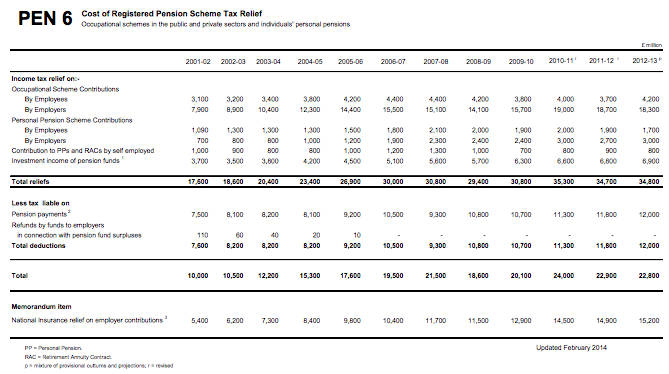

I wrote on this blog last week about the £50 billion annual subsidy given to pensions each year. Some have argued the true figure is £38 billion but that is not true. We would recover tax on pensions paid out of past contributions whether or not we give current contributions. So £50 billion is definitely the correct figure and comes from the following table for the tax year 2012/13 and represents total tax cost of £34.8 billion plus total NUC cost of £15.2 billion:

Let me put that in context. Total UK tax receipts were £556 billion in that year (page 108, here). So in effect £1 in every £11 of tax receipts was spent subsidising the pension savings of those in the UK who were, by definition, at least well off enough to save, whether personally or by taking a job where part of what they might otherwise earn was diverted by their employer into a pension fund. There is no reason to think that situation has changed now.

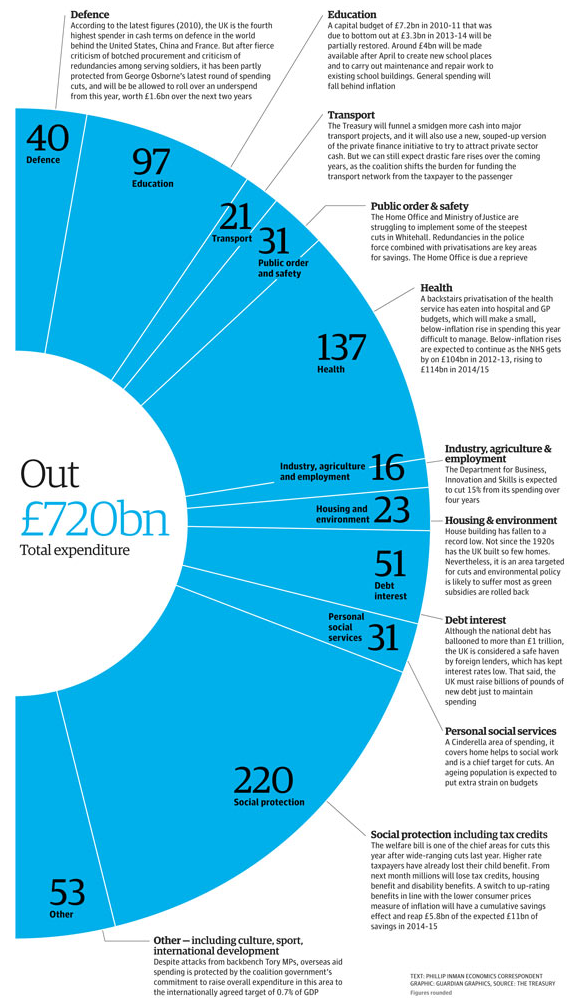

Let me also put that spend of £50 billion into context that year. This is a Guardian summary of government spending in 2012/13 based on Treasury data:

So, £50 billion comes in bigger than anything but education, health and social security and near as makes no difference the same as debt interest - until one realises that about one third of that was actually paid straight back to the government as a result of quantitative easing and so the real figure was about £35 billion there.

The amount we spend subsidising the pension savings of the wealthiest people in this country is our fourth biggest state spend.

