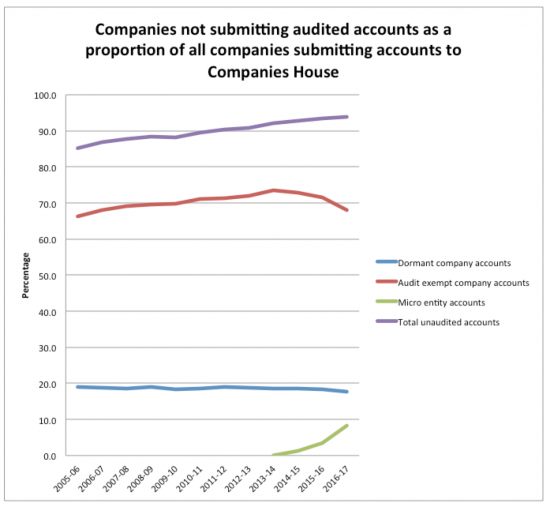

I have continued to work on UK Companies House data. One of the trends I have noted is the rise in the submission of unaudited accounts to Companies House. The data that I have is as follows, all secured from Companies House publications over the years noted:

At one time (when I began my career) all limited company accounts had to be audited. There was a good reason: parliament had decided that limited liability was a privilege that should not be abused and audit was considered to limit the risk of that abuse.

From the 90s onwards the audit requirement was steadily reduced. As will be noted, it has now reached the point where 93.8% of all accounts submitted to Companies House are unaudited.

There are two questions to be asked. If this is the case how reliable is this data? And who knows?

My suspicion is those with the power to regulate a) do not know and b) do not care.

I do. So do those who lose as a result of the abuse of limited liability.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

I do the accounts for a small local charity. Our accounts have to be audited and signed off every year. How is it that the big fish get such an easy ride?

Excellent question

Apparently charities are much more vulnerable to abuse…

“Apparently charities are much more vulnerable to abuse…”

And audit has bugger-all to do with reporting to shareholders.

Of course, you did your training such a long long time ago Richard and the world has moved on since then. Who are audits for? The shareholders of course. HMRC has their own way of delving into a company’s finances so it’s for shareholders. To check on those managing the company. That they are running it properly on behalf of the shareholders.

The vast majority of companies these days have the same managers and owners. What they call “owner managed businesses”. There’s just no need for an audit.

But don’t worry. Even if a company is otherwise exempt, did you know that it only takes 10% of shareholders to demand an audit.

I can understand your confusion. The world must seem so different from when you were young. Or even from when you were working in the profession rather than just commenting on it .

But there’s no need to go scare mongering!

You clearly have very little idea about audit

They are very obviously not just for shareholders (even if the profession of which I presume you are a part) likes to maintain that pretence

They are for the benefit of all stakeholders, just like accounts themselves

The profession once knew this. Now they deny it. Read this https://www.icaew.com/library/subject-gateways/corporate-reporting/the-corporate-report

And maybe being a little less patronising might help you make a better case: it’s just a bit of free advice you might find useful

Gillian Smith says:

” HMRC has their own way of delving into a company’s finances so it’s for shareholders. ”

HMRC has a very narrow brief, related to tax due. Nothing whatever to do with the health of a company.

“Who are audits for? The shareholders of course.” That works well doesn’t it ? When big companies like BHS and Carillion go down the tubes the shareholders are the last to know. By which time they’ve been fleeced, along with the pensioners and the company’s suppliers.

If your comments are representative of modern standards, much is explained. But as long as you get your fee why would you care ?

Christ All-bloody-mighty. What is the point of such an ignorant and patronising response? If you have nothing better to say for yourself, please don’t bother.

That hit a spot, then.

😀

Mr Murphy, I am not sure if you appreciate this, but it is the EU that led deregulation in this area. The 2013 Accounting Directive expanded the UK’s small company audit exemption. If you disagree with the rules you should be pointing the finger at the EU.

GG

I am aware of it

But it was a trend we began of our own volition a long time before that

“But it was a trend we began of our own volition a long time before that.”

You’re incorrect there, Richard. The audit exemption for small companies was first introduced by the Fourth Directive (78/660/EEC) in 1978. The UK considered applying it several times in the 1980s but it wasn’t until 1994 that the £90,000 threshold was introduced, which was significantly below the then EU small company threshold (increased to ECU 5 million by directive 94/8/EC in 1994). It wasn’t until 2004 that the UK audit threshold was increased to the then EU thresholds. It’s a European path we followed from the beginning.

Gillian is correct about how the audit report is for. The Corporate Report identified users of the accounts but it does not comment on the audit report. The latter is governed by tort law as most famously determined in Caparo and later Bannerman. Hence why every audit report is explicitly addressed to the members of the company and contains some form of Bannerman wording exactly who the audit report is for. Anyone else relying on an audit report does so at their own risk.

I gave to say that it’s apparent we did make our own choices so you argument is wrong.

And as for the audit, I simply have to disagree. This argument is narrow minded : only the profession holds it. Your own argument is simply an expression of that, and the law was made to be an ass.

In that case I am completely entitled to take a different view, and to suggest it is right. It is something I have successfully done for some time, with the profession invariably being proved wrong. It will be again.

Georges Gravelle says:

” If you disagree with the rules you should be pointing the finger at the EU.”

Oh ! Good.

We’ll be seeing a whole new era of transparency after March 2019 when the Brexit arrangements free us from adherence to the lax regulation of the EU.

I shall look forward to that.

I am surprised to hear you say that, because the two lines in your graph are closely aligned until 2013. It shows no evidence of divergence before then.

GG

The top line shows a steady rise

That’s my concern

All three are unaudited

Although the Audit Report may ostensibly have been for the benefit of the shareholders the fact that an audit had been performed and a degree of professional scrutiny carried out ensured that creditors, many of them small businesses and traders, were supplied with some measure of the management and solvency of the businesses with whom they did business. By reducing the audit requirement this safety-net has been withdrawn and increased the risks to those who supply credit. Although banks will insist on high levels of reporting to safeguard their loans other creditors will only have the statutory reports filed by the business. Owner-managed businesses may well not see the need for an audit but when those businesses get into difficulties it is the creditors who suffer not the shareholders.

Simon

Precisely

Just as auditors sought to shift their risk to creditors (and by and large have succeeded in doing so, at cost to us all) so too have companies themselves sought to mitigate their liabilities

Of course, all of this is anti-competitive, which those who trumpet it usually completely ignore. Free markets require level playing fields. This was why Adam Smith was so opposed to limited liability and the abuse it permitted

Richard