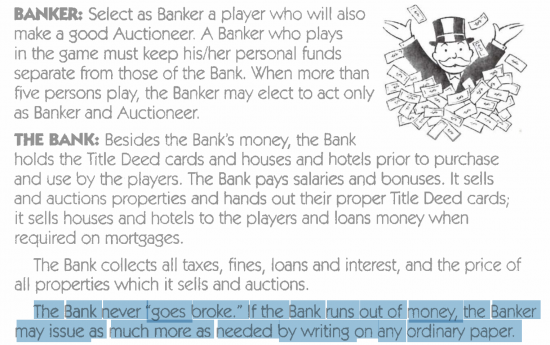

Based on comments received on the blog this morning I realised it as time I reacquainted myself with the rules of Monopoly. This is because of the comments made in last night's political debate. On doing so I discovered this (I added the highlight):

Monopoly reflects real life perfectly: the central bank can never run out of money. If it does, it can just create some more.

And because that is true to life that that's exactly why the UK can never go bust as long as it always borrows in sterling.

In fact, it's why, the government need not even borrow at all if it does not want to do so. After Brexit the Bank of England can simply make as much money as is needed to make the economy go round. No more, I stress, but definitely no less. That's what it has to do, with full employment as the aim.

Refusing to make the money needed to deliver that goal would just be callous. It would stop the game, just as in Monopoly, but with far more serious consequences in reality. But the Tories don't seem to realise that, which is why they guarantee us continuing hardship.

I hope YouGov are right: this election deserves to be a closely called thing.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Richard,

We can all learn something from Monopoly.

Even though there is a universal basic income – passing go – which keeps the game going for longer, the biggest landowner still sucks up all the money and eventually destroys the economy because there is no tax on wealth!

Even though it was invented to make exactly this point, the message was deliberated removed. The landowners decided that Henry George had to be stopped and he was stopped. History was rewritten, Monopoly became just a game – nothing like real life.

If you want to teach economics in schools, playing Monopoly is not a bad place to start.

It’s actually remarkably good…

Just don’t mention that it is in fact an anti-exploitation game…

I believe it is discussed in Kate Raworth’s highly acclaimed book: Donut Economics

reviewed here by Simon maxwell http://www.simonmaxwell.eu/blog/doughnut-economics-seven-ways-to-think-like-a-twenty-first-century-economist-by-kate-raworth.html

A good book

True. I’m not an economist, but I guess the trick is to match the amount of extra money to the amount of extra work that it’s buying. As we found in the 70s, it’s very easy for a government to print more money than the value of the additional work, with the effect that each pound buys less. One way to redistribute wealth, I suppose.

Since then, the explosion of personal credit must complicate the analysis. Does this actually remove money from the system, as the loan sharks squirrel away far more than they loan?

Over to people who know what they’re talking about…

You might try my book The Jiy of Tax

Will, the inflation of the 1970’s wasn’t a money supply issue in itself it was largely cost-push inflation due to the 1973 quadrupling of oil prices after the Arab Israeli war.

Later, unemployment was used as a price control and reached 1 million under Callaghan and then 3 million by 1982.

I totally agree with you as you are not the only person saying this. And that is important because it makes you less of an outlier and more of a potential new mainstream in the waiting.

Corbyn and his party now need to engage their killer instincts and take full advantage of this in my view. They must contend that there is a magical money tree.

As you mention, the police did not stop, the NHS did not collapse, the trains still ran on the fat government grants to the TOCs when we pumped in over £300 billion into the private banking sector.

Apparently the Tories main pollster has been laughing at the YouGov predictions about a hung parliament. The Tories are not stupid when it comes to gaining and retaining power so I’m sure that there is some substance to the Tories getting in again. But we shall see.

I’m sure you know that Monopoly had its origins in the Landlords Game, invented by Lizze Magee to demonstrate how LVT would improve the economy. There were two sets of rules: one where the landowner, either by luck or cunning, ends up owning everything and one where land values are shared and everyone benefits.

I do

What a lot of people don’t seem to realise is that the game Monopoly was designed as a warning!

It’s definitely not a successful economic model to aspire to, at least as the rules are currently set.

In an ideal world, you would receive your £200 on passing go (which represents your wages for all that dice throwing and trundling around the board, not a UBI), and NOT be allowed to buy properties, utilities or stations.

The rent you would pay when you landed on a property would be the un-improved rent for the site you landed on; the same for utilities and stations. You would pay Income Tax, and receive the occasional windfall or fine from Chance and Community Chest, as normal.

As such, the game would carry on for ever; no-one would get rich, but no-one would be bankrupted.

It would be the most boring board game ever invented!!!

But as a way to run an economy, it would be absolutely the way to go.

‘Does Money Make You Mean?’ is a somewhat-related talk which uses Monopoly to illustrate its key message:

https://www.youtube.com/watch?v=bJ8Kq1wucsk

Dare I suggest that Amber Rudd just doesn’t have a Cluedo. (Sorry!)

Bad!

