Two illustrations of the fact that tax competition does not work have come to my attention this week. The first arose in evidence given by Chris Sanger of Ernst & Young to the House of Lords on Monday earlier in the session during which I also gave evidence. He said that in his firm's experience tax was the sixth or seventh most important consideration in decisions made by companies on international location. I do need to get one to five from him.

More important is a new paper by Tidiane Kinda for the IMF, the abstract of which says:

Using manufacturing and services firm-level data for 30 sub-Saharan African (SSA) countries, this paper shows that taxation is not a significant driver for the location of foreign firms in SSA, while other investment climate factors, such as infrastructure, human capital, and institutions, are. By analyzing disaggregate FDI data, the paper establishes that, while there is considerable contrast in behavior between vertical FDI (foreign firms producing for export) and horizontal FDI (foreign firms producing for local markets), taxation is not a key determinant for either type of FDI. Horizontal FDI is attracted to areas with higher trade regulations, highlighting interest in protected markets. Furthermore, horizontal FDI is affected more by financing and human capital constraints, and less by infrastructure and institutional constraints, than is vertical FDI.

In other words, tax competition does not work.

Despite that though the Coalition has set out to engage in tax competition to attract new business. It has said:

Since 2010, the Government has undertaken a comprehensive review of the UK tax system, consulting with business on the direction and design of our reforms. We have made tax policy simpler, more transparent and therefore better suited to a globalised trading world and to modern business practice. We believe that the corporate tax system can and should be an asset for the UK, improving the business environment and helping to attract multinational companies and investment.

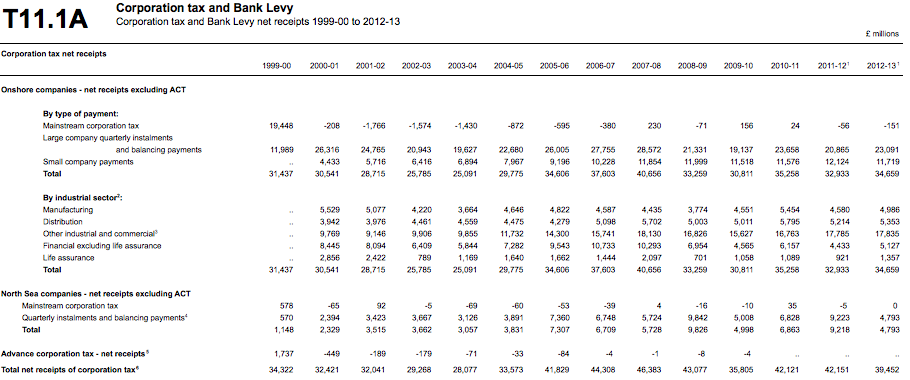

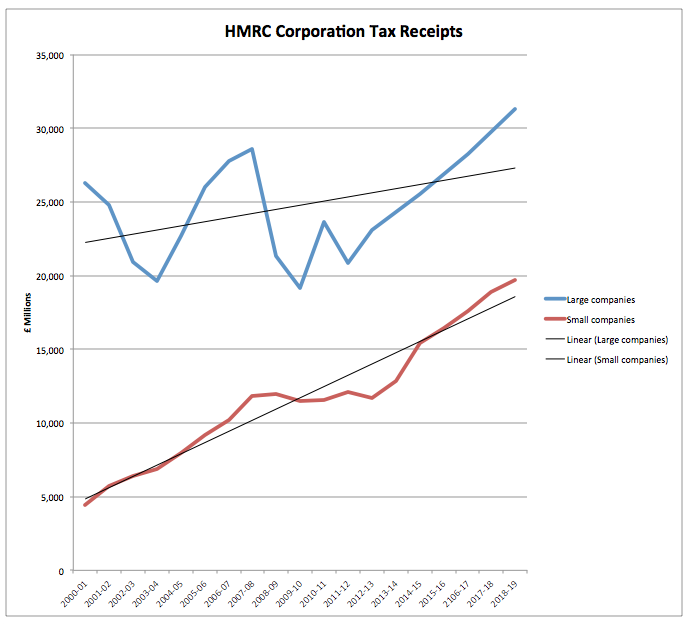

The cost has been phenomenal. UK corporation tax receipts for the last decade or so have been as follows (source HMRC) (click image for a bigger version):

