I admit I get really bored of Tories talking about the government's debt.

Take this from new Tory MP Sajid Javid in the Telegraph a day or two ago:

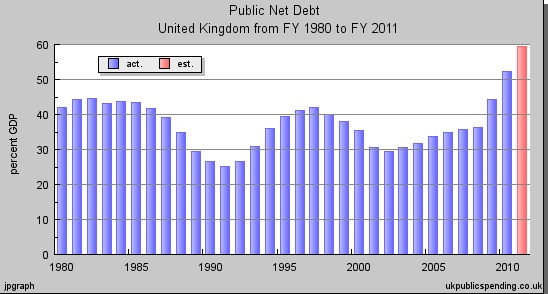

Over the past decade, our net public debt has rocketed from £312 billion to £920 billion (or from 31.5 per cent of GDP then to 60 per cent now). This happened because Labour chose the easy way out instead of trying to find solutions to the long-term challenges facing the public finances. It believed that the answer to every problem was to spend more money: so budgets and debt soared.

Now that's complete nonsense. This is what actually happened on debt excluding interventions in banks:

Source here, from ONS.

If we take 2001 to 2007 as the years for which labour was wholly responsible - i.e. after the Tory policies had washed out of the system and before the worldwide crash - then debt as a proportion of GDP was very obviously much lower as a proportion of GDP then during most of Thatcher's era and way better than much of Major's period in office.

Of course debt went up in 2008 and onwards - but unless Tories wanted the economy to have been destroyed, as I explained would have happened if Labour had not acted here today - then first Labour had to bail out the banks and second bear the costs of the crash which was the sole cause of the resultant increase in debt which was not and never could have been Labour's fault.

So what word describes most accurately the Tories' claim? Does 'lies' work for you? It does for me.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

You are ignoring PFI liabilities and unfunded public sector pensions, both of which should be included in any assessment of the public finances.

PFI debts are actually not that big – and they’re asset backed (you might recall)

As for pensions – what liabilities? Since cost is falling as % of GDP and they’re wholly affordable how come they’re unfunded?

Surely the big risk is the unfunded nature of private pensions – many of which will not pay

Does this include PFI?

Yep, that’s right, just ignore the cost of bailing out the banks. It was a one-off, after all. Just like the whole recession.

But it was not Labour’s fault

That was my point

You ignore the fact that from 2003/04 onwards all GDP growth was accounted for by increases in public spending and a massive accumulation of private debt, which Labour made no effort to stop and which eventually caused the baniking crash.

It would be incorrect to ignore the cost the banking rescue without taking into account the GDP “inflation” in the run-up to the crash. Once you adjust GDP in the 2004-08 perood for the portion that directly resulted from the unsustainable debt dynamcs (that is about 8%-10% of GDP), the analysis would look very different. .

D

Of course public spending increase, that is why borrowing rose to fund necessary investment. So what? Society needed that investment. I warmly welcome it.

And borrowing went up for quite different reasons. The 1st was the refusal of the market to pay decent wages. The 2nd was the massive advertising of credit by banks and other institutions, who created this problem. This was a supply led phenomena, not a demand led one.

As for your analysis of unsustainable debt dynamics, that’s just codswallop: it would be much worse under the Tories because they demanded a lot less regulation. Thankfully they were not in office.

Would sovereign debt default really be the end of the world, if everyone did it? If we all owe money to each other, why can’t we come to some sensible agreement to cancel or at least only pay an affordable percentage of it?

Sorry if that is a stupid question, only it is what I wish I could ask every time debt and deficit are talked about.

Thank you for writing with so much energy about unfairness.

The problem is it’s not easy to work out who owes what to whom – so the edifice all falls over whilst you’re doing that…

It’s not absloutely clear whether the bank bail out is represented in the graph – it says ‘excluding’ above the graph, but below it says ‘of course the debt went up in 2008 and after’, apparently in explanation of the rise that sets in then.

Much to thank Brown for, certainly (Euro, saving the world, etc). But he it was who systematically, openly, as policy, cheered them on, all the way over the cliff. And protected the City as tax-haven the Germans begged him to stop it.