I find the process of trying to understand macroeconomics both fascinating and frustrating, as one layer of understanding forever dissatisfies and demands a deeper understanding as I try to model the key processes.

If government can create all the money it wants AND commercial banks can create as much money as credit as there is demand at acceptable risk, the two sources of money are at the same time complementary and in competition. The appropriate points of taxation are where the money from government spending accrues as profits, capital gains, high incomes as well as on transactions. Taxation then restricts the access of banks to both assets as security and income for loan repayments. However, inevitably increases in government spending increase the opportunities for expanding private debt, giving rise to the risk of inflation as too much money enters the economy. Government then has the choice to raise interest rates, but this then constricts the multiplier effects of its own spending and encourages short term perspectives. The alternative is to use regulation to restrict credit, but that risks distortions in market values as much as excess secured lending pushes up the value of assets.

If this understanding is correct, we are caught between two unsatisfactory propositions: state management of the economy, or the state handing substantial power to financial institutions who only are really responsible for their own profit and power. Achieving the Goldilocks balance between the two is extremely difficult (and only recognisable with hindsight).

Yourself and others advance the idea that the state can justify assuming significant power, provided that it advances a clarity of mission that has the authority of being recognised as the appropriate mission. However, just as we see that an economy dominated by finance feeds inequality and social and environmental abuse, state power has a reputation for creating bloated institutions and politicised industrial relations. For economic policy to be coherent, purposeful and capacity building, a framework is needed that reduces the conflict of interest between the state and commercial finance, such that the two are working together.

Banks are licenced

They must be allowed to create money: that is their role

BUT that can be constrained by they terms of the licence they operate under

There is only one currency at the end of the day and only one money

And all is created by state licence at the end of the day

There is no conflict unless the state fails as a regulator of the banks

But I stress, banks still have to actually do the creation oif the money

Richard could you clarify why, in your opinion, banks have to do the actual creation of money through loans? After all, this is actually creating debt.

Why should we not cut out the parasitic middle man, and have money spent into the economy debt free by the Central Bank under elected and democratic controls, associated to national priorities and policies?

I see no reason not to have private banks lending at interest from existing deposits, but can’t understand why ALL money needs to be created as debt.

First, I accept banks can be oarasitic but I see no reason why they must be

Second, credit is real – and is what gives money value

Third, government unless you ban credit it will exist as money come what may

Fourth, how would chit with real value not be the real currency in your world?

And if you banned credit how would your economy work?

And who would know how much money would be needed – or would you call those who decided bankers?

Last, how does money that exists in perpetuity work? I have no idea

Clearly Hunt and Rudd want to win at Monopoly:

‘Millionaire Jeremy Hunt and the Climate Change Secretary Amber Rudd claimed 27p expenses for a 900-METRE journey’ ( Daily Mail 2016).

This seems right to me Richard and broadly in accord with (in fact the same as) what Stephanie Kelton says here – https://www.youtube.com/watch?v=Q1SMjeuyF-Y

But the bit I don’t get is why sovereign governments feel the need to borrow through bond sales etc in the first place. Why not just create and manage the money as a deficit? You’ve said previously that bonds make sense as a control mechanisms. Do you mean to say that the demand for bonds provides a market mechanism for money creation? Honestly, I don’t get it but my hunch is that Randall Wray gets it right (and I think Kelton says this too) that bond sales are about hitting interest rates but are basically unnecessary. That said, I’m at best a dilettante about this stuff so much of it is very murky to me. Here’s Wray on bond sales – https://www.youtube.com/watch?v=je-1eTl6J0g&t=12s

Try this

http://www.taxresearch.org.uk/Blog/2017/05/03/why-we-need-more-government-debt-2/

I must have missed something in my yoof as I played Escape From Colditz.

Amber Rudd and TressaMay’s husband are keen gardeners of the “magic money tree” – see reports in The Guardian of her links to Bahamas based tax haven businesses and his ‘asset management’ occupation.

People, There is just time for a quick education on the late Prof Elinor Ostrom’s Nobel winning work on ‘Management of the Commons’ in which she corrected Garrett Hardin’s 1968 essay ‘The Tragedy of the Commons’. There is at present a battle royal in play over these two concepts/philosophies. There are certainly many examples of Commons Tragedy – from the expansion of rentier class, the bonus culture, environmental chaos, species extinctions, the proposals to privatise the NHS (Naylor report) and Il Duce Trumpolini’s decision to remove USA from Paris climate agreement.

Attempts to put Ostrom’s philosophy into practice can be seen in many aspects of the EU – i.e. building institutions. Unfortunately, UK remains wedded to the enclosures consequent from one interpretation of Hardin’s analysis.

Agreed

Hi Richard,

As a layman I am concerned that creating more money could lead to monetary inflation. History lessons as a teenager of hyperinflation in the Weimar Republic spring to mind.

Would you or anyone else please be able to point me in the direction of some resources to read which might allay my fears?

Regards,

Harry

Weimar collapsed because a) it had to pay debt in other country’s currencies and b) it’s productive capacity was taken from it so could not earn that currency

The reality of the economy collapsed as a result. We are not in that scenario

What is more, you ignore the fact that all bank lending creates new money – are you worrying about that?