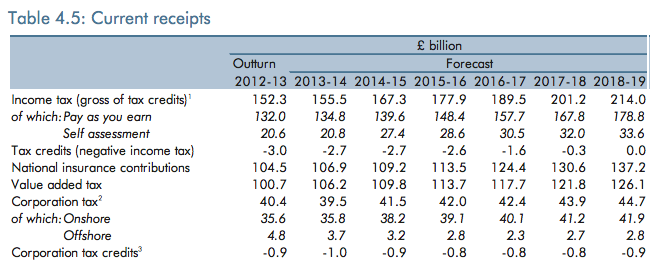

Forecast revenues based on OBR data are:

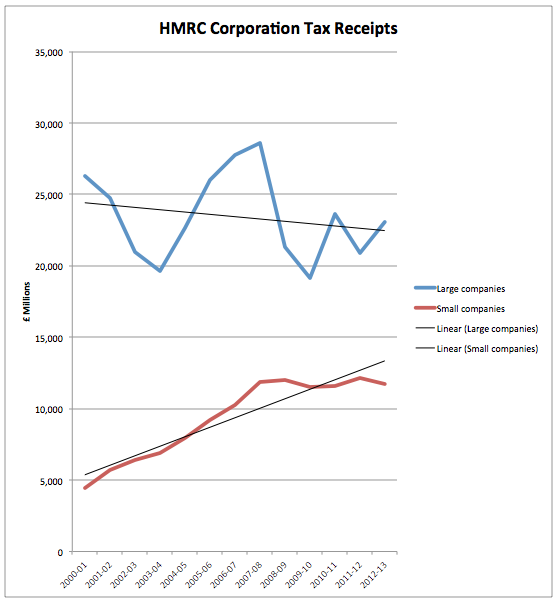

I thought it worth plotting the actual data to give an indication of trends:

Give or take large company tax take has fallen on average by £150 million a year over 12 years, admittedly with wild oscillations but with recent behaviour when it is known that profits have been rising confirming the trend. In contrast small company revenues have risen, admittedly partly because there are simply more of them.

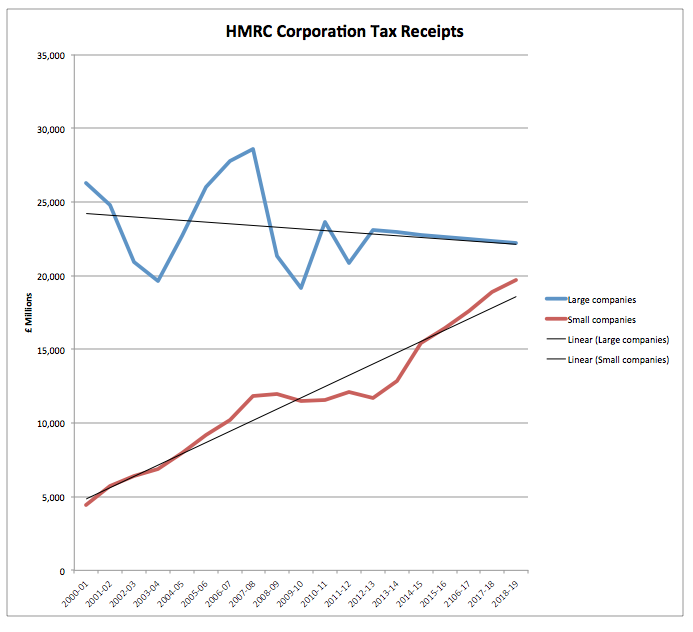

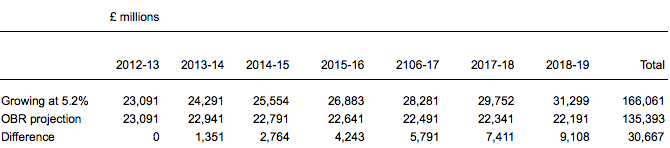

I then remodelled the data to 2017-18 using this trend data:

Thius projection forms the base line for comparisons noted below on tax lost from big business. Now, of course, this is extrapolation but the point is very clear: the contribution that big business is going to make to the UK over the next few years is going to fall considerably, and smaller business is going to contribute more. I have little doubt at all that this is true. Indeed, it is confirmed by the FT this morning, who say, triumphantly (given that PWC are behind the story), that:

Britain's biggest companies paid more in national insurance contributions than corporation tax for the first time last year, marking a drop in profits and a historic shift in the way companies are taxed.