The graph does not include bank debt – it includes debt caused by the crash more generally

I don’t excuse Brown – dammit, I criticised him – http://www.taxresearch.org.uk/Blog/2007/06/14/brown%E2%80%99s-decade-was-it-taxing/ – but the Tories would have been worse

That’s all I am saying

You say that the ‘Tories would have been worse’ but I seem to remember that they went into the 2001 and 2005 elections promising to reduce the expansion in expenditure if they won those elections …

That’s why they lost

The spending in 2001 and 2005 was affordable

That’s why they then promised to match Labour

They lost – but I suspect that the reasons are rather more complicated than you suggest.

As to the alleged affordability – profoundly, I disagree, and I would point to the current cicurmstances as evidence that the increased expenditure was not affordable.

That’s OK

Disagreement is part of life!

We’ll have to agree on that

I agree that what Sajid Javid said is unfair, but I’m not yet convinced that Labour can avoid all blame. Public debt as a proportion of GDP increased consistently from 2002 to 2007. It didn’t make huge jumps, but it was increasing, and ended up noticeably higher in 2007 than it had been in 2001. I’ll admit to not being an economist, but I would have thought that it makes sense when times are good to reduce the debt so that you’re in a stronger position when things inevitably go wrong. Maybe you should take on some extra debt so that you could spend more to boost growth, but then you still shouldn’t want debt to consistently grow as a proportion of GDP.

As I said, I’m not an expert. I could be missing something.

Sure it rose – and maybe in 2005 on it should not have done – I agree – but to say it was in any way out of control is just wrong – it remained modest by all standards in our history – whoch is why the Tories said they would match Labour spending plans until 2008

That’s their hypocrisy

When a right-winger forms an opinion on something, it very quickly transmogrifies into fact (albeit in their own heads.) This is why anybody who has the temerity to disagree with them is a ‘deficit-denier.’

That Tory MP has been inspired by the Tea Party in the US. There is a fixation by the Right about debt to the exclusion of almost everything else. Most people who own a house have acquired it by means of debt (a mortgage). There are of course challenges to the public finances which need to be addressed but to simply state that the nation is ‘maxed out on its credit card’ as a reason for not investing for the future will serve to damage our nation. Asian economies pursue the ‘developmental state’ model and that explains to a large extent their growth patterns. They recognise that the state has an important role to play in economic development and that the market alone will not stimulate growth. Unfortunately neoliberalism downgrades the role of the state and relies on the pre-eminence of the market. Osborne’s reliance on the latter is proving to be a disaster.

“As for your analysis of unsustainable debt dynamics, that’s just codswallop”

Actually I think what Darren wrote is pretty accurate. What I understand him to be saying is that the vast majority of GDP “growth” between 2001 and 2007 was actually fictitious but caused by unsustainable increases in the level of debt. How can one disagree with that?

Quite easily

Someone actually made that stuff

But it was made by increasing debt. And that was unsustainable.

Yes

But you fail to analyse why

It was not gov’t debt that was the problem – it was private debt

Would I be right in thinking that the level of debt (as % of GDP) which Labour had risen to before the financial crisis was still lower than the level they inherited from the Tories in 1997? And that the rise preceding that was at a sharper rate than under Gordon Brown?

Any reasons or explanations for this?

You are right in thinking both things

The answer is simple: Brown was an economic manager with an objective of achieving social goals for which he thought it was worth borrowing but he managed that borrowing a lot better than the Tories ever did

This is what I find worrying; that in an educated society Conservatives can get away with saying “Brown’s spending was irresponsible” when they agreed to match it at the time, and that the level of debt (pre-crisis) was unmanageable, when it was lower than their last incarnations left it.

Why do the journalists taking such quotes not laugh at them?

The problem is that if you compare chalk with cheese you end up with a disputable conclusion –

When we entered the recession in the early 90’s, the debt to GDP ratio wasconsiderable lower (about 26% or so) than it was when we entered this latest recession (about 40%). In my view, a responsible Government will pay down debt in the good times, and on this Labour did OK between 97 and 01 – but the problem is what they did after 01.