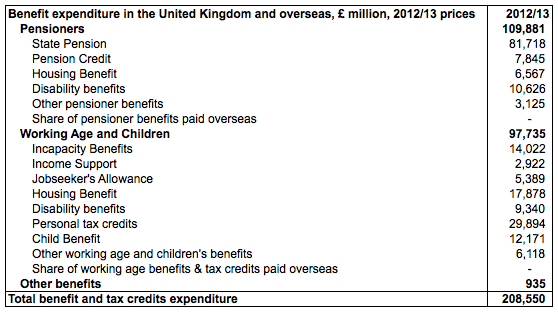

Let me put this figure into another context which is the total state spending on pensions in 2012/13, which is, again, the year for which most accurate data is available, was £109 billion, as shown in this table:

State subsidy of private pensions does then cost 45% of state pension spending or, if the total is aggregated 31% of a combined spend of £160 billion.

Let's also put the number on the context of total non-pension social security spending - again using 2012/13 data - which as the table shows was £97 billion. In that case the subsidy to pension payments for those in work who can afford to save is near enough half that of all spending on those who cannot make ends meet.

Then let me put this in another context. The benefits cap of £26,000 that the Conservatives want to reduce to £23,000 supposedly saves at most £110 million a year - or 0.22% of the cost of private pension subsidies each year.

And the child benefit cap Labour is proposing will supposedly save £400 million a year - or 0.8% of the cost of private pension subsidies.

Why make these points? Precisely because they make clear that all this discussion on austerity and benefits and the need to cut down is completely missing the glaringly obvious point that whilst the poorest in this country will be hit hardest, as will families with young children, those who can afford to save are getting a massive state subsidy.

Is that just is the first question?

How can it be when we are facing austerity that one of our biggest state spending categories is intended to redistribute wealth upwards?

And how can it be that we are willing to suffer such enormous tax leakage on this because even if tax is eventually paid on some of the pension recovered the following have to be taken into account:

a) Usually up to 25% of a fund can be taken tax free

b) There is never a penny of recovery on the NIC cost of contributions

c) Income tax is almost invariably recovered at a lower tax rate and many years in the future, if at all.

Take these factors into account and the chance of future tax recovery from these reliefs is well under £6 billion in my estimate, and quite probably less in current terms. This really is the most massive tax give away, and almost all of the funds in question are taken out of the productive economy, moved into City based speculative activity where almost none leaks into real investment activity but vast amounts are lost in paying enormous sums to those working for City institutions that only goes to fuel even greater inequality.

And, as I showed in my 2010 work on this issue, the subsidies given to in fact cover the entire cost of all private pensions paid in the UK right now - suggesting that in fact all pensions are really paid at direct cost to the state anyway but with massive rake offs for for the financial services industry ion the way.

If you were to design a way to provide pensions this is about the worst one possible.

And today George Osborne wants to make it worse.

The time for reform is now. But no one wants to talk about it.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Am I misreading the data, or is that the value of relief on all pension contributions? I.e. Is that the income tax/NIC charged on all the contributions into all public and private pension schemes?

If so, then your attribution of it to the ‘wealthiest’ requires some support, and I’m not sure it will stand up.

For example, 85% of the value of relief on employer contributions is on occupational schemes. What proportion of that is public sector schemes? What proportion relates to the wealthy beneficiaries of those schemes?

Whilst there are still some occupational and final salary schemes for the very privelaged few in high-paying private sector jobs, most people have now been pushed into private schemes. The disparity in the numbers between Employee and Employer relief on occupational schemes suggests that public sector schemes are heavily reperesented (as they typically have a heavy bias towards employer contributions).

This report values higher rate tax relief on pension contributions at £7bn: http://www.cps.org.uk/publications/reports/costly-and-ineffective-why-pension-tax-reliefs-should-be-reformed/

That’s a big number, but not £50bn. If the CPS numbers are to stack with the numbers you’ve given then that £7bn must include employers contributions. If we add NIC in proportion we have a total cost of £10bn. That means 20% of the £50bn is related to higher-rate earnings. Let’s double that because to get the higher rate relief they must be getting the basic rate relief too. So £20bn, or 40%, might be going to people who are higher-rate taxpayers. Am I wrong?

We can argue about whether everyone on higher rate tax should be categorised as ‘the wealthiest’, but even if we accept that they should – that still leaves 60% of the relief going to basic rate taxpayers. A large proportion, I would suggest, to those in public sector schemes.

Saying that pension tax relief is all going to ‘the wealthiest’ seems to be as credible as saying that a £2m mansion tax will hit ’the middle class’. i.e. not very.