A decline in profits from North Sea companies was the biggest factor driving down the corporation tax paid by The 100 Group of the largest UK businesses, which fell by a quarter to £6bn in 2013.

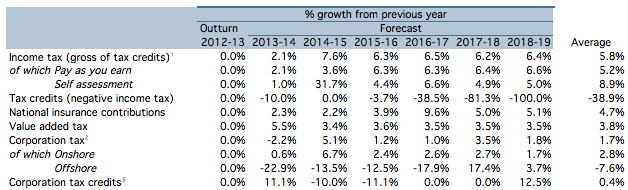

So what might this policy of tax cutting, promoted because it is believed that it will induce tax competition that will in turn bring business to the UK despite the fact that evidence shows that this does not happen, cost us? To work this out I looked at the OBR forecasts for tax revenues until 2018-19 and expressed these in percentage growth terms, as follows:

The average is for 2013-14 onwards. The figure for self assessment looks to be wrong in 2014-15 unless there is a massive tax hike coming so far not announced or the OBR believes that business is going to see the most enormous hike in profits. The overall figures actually look absurdly high as well: tax take is planned to increase considerably faster than growth over this whole period which may come as news to all those who think the government is committed to tax cuts However, for the current purpose I am assuming the OBR know what they are doing and it seems fair in that case to assume a growth rate that is based on broad economic activity and since 5.2% would broadly average income tax, PAYE and NIC that is the rate of anticipated tax growth I have used in the first instance.

Using this rate I have then estimated the growth rate for small business corporation tax contributions and averaged them over 2013-14 to 2018-19. That average is 9.1%, remarkably similar to the self assessment growth rate and oddly the peak is also in 2014-15, where again there is a weirdly high growth rate. I have no idea what the OBR think is going to happen to small business profits next year. The important point is that there is data consistency, and there is.

Then I have applied the 5.2% growth rate to big company corporation tax receipts, making the reasonable assumption that without policy interference they would rise like other taxes. The resulting graph of projected revenues would then look like this:

Expressed in terms of tax lost the data is as follows:

What this means is that over a period of six years more than £30 billion is to be given away to big business to supposedly lure new business activity to the UK when there is no evidence that such a policy works.

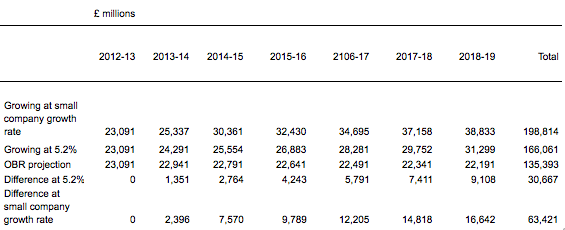

This, though, did not seem like the best answer to the question of what this policy might cost. We know that profits are cyclical, and we can see from anticipated self assessment receipts and implicit small company corporation tax receipts that significant additional tax revenues are anticipated in 2014-15 as a result of what must be anticipated profit growth. It would be very odd if the same rate of profit growth was not anticipated for large business, so I then used the rate of projection implicit in the OBE figures for smaller companies and applied it to the large company tax paid data and the following resulted:

Now the total cost of the policy is shown to be as high as £63 billion over six years.

In that case it is likely, on reasonable bases of estimation, that an average of between £5 billion and £10 billion a year is to be lost from tax revenues because of a dogmatic experiment with a policy that EY says has little impact on decision making and which hard evidence shows is largely irrelevant to business location decisions. But the loss is real nonetheless: those many billions will be lost come what may and all because of misplaced policy. As the FT, again, note today:

The figures were hailed by PwC, the professional services firm that compiled them, as a sign of a global trend away from taxing profits as governments have tried to stimulate investment and achieve a more stable tax base.

Kevin Nicholson, head of tax at PwC, said: “It's not a surprise that for the first time corporation tax is not the largest tax paid by the UK's bigger employers. Looking at the full picture of tax paid by business, you see that tax on profits has fallen while taxes on labour and property have increased. This is a global trend.”

But if this is a global trend (and I think it fair to say there is evidence of that) then it is because people like EY and PWC promote it, even though there is no evidence base for it. In that case it is fair to conclude that the policy is instead intended to promote a simple shift in tax onto labour; there's no evidence of it falling on property.

