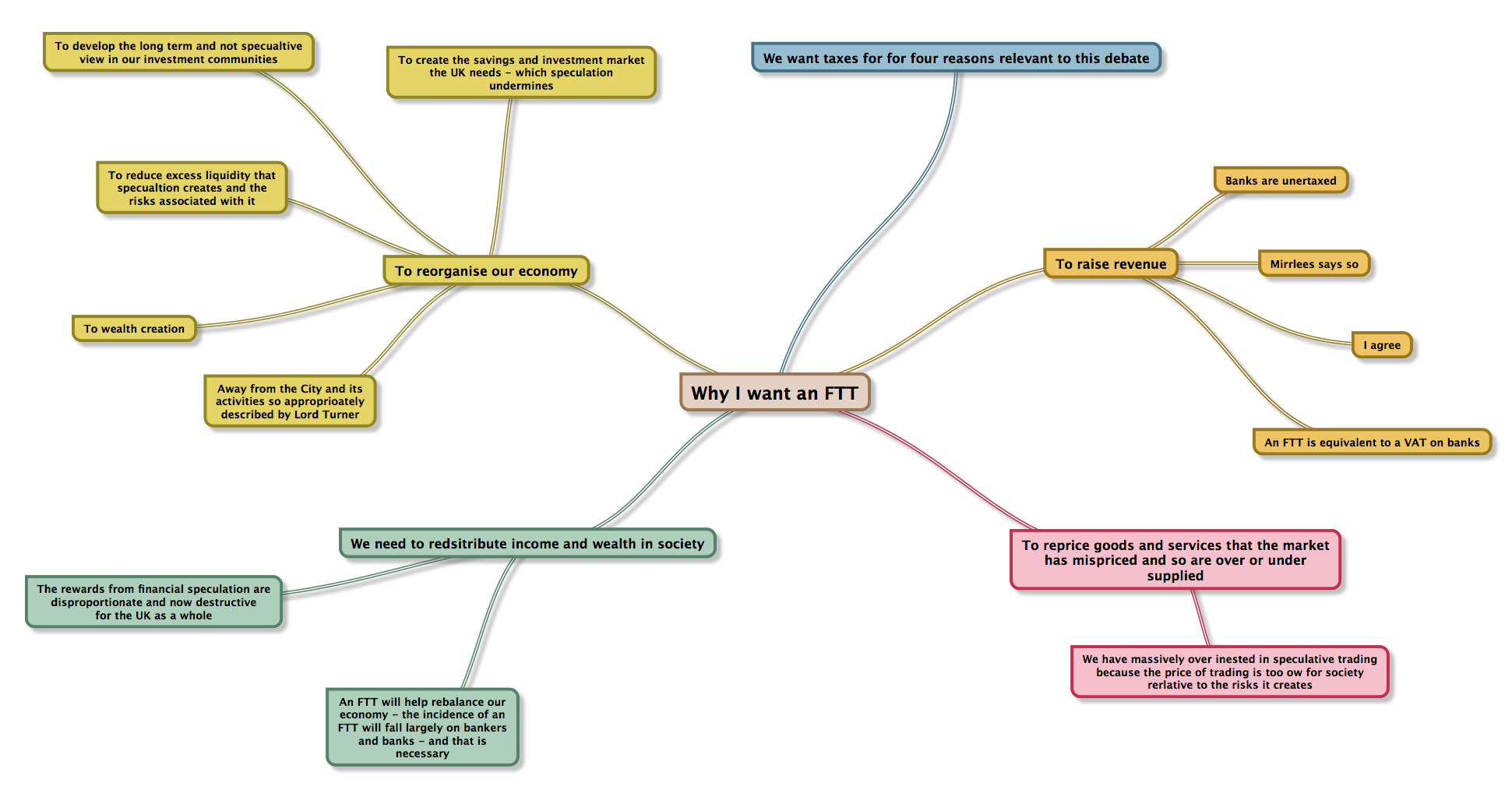

As I have mentioned, I spoke on financial transaction taxes at the Law Society last night. These were my speaking notes:

Start in the blue box at 1 o'clock and work round, clockwise.

Click on the image to see a larger version.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Richard

Interesting notes. Interested in what evidence you have that the incidence of the tax will largely be on banks and bankers?

TP

See ‘Taxing Banks’

I wrote it 5 years ago

What about pension funds and insurers?

The Dutch central bank estimate that half of the tax would be collected from pension funds and insurers: http://www.dnb.nl/en/news/news-and-archive/dnbulletin-2012/dnb267803.jsp

Even the Commission says that:

“However, it cannot be taken for granted that this assumption necessarily holds since it also concerns the activities of financial intermediaries such as pension funds, which also manage the savings of middle- and lower-income earners.”:

http://ec.europa.eu/taxation_customs/resources/documents/taxation/gen_info/economic_analysis/tax_papers/taxation_paper_25_en.pdf

How can you say largely banks without mentioning pension funds?

Pension funds should stop trading in the way they do

Maybe they would earn a return for their members then rather than let it be captured by their fund manages and advisers

If the charge fell on pension funds I say good: we will have better pension fund management for the long term as a result

And that is what we need

Richard

That might be justified if the tax were focused on unnecessary trading but it isn’t. For example, even if a pension fund just buys a second hand corporate bond and holds it to maturity then there are two FTT hits (purchase and redemption). Why? And pension funds are big users of swaps to properly manage assets and liabilities as a standard tool of the trade to control risk. Why tax those transactions?