What you need to do is look at the reality. If we have under employment we can create new money to get resources to work until we have full employment. The we must stop. That’s when inflation happens

So, we can make money, but I never said without limits

Love this article Richard – so easy for people to understand. I have reposted to Facebook. I think it is amazing that Corbyn has got this far to get ideas passed with certain old labour MPs. If and I pray Labour does get into power people like you need to encourage and support so that the ideas are taken even further as discussed.Positive press would be a start, but lets face it the media is owned by those that don’t want this change

You forget I have no influence at all, or negative impact, these days in Labour

This has just arrived via email. While it’s better than nothing, a UK version would be helpful: The Basics of Modern Money – https://www.youtube.com/watch?v=TDL4c8fMODk.

I do not buy the difference between credit and currency: banks create money under government licence

Nor do I – but maybe it was a poorly directed attempt to simplify the message for an audience with no previous understanding. It doesn’t sound like an explanation that Randall Wray would subscribe to. But I’m not an economist (as you know!).

I wouldn’t recommend it

So back in the 70’s we didnt really need the IMF bailout after all?

It’s now well known that the situation was not as bad as was believed at that time so quite probably not

Of course we didn’t need the IMF!!

Why on earth would the monopoly issuer of the currency need to borrow back its own currency?

The ‘overdraft’ facility at the IMF was never actually used; but that didn’t stop Denis Healey and James Callaghan reducing public spending more in 1976 than at any time since, and thereby paved the way for the Winter of Discontent, 11 years of Thatcher, and 18 years of Tory government.

Idiots.

Not only was it not as bad but Callaghan completely mismanaged the crisis and unwittingly (?) bought into the IMF’s Monetarist agenda. He has a lot to answer for. As you know, Bill Mitchell has written extensively on the topic (http://bilbo.economicoutlook.net/blog/?p=33825). If only we could re-write history!

“A banker who plays in the game must keep his/her personal funds separate from those of the Bank”.

Oh, the irony with the revolving door, ever increasing public spending, etc.

I mean, at what point do we say “don’t mention the game”

Richard,

After watching yet another unchecked uttering of the word ‘magic money tree’ can you please go on air and give these morons (our PM) some basic economics lessons.

All I can do is write it

Invitations to go in air are not under my control

[…] http://www.taxresearch.org.uk/Blog/2017/06/01/monopoly-has-a-magic-money-tree-just-like-the-real-wor… […]

A very timely blog article Richard. Thanks. Theresa May repeated the “money tree” mantra last night.

A question for you:

Couldn’t the Bank of England create all the money (cash and credit) in our economy?

The Positive Money organisation suggests such a system is possible and would result in us paying less tax and not having to bail out private banks each time they bankrupt the economy.

In other words, I don’t see why private banks, “must” be the ones to create virtually all the money in our economy, which seems a little like putting the fox in charge of the chicken coup.

I too agree that Monopoly is a little like real life with regard to the banker’s role if not so much the rest of the game. I wrote about it here: http://m.huffpost.com/uk/entry/15082784

The Bank of England does create all money in our economy – you can’t create it unless the BoE lets you do so

But the PM idea that there is a stock of money is absurd. All money is debt. And it takes two to make a debt. PM has not realised that

So banks must create money by lending. There is no other way of making money

But there is no reason why banks could not be much better regulated and the abuse of this right be turned to social advantage

That is the right direction of travel. PM have just got this one wrong and it’s deeply unfortunate that they have done so

Richard,

Is it not true that rentiers have a “magic money tree” as well, since they can rent (or “tax”) the rest of us if we need what they “own” – land, property, intellectual property etc?

I do not think rents and money creation can be confused

Money creation can be benign

Rents almost never are

Richard,

Firstly, great blog and very interesting. I don’t have a background in economics or business but I developed an interest recently, mainly due to the upcoming election. From what I have researched so far,labour over the last few years have allowed themselves to fall for this myth that is ‘balancing the books’,or ‘eliminating the deficit’. Even a prominent labour MP, Chuka Umanna, embarked on a apology tour, arguing that labour main problem was economic credibility

https://www.theguardian.com/commentisfree/2015/jun/29/labour-tory-lite-economic-credibility-leadership

I have never understood this austerity fever and how the British public have allowed themselves to buy into this deficit game. Having read this piece by Paul krugman, I now know why the election has gone the way it has.

My question to you,is what happens after a Tory government eliminates the deficit? Assuming this is possible,considering that they have been unable to do so thus far. Will the British people be expecting some kind of reward in public spending, to make up for more than a decade of austerity, cuts ,cuts cuts. A more democratic and efficient media would have investigated the actual reason why reducing the deficit is the most important task.

There would be no reward

There could only be a punishment because a government running a surplus is continually shrinking the economy by taking demand out of it

There may also be a credit crisis: there would be insufficient money to meet demand

And a pensions crisis since government debt underpins private pensions

But I wouldn’t worry: the chance it will happen is remote