And yet at the same time the bosses of these firms receiving these windfall tax cuts - most of which will help trigger massive executive share bonuses - are also protesting about the 50p tax rate and are sitting on enormous piles of cash that they have no clue what to do with.

If someone wants to know where some real contributions to the cost of cutting the deficit can be found they could start with large company corporation tax. A rate cut of 7%, the introduction of territorial taxation, the effective ending of the controlled foreign companies rule, the introduction of the patent box and the offshore treasury arrangements have all been designed to give business a tax bonanza and it is going to pay out handsomely at cost to the rest to us. When that cost could be an average of more than £10 billion a year over the next six years no one can ignore this issue.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Firstly, what has sub-saharan Africa with it’s closed markets and lck of developed infrastructure got to do with Western free markets?

Secondly, you make a huge ommission. The trend of the tax reciepts isn’t solely due to the tax rate – the massive dip post 2008 is due to the recession. This means that any further extrapoation, without normalising for this, is totally meaningless.

First, EY confirmed that the African trend is found here

Second, other studies do as well

Third, the OBR data allows for recession – and I have done so by default as well

All your suggestions are therefore wrong

OBR data doesn’t “allow” for recession, it jsut gives nominal tax reciepts.

You have also clearly ommitted the 1999-2000 number for large companies, I assume to fudge the data to give you the downward sloping curve your argument rests on. If yoou go back to 1965, the slope of the curve looks very different – upward sloping.

If I went back to 1965 I would inflation adjust – of course it is upward without that adjustment

I omitted 1999-2000 because there was no small company data

If the African trend works here, why has Fiat just set up its new filing cabinet head office in the UK?

Note reply to Tyler

And by ommitting 1999-2000 you have managed to create a downward sloping curve. Simply by adding that point in, it becomes upward sloping, invalidating your whole argument.

If that’s the case I never tested it

I ignored data for which there was no comparison – an entirely statistically valid reason

But let’s also be clear – I have been generous. PWCD say the fall in big business tax payment last year was 25%. I ignored that and assumed past gradual declines would continue. I have actually been extraordinarily generous in ignoring falling tax rates and changes in systems in suggesting likely change

I therefore almost certainly understate my case

Also:

In this article you are basically arguing that companies don’t locate or relocate for tax reasons.

However, in the other article you posted today about Fiat/Chrsyler, you are saying they do.

Which is it to be?

Fiat Chrysler is a notional location

The article is about the real centre of economic activity

They are now unrelated

Tax moves notional locations but not real economic activity

FIAT itself has factories all over the world, including Italy, Serbia, Poland, Brazil, Argentina, China, Turkey and France. Chrysler has even more locations around the world. Both companies have sales all over the world as well.

How can you say their economic activity is based in a certain place?

The move to a Netherlands base has a very simple reason behind it. The Netherlands has double taxation treaties in place with almost every country in the world. It’s not about avoiding paying tax, it’s about avoiding paying it twice.

You have just said their activity is based in certain places

More interestingly, where is this ‘nowhere’ where you are suggesting economic activity occurs? And who lives there?

And as for the Netherlands and double tax treaties – as the OECD now says – measures to avoid double tax now usually result in double non-tax

That’s not me saying that – it is the OECD

Shall we therefore deal in facts – not your fiction?

“You have just said their activity is based in certain places More interestingly, where is this ‘nowhere’ where you are suggesting economic activity occurs? And who lives there?”

What on earth are you talking about. These companies maufacture in certain locations, but do business all over the world. You seem to make the assumption that there is some singular “real centre of economic activity” which for global corporations is utter nonsense – it’s globally diversified.

They still have to have an HQ though, and it is entirely up to that company as to where it is. The Netherlands is common because of their dual taxation treaties, which means that a company doesn’t get taxed twice on the same profits – which avoids some otherwise ridiculous situations. For example, Apple being unable to repatriate non-US profits back to the US. Are you suggesting a company should be taxed twice on the same profits?

You seem to have this fixation on taxation where the economic activity occurs, as if each company acts within the borders of a country in isolation, and each economy is essentially a closed one – driving your country by country reporting meme, which treats a company’s presence in a country as if it were an individual, stand-alone entity.