The fact is that the FTT is the wrong tool to achieve the stated objective of getting the institutions that caused the problems to contribute to the cost. It just won’t do that. The FTT is going to be borne mainly by the customers of the FS industry as a whole, not the banks. Those customers who probably are having difficulty saving because of the general economic climate. It will raise the cost of capital for everyone. That will make it harder for manufacturing and other sectors to invest. It will cut GDP and depress demand. That’s all in the Commission’s impact assessment.

Pretty much all of the problems that the proposals have run into are because the Commission unaccountably chose FTT over a FAT, which would have been much easier to design within the EU treaty, actually have targeted rentiers in the banks and made the polluters pay.

What we’ve got now is a bad tax that’s being badly implemented but none of the designers/boosters are interested in looking at the evidence.

TP

I cannot see your issue

Why shouldn’t a pension fund pay tax on its transactions?

Is GDP from dealing in second hand shares what we want?

Why will it raise the cost of capital? Much capital is never traded

That which is is rarely related to the raising of business capital e.g. equity issues contribute very little at all to business capital now

I’m afraid you want a tax that suits the City

I don’t

I’m confused. I thought this was a tax on banks to recover the bailout money?

That is the bank levy

Which is a token gesture

If that was just a token gesture then why not have a large levy instead of taxing pension funds?

Please read what I wrote about the role it can have in creating behavioural change

That’s why it is needed

The revenue is less significant than that

Is it that hard to understand?

I see where you’re coming from on behaviour, not disputing that point at all, but that means you need to target the behaviour you want to change. I just don’t see that my pension is what you should be taxing rather than speculative activities in banks or hedge funds or whatever – or bad lending to property developers, which is what has killed us on this side of the Irish Sea.

Maybe you should look at your pension return and wonder why I want reform

19% on my defined contribution scheme over here (I keep that in a couple of passive funds and only ever look at those a couple of times a year). I’ve also got some final salary benefits accrued from some years work in the UK. Those grow at UK RPI. So not bad. How about yours?

The normal rerun is at best the return of funds contributed

Your experience if true is exceptional

I also suggest your two year view is naive, politely

Well last year was a good year – most markets bounced back so 19% is nothing special. I’m not taking a two-year view by the way. I think you’ve misunderstood what I wrote – my fault I’m sure. I only look at the funds a couple of times a year because you shouldn’t switch around very often and I only use passive funds because anyone who pays for an actively managed fund is foolish (in the long run).

Richard

Thanks for the reply. A few comments on your comments – yours shown as quotations:

“Why shouldn’t a pension fund pay tax on its transactions?”

That’s a policy point so I can’t give a “why”. I wouldn’t do it, but it’s a policy choice not a principle and others will disagree.

“Is GDP from dealing in second hand shares what we want?”

That’s not what I was referring to when I mentioned a GDP reduction. The FTT would reduce GDP generally, not from trading equities. The Commission estimates that “the possible deviation of GDP was established at – 0.28%”

http://ec.europa.eu/taxation_customs/resources/documents/taxation/swd_2013_28_en.pdf

That’s year on year loss of GDP due to the tax. By the way, the Commission’s estimate is the lowest I could find and depends on an increase in cost of capital of only 7 basis points (see my response to your next point below). Even on the Commission’s estimate the GDP loss is comparable to the tax revenue.

“Why will it raise the cost of capital? Much capital is never traded”

It will raise the cost of capital for debt and equity even if the instruments are not traded. You can’t get the money back out of the instrument without suffering one FTT occurrence – even for an instrument that is bought on issue and then held to maturity. It’s an unavoidable extra cost so it comes through into cost of capital. That is not a controversial statement honestly. Everyone, including the Commission agrees on that (it’s true for stamp in the UK by the way). The Commission’s estimate is that “the tax is simulated to increase the cost of capital by about 7 basis points” (same link as above). Again that’s the lowest estimate I could find but even that would be a significant extra cost for industry when it raises debt finance (again see my response to your next point below). This is one of the drivers of reduce GDP.

“That which is is rarely related to the raising of business capital e.g. equity issues contribute very little at all to business capital now”

That’s true for equity – I think the figure is about 10%? But the FTT applies to debt issued so if if a manufacturer issues debt to finance a new facility then it will face an increased cost of capital. That means that some investments will no longer be possible. German manufacturers in particular sees that as an enormous problem – they can borrow pretty cheaply at the moment so the 7 basis points increase would be a significant increase in their borrowing cost.

“I’m afraid you want a tax that suits the City”

I would go for an FAT. The tax base would be bank profits plus bank remuneration. The rate would be set to recoup as much as governments wanted. That could be equal or greater than what an FTT might raise. Why is that a tax that suits the City?

I’m afraid that FTT is just not a form of tax well-suited to what the FTT-zone governments want to achieve, which is one of the reasons why they are making such minimal progress in inter-governmental discussions. An FAT could be targeted much more accurately and would use the data that tax authorities are already collecting for corporation and payroll taxes so it would also be cheaper and quicker to implement.

I respect your views

And thank you for airing them

But we clearly differ – and I think you’re ignoring the behavioural on sequences of an FTT which would reduce the supposed costs you identify and benefit society

Any problem with my last post? I’m curious because you have accepted a number of others since I posted it.

TB

I am thinking about it

The BIS triennial report just showed that speculators are doing €5.3 trillion a day in Foreign Exchange ($1.375 quadrillion a year). 40% of this is done in the City of London. Can anyone argue that this has any useful function, apart from allowing traders to siphon money out of the system?

Despite the fact that the financial markets can do all this foreign exchange tax free, when I use my credit card in a foreign currency, the card company charges 2 or even 3% for multiplying the value by the current exchange rate. And these people claim that 0.05% would put them out of business?

Totally absurd.