweconomicperspectives.org/2019/10/the-peoples-money-part-2.html

Neil Wilson shows that when economic flux becomes crisis the tendency becomes for people to seek stability by swapping some of their “activate (current)” money for “inactivate (future)” money and since there is only one source for relatively stable “inactivate (future)” money a sovereign government’s deficit will increase by private sector demand. (Gold not so stable and secure for a variety of reasons.)

https://new-wayland.com/blog/#Bonds%20Pay%20For%20Themselves

With these posts on MMT I’ve been thinking about the term taxpayers’ money.

I’ve never liked the phrase taxpayers’ money, as it seems it is usually used to try to make people angry.

Then throw in knowledge of MMT, and that taxpayers’ money doesn’t even really exist and it becomes even more frustrating. And it is used so often!

Taxpayers use government made money

Governments do not use taxpayer money

Big heaps of IOUs all over the place!! 😀

I had never thought of the government guarantee on money in the bank that way before, it make so much sense.

In fact, all of MMT makes so much sense that I can understand it. Inflation has no meaning for me when people talk in household budget terms. When I transfer money over online and such like I can visualise what happens now – transfers of debt. I’m less hung-up about using cash now as well, it is just your paper-form IOU. I do however hope that Scotland gets its Scottish pound soon with some nice designs on the notes,,, well, within my lifetime would be nice. Maybe I should get my brain frozen and come back in 10 000 years to see it happen.

Of course, all MMT does is explain how a currency-issuing economy works, so, of course it makes sense, and I even understand how tax is an inherent part of it. It’s when governments and MPs give garbled accounts of how they’ve ‘run out of money’ and such like that I didn’t understand how the economy worked – MMT should be taught to primary 1 children along with leaning their numbers!

Yay!

I am pleased

But The Blessed Margaret says government’s have no money of their own:-

https://www.thelocal.de/20101007/30325

I saw and retweeted some these yesterday and I am glad you have set them out here as well – they are very clear and easy to read. Will include a link in my next blog post.

Thanks

Admirably succinct!

Just a little more explanation is needed I think.

What is promised? That is, what is it to pay?

I suggest that payment is substituting one promise for another. When A promises B payment, A pays by substituting her promise to B with a special kind of promise from G to X, where G is the Government and X is anyone.

I will be exploring this further…

As I understand it, there was a time when the pound sterling was backed by gold deposits, and you could (at least theoretically) ask the bank to give you the gold equivalent of your money (there was a time of course when the physical money itself was made of gold or silver). These days, if you ask the bank for “your money” they will give you a banknote – that is, replace one promise with another. The important point is that someone else will accept that banknote (or equivalently the swapping of promises when you make a bank transfer, or use a debt or credit card) as being “worth” that amount.

But how is something like Bitcoin, a currency without the backing of a national government, analysed by MMT? Or a multinational current like the Euro?

And tax is what gives money that trustworthy value

In contrast Bitcoin is not currency

It is a speculative asset. It’s no more money that shares in BP are

What I didn’t make clear was the conceptual problem: if money is a promise to pay, then payment can’t be of the thing, money, since that would be a circular definition.

Money is not a thing. That’s why I suggest “paying” is substituting one promise for another.

But I must admit I haven’t allowed this idea to fully percolate in my mind. There may be more to sort out.

I admit I am not following you

Money is simply information, but information is a thing.

It is circular. One debt is replaced by another and the pile of debt and hence the pile of money keep on growing.

As you (Robert Fox) say, money is not a thing in itself, it is a representation of a thing. It represents an amount of value, which can be exchanged for anything of equivalent value. The “promise to pay the bearer on demand” written on it is a leftover from the days of the gold standard. In reality, it makes no sense now because all you would be requesting is another representation of the same value – which doesn’t exist. There is only one sovereign currency – for obvious reasons – in any sovereign state. The promise is that the value on the note or coin will be backed by the government so that it continues to be possible to use it to exchange for something of equivalent value. That’s all.

It’s great to read the rising number of comments from folk who are “getting” the MMT message. The “promise to pay” backed by a sovereign government is the most secured investment/ savings account on the planet. The real money men in our society know this fine well. Back in the day, it was old Etonians who were the “jobbers” for Gilts in the City.

Our leaders are very scared at the prospect of defending austerity as a POLITICAL decision. Especially after the largesse shown to the banks in 2008/09.

Richard, you have shown that economics as an academic study has been hijacked by the neoliberal right and that the progressive left now have the MMT “back up” to take the debate forward.

Thanks

What does the verb “to pay” mean?

It can’t take the direct object “money” for that is to fall into circularity of definition, when money is itself defined as a promise to pay.

To pay is to fulfil the promise. What fulfils and cancels the promise? If it is not forgiven (written off) by the promisee, then it is achieved by the substitution of another (very special) promise from G to X. Like a cash cheque signed by the Government, payable to bearer. This promise is so absolutely certain and secure that it need never be paid; the very existence of this promise is equivalent to its fulfilment. (One does not bother to take one’s currency banknote into the Central Bank to ‘cash’ it.)

When A pays B, she draws on her stack of G to X promises and substitutes them for her promise. B accepts the G to X promise as fulfilment of A’s promise.

As I said, the G to X promises need never be fulfilled (which is just as well,) since what possible promise would serve?

I am trying to be as clear as possible!

Hi Robert,

It sounds like you’re suggesting something similar to my comment at the top of https://www.taxresearch.org.uk/Blog/2020/07/17/todays-video-modern-monetary-theory/

Johan,

Anyone can try to create money, that is, try to make a promise to pay (using Richard’s definition of money), but it’s only created if the promisee accepts the promise. The promiser has to be trusted. The Central Bank is the ultimate trustworthy promiser.

My original post deals with a lacuna in the definition of money as an promise to pay.’ We know what it is to promise, but what does ‘pay’ mean? It can’t mean ‘pay money’, because then the definition of money is “money is a promise to pay money.” So pay must mean something else. That’s the issue I have tried to resolve.

I don’t think this is useless hairsplitting. Because until the problem is resolved, the definition can be justifiably attacked as incoherent or incomplete.