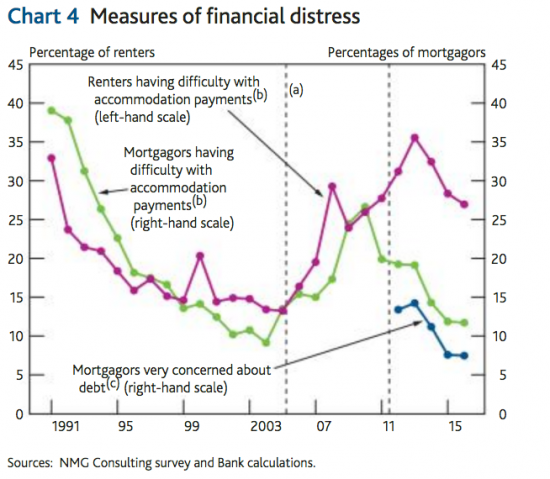

The new Bank of England Quarterly report contains the following chart (page 192):

The BoE discussion focusses on interest rates, unsurprisingly. I note three things.

The first is how closely mortgage and rental payment difficulties tracked each other during much of this period.

Second, how this totally changed in the period of low interest rates.

Third, that rental concerns remain out of all proprtion to the past.

If there was a graph to show a divided society this might be it.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Although I don’t have the data I think it would probably reveal a series of crescents and dips since the early 1970’s when the commercial banks were first allowed to blow house price bubbles by both Conservative and Labour governments. This would also coincide with UK governments dropping Keynesian insight (Functional Finance) for Neo-Liberalism in regard to understanding how the country’s fiat monetary system works and how global outsourcing affects economies because the value of money can be manipulated. Effectively the UK has been going through a period of economic stupidity for seventy odd years because of market fundamentalist ideology which refuses to recognise the reliance on and necessity of “Institutional Entrepreneurship” (Intervention).

http://community.middlebury.edu/~colander/articles/guiding%20the%20invisible%20hand.pdf

The gap between mortgagors and renters will continue to widen. I see no political or economic force in play that will counteract this: there is every reason to believe that current trends will accelerate.

Further: the exploitation of renters will worsen. They have no economic leverage whatsoever – withholding payment is a non-starter – no access to the courts for redress save by the charity of others, and no significant political party represents their interests.

I personally find it quite surprising that there the people having difficulties with mortgage payments aren’t very concerned about it. I would expect those two lines to be the other way around.