The FT notes this morning that:

Britain has been issued a fresh warning over its poor record in innovation and embracing technological change, with new estimates showing a key measure of productivity fell in 2014 for the third year in a row.

The report refers to one measure of productivity. Others suggest matters are much worse.

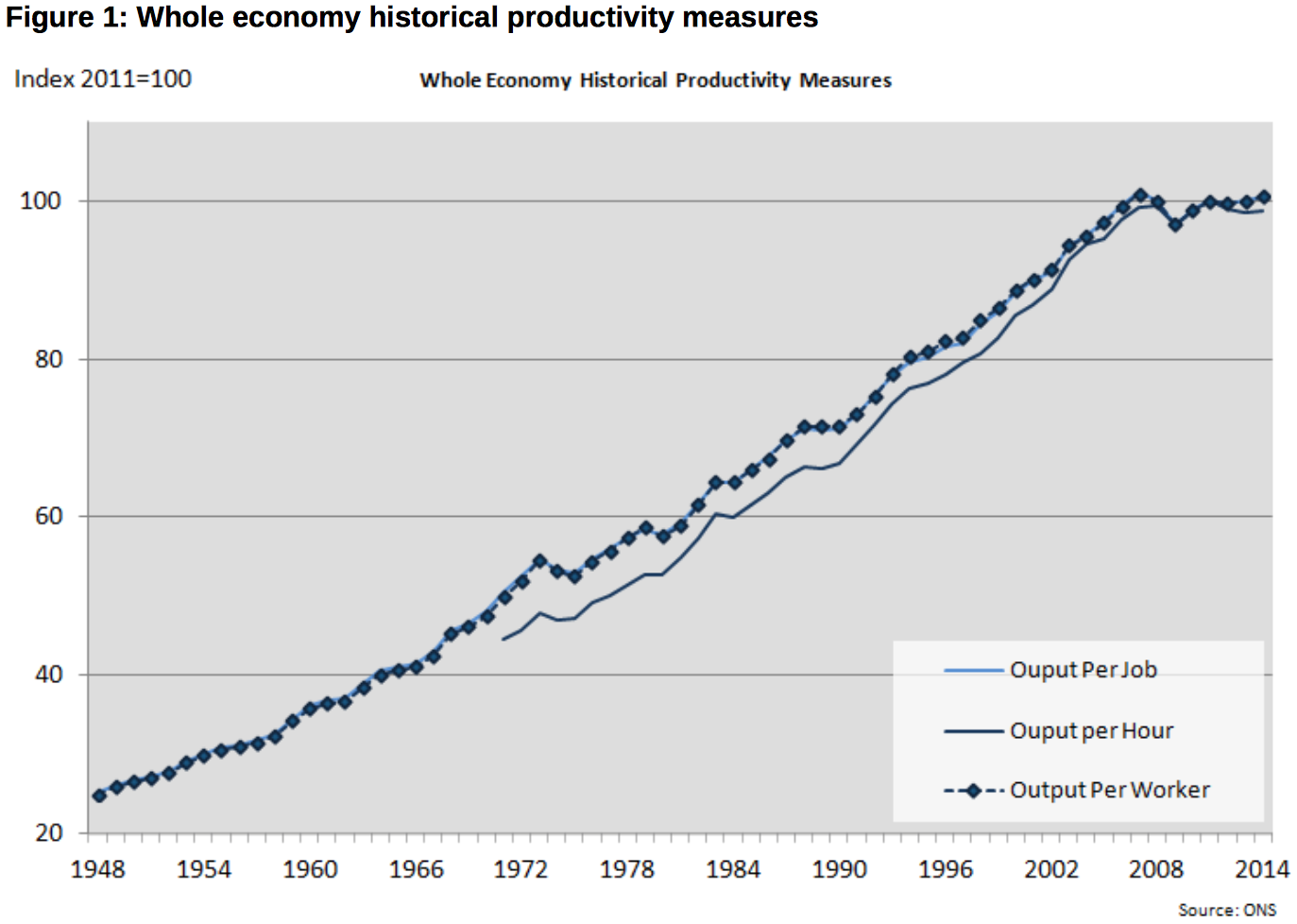

A much more detailed analysis of this issue is provided by the excellent Flip Chart Fairy Tales web site. This graph, borrowed from there shows the ONS data:

The UK has been flatlining since 2007 on output per hour. Growth has only come from increased hours.