You are quite right in noting that the £50 billion I refer to is all pension contributions at all income levels: I have never disputed it, and I’ve even been explicit about it, by noting that this does include those who can forego current income by choosing to take a job where part of their remuneration is settled by way of pension contribution.

Your estimate of the relief going to higher rate taxpayers may be right but if that is true they represent approximately 10% of all taxpayers but are getting 40% for relief and are already, by definition, well into the top half of the income distribution. It is also true that many of those who are getting tax relief at basic rate will also be earning above median pay and are well known to be amongst those who are very resentful of benefits paid to those on lower income, whilst happily taking reliefs available to them.

But, to counterbalance this, I am not actually asking for all income tax reliefs on pensions to be withdrawn. I am saying I see no reason for any National Insurance relief at all because I see no potential payback on this, and so it is a straight subsidy when the person no longer contributing in full will still be expecting all the benefits that another person receives. I do not think that any tax relief at higher rates is appropriate. I do think that as a condition of tax relief condition should be applied to the ways in which pension funds should be invested so that the majority of the funds available are not invested in the casino that is the stock exchange. I think that tax relieved savings should be used for the benefit of the national economy as a whole as well as for the benefit of the individual who benefits. So I am not actually arguing against the existence of pension funds per se and therefore those about whom you have concern are not my primary target for comment.

But, that said, the proposals I suggest here would save many billions (£15 billion of National Insurance for a start plus a significant element of income tax relief) with regard to reliefs on funds going into pensions whilst directing very many billions more into productive use in the economy. That, I would argue, is what a good Chancellor should do to ensure effective use of the funds over which they have some influence. What we have at present is negligent management with regard to this issue, and that is my point of differentiation.

Thanks for your response. I don’t support those proposals (unless as part of far greater reform to public, private and state pensions) but they are not unreasonable or illogical suggestions.

I do think your wording is very misleading though. I don’t think anyone would consider that ‘the wealthiest’ is the right word in this context.

That is because of the enormous ambiguities that exist with regard to perceptions of wealth. Anyone earning over £26,000 a year is in the top half of the income earning profile albeit, and I fully recognise this, they are hardly well off. Those who are paying higher rates of tax may well be in the top 10% of income earners. They may not think they’re well off but very clearly compared to the majority of the population they are. Perversely, most of those who are learning a great deal also think that they earn very much less than they really do in proportionate terms. We need to educate ourselves better, is my point

“So £50 billion is definitely the correct figure and comes from the following table”

Even this table shows the £12bn being offset. There are 3 lines called: Total reliefs, Total deductions, and Total.

Why do HMRC present it this way? Because it would be misleading if they did not. Or is this another case of everybody else (including HMRC) being wrong, and Richard Murphy being right?

Yes, HMRC are wrong.

Just as they’ve said Google don’t avoid tax and yet today the Chancellor says he is going to raise hundreds of billions closing their tax avoidance

As usual, I was right

And as ever, you’re backing the wrong side

An interesting breakdown. So, of your £50 bn:

* about £22 bn relates to income tax reliefs on contributions to occupational pensions (but presumably not state occupational pensions, which by and large are unfunded, I believe)

* about £5.5 bn to income tax reliefs on contributions to private pensions

* another £15 bn on NICs reliefs

* another £7 bn for relief of tax on investment income of assets held by pension funds

Presumably corporation tax relief on employer contributions should be added, or is that already included in the income tax line?

Assuming that the last two in the list divide roughly pro rata to the contributions, occupational pensions get about 80% of the tax reliefs each year. “taking a job where part of what they might otherwise earn was diverted by their employer into a pension fund” is a peculiar way of putting it. Are you against occupational pensions? Or just tax reliefs on occupational pensions? Most of those in occupational pension schemes are not the 1%, surely.

It is difficult for anyone to get ridiculously rich through tax-relieved pensions savings. The annual allowance (the maximum contribution that qualifies for relief) is down to £40,000 now, which is still quite a lot but somewhat below the £255,000 that Gordon Brown set originally, and the lifetime allowance has been reduced too.

So, is your proposal that the state pension will be increased so there would be no need for tax relief on private pension provision? The figures above show that state pensions cost about £80 billion per year, so adding £50 billion could increase the weekly pension from around £110 to around £180, which nicely falls within the £10,000 income tax personal allowance.

If I as given a choice on how to spend £50 billion your last proposal would make a lot of sense