The problem is the world, thanks to globalisation simply doesn’t operate that way. A company’s labour, production, sales and profits are not distributed on the basis of borders. CbC ignores this, and will lead to the same problems transfer pricing tries to deal with, where costs of manufacture show up in one location (so a loss) but all the sales revenues show up elsewhere as massive profits, yet the net profit is all that can rightfully be taxed.

You have not answered the question

Of course I have a fixation on “taxation where the economic activity occurs” because I think that has to be somewhere

Are you denying that?

If so, why, and with what evidence?

Oh, and that fixation with a “treating a company’s presence in a country as if it were an individual, stand-alone entity” – maybe you don’t know that’s how all the big accountants, lawyers and MNCs say things are for tax. Are they wrong?

Please tell

The small company tax hike in 2014/15 will be due, in my estimation, to the disproportionate effect of the reduction of AIA on small companies. Companies taking advantage of AIA at more recent generous levels have built up significant deferred tax liabilities which will begin to be released in 2014/15.Also new investment above£25K will attract only 18% or 8% allowances, significantly below rates of accounts depreciation on the same assets. All predictable.

Hang on – deferred tax has no implication for actual yield in the way you predict, at all

It’s all accounting

http://www.telegraph.co.uk/finance/newsbysector/banksandfinance/10472446/EY-Cutting-UK-tax-draws-in-more-multinationals.html

From the above article, he explains that they are moving into the UK over the next 12 months.

How many companies will decide to move after the outburst from Labour this week is another matter, however. Which is very sad.

And as I have explained, they are only moving their filing cabinets in

Yep. Fiat are only avoiding tax elsewhere.

Meanwhile, Germany seems to have slipped somewhat….Cypriots are better-off than Germans!

http://www.testosteronepit.com/home/2013/4/9/total-fiasco-germans-are-the-poorest-cypriots-the-second-ric.html

The problem here is not with the large company figures so much as the small. Richard, I agree that the 2014/15 self assessment growth rate in the OBR figures looks decidedly odd, but your small co. CT one is easily explained – you’ve taken a trend that flatlined from about 2007 on, and assumed it will revert to the mean from 2000 in 2014/15.

The main reason for the astonishing rise in small company CT receipts from 2000 – 2007 is the massive but entirely predictable rise in incorporations of small businesses. This was triggered by the introduction of the 10% and then 0% rate on the first £10k of profits. Admittedly a 0% rate does not bring in a lot of tax… but most of the companies had higher overall profits than that, it just meant they paid at least £2k less tax on the business profits than when they were unincorporated. The increase stopped when Brown finally gave up on his obstinate insistence that the 0% rate was a good idea that could be rescued by the NCD rate.

Adjust the total small company tax paid for the increase in the number of companies and you might have a case; but at the moment that looks like the most obvious explanation.

I agree the number of small companies can explain the trend – and the removal of AIA may do as well

But if I am wrong on small companies big companies would have to pay more to make sense of the OBR data – which is all i am seeking to explain (lest anyone forget, that is not my number) but we know there is very good reason for big company tax to fall more than I have suggested and PWC is saying it is, in which case I have not over but underestimated small company tax due

I have therefore likely understated the cost of the big business subsidy – which is what all this was about

You have also ignored the recession Mike, not a minor side issue

I’m not sure I follow the point that if small companies’ bills increase less than you predicted big companies would have to pay more – is that direct from the OBR data on corporate tax, from your extrapolation of PAYE/NIC to tax growth, or your extrapolations for future years?

But in general I don’t disagree with your point; big companies are getting tax breaks in the shape of reduced rates and the CFC/patent box changes. Unlike you, however, I don’t see any reason to believe that tax competition isn’t real (though problematic). I can believe that in sub-Saharan Africa issues such as rule of law and infrastructure mean tax is not that relevant, I can even believe that tax is some way down the list for western countries, but since other things are often fairly equal in the west, tax competition surely plays a part.

Tax competition exists but is for the location of profit recording and not for the location of profit generation which are far from the same thing

So the UK has competed to record Fiat’s profit by cutting its tax rate and base

It has won that race but Fiat says no work will be shifted to the UK

The result is we gave way existing tax revenue to win no new revenue. Mo

PAYE, VAT etc will follow. We have just lost

So tax competition exists for the false recording of profits – hence BEPS – but as the evidence shows , does not change reality

However it does have a cost – business contributes much less to the UK as a result because cuts are given to business already here