The UK has been flatlining since 2007 on output per hour. Growth has only come from increased hours.

This is dire, and leaves the UK out of line with many of its competitors. The explanation, again from the Flip Chart web site:

LSE's Centre for Economic Performance published a pre-election briefing on productivity a couple of weeks ago. Among its conclusions:

"UK GDP per hour is currently around 17% below the G7 average. This is due to low investment especially in infrastructure and innovation, poor management and weak intermediate skills."

We are not enjoying an economic miracle in the UK. We are suffering enormous strain because we'd rather not invest so that managers and banks can make short term gains and we'd rather create low paid jobs than provide people with the skills they need.

This is the crisis that any new government needs to address after 7 May. Labour's pale green new deal is welcome in that respect. But what we really need is a clear, funded and coherent industrial policy. A proper Green new Deal could be just that. And no one else but government can deliver this change that is so necessary. That is what government is for and to suggest that this issue can be left to the private sector is absurd: they created it in the first place.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

This is exactly the result you would expect to see in an economy where capital is being extracted from productive enterprise and redeployed into rent-seeking.

Also: the turn of the century marked the effective end of manufacturing as an engine if economic growth in the United Kingdom – New Labour benefited from an asset bubble and service sector growth in a severe industrial recession – and the levelling-off in 2002 marks the end of the productivity gains from desktop computers in the service sector. Other countries have made continuing gains from that, but there’s nothing on the table except call-centre jobs in an economy with no mid-level education.

I recommend anyone interested go listen to Terry Smith’s annual presentation to Fundsmith investors: it is on the Fundsmith website. He vividly describes the Jack Daniels brand, and how it went in 30 years from being a provincial US product to a global brand because it was owned by a family who were willing to invest in building up relationships and logistics in foreign countries over a long period of time, at significant short term cost to the company. They could accept 5-10 years of reduced profits because they could see at the end of the process they would have a much bigger brand.

And he compared it to Cadbury, which was doing something very similar in China at the time it was bought by Kraft. Kraft’s main concern was short-term “shareholder returns”. They pulled the Chinese infrastructure, wrote off the investment, and Cadbury will probably have lost that market forever.

What is heartening is that some fund managers – Nick Train, Terry Smith and Neil Woodford spring to mind – are now starting to say that long term investment is the only way to make significant returns. But most look only at short term shareholder returns and I suspect that is why, in the medium term, most value created in the (private but quoted) UK economy will be acquired by Chinese and German investors who are capable of taking a long term view.

I agree, longer term investment and risk taking required. Evidence – I am a research scientist/engineer and collaborate with large companies, no names, who are cash rich. One world leading brand wants virtually all the funding for a very exciting scientific instrument [not a small product], my team is developing, to be paid for by taxpayer grant funding. There will be in-kind contributions but not sure how much these will be, no hard cash on the table. This project is near market, only one part blue sky. I see many other similar projects in the same circumstance.

As far as I am aware, even though we are working harder, our productivity is still mediocre, and has been since…hmmm…..let me se……….ah yes – since the Thatcher years apparently.

Which might explain why, despite the ‘jobs miracle’ proclaimed by the usual suspects on the right, the party that likes to claim its the party of wealth creation isn’t going anywhere in the polls. I’m just rereading Ha Joon Chang’s excellent ’23 things they don’t tell you about capitalism’ which explains, from the PoV of an economist who himself believes the market is the best way yet found of creating wealth, why the free market dogma of deregulation, ‘private good, public bad’, shareholder value etc doesn’t work in the long run.

It should be compulsory reading for all the right wing idiots still desperately clinging onto their neoliberal dogma.

It is a great book that one.

But neo-libs don’t read: they ‘feel’and construct realities of their own that make them feel happy.