There was a recession elsewhere in the world in 2000 to 01, which was avoided in the UK by a combination of changing the basis of calculation for inflation thus feeding an asset price bubble and by increasing the ratio of Government expenditure (which produced a short term and unsustatinable increase in GDP). That the Government was also spending more than it received by way of revenues and that some of the revenues themselves were inflated by the asset price bubble only exacerbated the self-deception – what was it about ‘abolishing boom and bust’?

But then, we disagree – partly out of education, partly out of experience and partly out of what we feel comfortable with. I can cite nobel winning economists too, but the difficulty is that, to misquote your favourite, Keynes, to change your mind when the circumstances change is entirely to be expected. The old joke about the opinions of economists comes to mind …

Look – please get facts right

About 30% and 35% – you wildly mis-state things

If you want to be taken seriously that does not help

Sorry, I don’t think that I am – I was writing from memory – which is always a dangerous think to do, but since this is not work, I though that using remembered information would not matter much –

But if you look at the HM Treasury databank – tab A6, Public Debt (% GDP)- and the figures for Public Sector net debt – 1990-91 (the recession was in 1991-1992) reveals 26% and 2007-2008 (the recession was in 2008-2009)-2010) – 36.5% – the gross debt figures were 32.9% and 43.6% respectively. I appeared to be remembering the net debt position – and misremembered the latter figure. But then, if I remember rightly, the recession struck in the latter half of the 2008-2009 tax year, whereas the recession in the early 90’s struck the UK earlier in the 1991-1992 tax year – I haven’t checked this, so I suppose it is entirely possible I am mistaken.

The fact that I appear to have overstated the net debt positon in 2007-2008 by 3.5% is an error that I am happy to admit – but given that these are estimates, and given the narrative of what I have written, I don’t think that that particular error matters too much, especially given that I used the word ‘about’ because I was using remembered information in a blog discussion …

Evan

Debt to GDP at 26% (1991) v debt at 38% (2007-8) isn’t much of a difference really.

Getting wildly hysterical over the debt to GDP in 2007-8 is barking up the wrong tree.

The UK’s economic problems were – sorry, are – deep rooted and stem from a lack of investment, emphasis on low skills and gluttony for short term returns. Think about how the media and politicians were hailing all those bank profits from mid 1990s onwards. The provisions we see being set up today are the wholesale write down of those activities. In other words, even the post de-regulation “success” in financial services industry, so long held up as the UK’s success story, were a mirage.

That is partly a failure of politicians, but the Tories certainly don’t get off scott free from any blame – they set the whole pyramid scheme up in the first place, and their press watchdogs howl every time a government dares to bring closer control and scrutiny over this tottering structure.

It is also a damning failure of the private sector and its acolytes – which is exposed now as not really knowing what is good for it. More deregulation and low taxes has just bred mass market volatility and flagging demand for its goods and services.

When will we learn? The best markets are ones where government takes an active role, backed and checked by democratic accountability. Free market libertarian lunacy is just that: a barking mad theory which undermines the vested interests it purports to represent, with no grounding of its theories in the real world.

I am not hysterical about debt at all – the difference between 26% and 38% is a little over 10% – and when that represents about 1/3 of the total debt, I am not sure that it is insignificant.

I was responding to the points made with points of my own – showing, I hope, that it is not as simple as one side being right and one wrong – and the right may not be right, although I happen to find some of their arguments more persuasive. The problem with economic argument is that it is impossible to know who is in fact right and who wrong, it is merely a matter of argument and who persuades you.

The ‘Big Bang’ in the mid 80’s was, in my view, a significant success. In the Chancery Bar we warned the Government away from the structures establised by the FSMA in 2000 and its purposive regulatory system. Two of the problems were that were specifically identified were, in my view, significant – one the loss of specific knowledge of individual regulators with the creation of the FSA – and two that unless there was certainty in the law, the relative power and ability of individual players in the markets would be significant – I happened to be present listening to a discussion in 2000 before the act came into force and listened and participated in the discussion with the first proposed head of the FSA who dismissed both of these concerns as they needed to be able to react to changed circumstances, thus justifying both of the propositions that concerned the lawyers.

From experience after the FSMA came into force, I found that there was only an appetite to ‘go for’ the small players – who were stopped from doing things the bigger players were participating in – and to this extent, there was a failure of certainty in the law and a failure of regulation. The result was that the systemic risks being undertaken by the largest players were not being effectively regulated at all.

The original 80’s deregulation led to massive real investment in businesses up and down the country and elsewhere – the growth in captial investment in private markets between 85 and 2000 was very significant indeed. It acheived a level of certainty and survived 2 booms and 2 recessions – the FSMA failed at the first recession (although it has to be said that the recession was more significant in scope); but to some extent it was the failure of the regulatory regime to achieve certainty and to regulate the bigger players that played a part in that recession too.

We all want there to be longer term private investment in the UK – it has been the holy grail of Government policy in industry almost since the establishment of the Board of Trade – which was a very long time ago indeed. The regulatory models of the 1970’s had their advantages; but they stifled both ingenuity and investment.

Markets have always been and will always be regulated. Think about the City and the great Companies and the manner in which they managed their monopolies – then the revolution which led to those monopoloes being broken up and the subsequent revolutions in the establishment of banking, the creation of controls on monopolies, the evolution of the joint stock company and the limited liability of companies, and the evolution of what we now call financial markets – finally the development of markets in derivatives and other purely fincial products. All of these have been and will be regulated. That different parties place difference emphasis on different aspects of that regulation – some preferring to let the markets freer than others, does not mean that anyone sensible proposes the wholesale abandonment of regulation. Certainly, that is not the view of any of the Conservative politicians that I know – and given that I have almost become one of their number, I know rather a lot of them – save for a few whose real influence is limited. Indeed, if you talk to the people who participate in the markets themselves, they do not object to regulation; what they oppose is regulation that is ineffective, that creates uncertainty, that fails to regulate the whole market including all of its players, or that fails to protect individuals consumers (especially) adequately.

Having written that, no regulatory regime will do all of these things all of the time. So we have to strike a balance between the regulatory regime and the risks we are prepared to accept. In my view, the FSMA crossed that boundary and the FSA’s subsequent failure to assess/understand the risks and in particular the systemic risks assocated with the enormous growth in the markets for what are in effect bundled debt and other obligations – in London this grew from a few hundred million in about 2003/4 to many tens of billlions in 2007/8.

Sadly, in the global world we live in, and the increasingly complicated lives we lead, I don’t believe that we can simply say, ‘time to get off and walk the earth untroubled by such complications’. Perdiocally, throughout history, there have been troubling times – and despite these we have seen our lives improve throughout that period of time. We have responsibilities too. But the wholly managed ecomony is, in my view, considerably less capable of delivering prosperity to all, than the partially managed economy that we live in today.

Sorry to be so long winded, and there may well be ideas in this entry that I will need to expand upon and develop to deliver clarity – but this is what my real world experience causes me to consider relevant to respond to your post.

All I can say is read my forthcoming book – The Courageous State

To say our world views differ is an understatement

But your glibness in blaming regulation is astonishing – that was part of the whole neoliberal conceit you applaud

And was the adoption of neoliberal economics – with its view that there was no such thing as uncertainty

Only Keynes’ and his understanding of maths – including the fact that we can just not know so that gov’t has to exercise judgement – can get us out of this

The tories don’t seem to mind certain types of debt. They don’t mind the £8 billion of tax relief given to the rich, which woulf be fair enough if it was in condition of investing in the economy, but it isn’t. Plus, correct me if I’m wrong, but haven’t they given away £24 billion in coporation tax cuts? They also don’t seem bothered by the billions of pounds that goes towards subsidising private pensions, or indeed the £100 billion plus that will be spent on the Trident replacement.

Of course, they intend to build eight new nuclear power stations, in which most of the cost will inevitably fall onto the taxpayer.

And there is the debt of £15 billion a year plus that they’d rather spend to keep people on the dole rather than spending the equivalent to get people back into work.

This country is not broke. The national debt is actually not that big. It is now cheaper than it ever has been for the government to lend money.

The items I have quoted here add up to £174 billion. Even a quarter of that would provide over £36 billion of investment. Never let the tories away with the excuse that they cannot afford something. When the political will is there, they clearly can!