I posted this on Twitter about an hour ago:

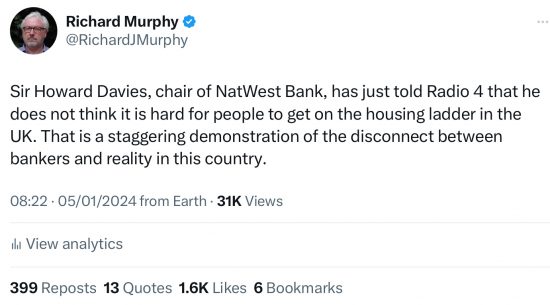

I admit I was not alone in noticing this, or posting it on X (as it likes to call itself), but it seems that this comment is getting a lot of attention, and appropriately so.

A man so out of touch with reality deserves no role in a bank boardroom, or public life.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

In his autobiography, Dr John Marks writes about his house purchase in 1956 (£4,500 at 3.5% fixed for 30 years):

“We offered him our maximum, the princely sum of £4,500, which he accepted. At the time the nation was in the middle of one of its recurrent credit squeezes

and raising money was very difficult indeed, but the Scottish Equitable Insurance Society offered me an endowment mortgage. It was to be a policy without profits and the interest was fixed at 3.5 per cent, payable for 30 years. We accepted, although we were told that we were stupid. Years later, as a result of inflation and high interest rates, we would still be paying £350 a year on our mortgage — a pittance — while others were paying more than that monthly for much smaller houses.” — The NHS: Beginning, Middle and End? The autobiography of Dr John Marks (2008)

Even in 1983, 3 times the average salary would buy the average house. In 2023, 8½ times the average salary buys the average house.

Worse, average house prices have more than doubled in value (not price). https://www.avtrinity.com/news/house-prices-vs-income-how-affordable-are-uk-homes

See my comment elsewhere in buying a flat in 1983

I bought my first house in 1986 for £46,000, a 3-bed maisonette on 3½ times salary.

I remember the estate agent not telling me until I had agreed, that they would want a £1,000 deposit, increased a week later to £2,000 (still under 5% of the house cost, but I wasn’t impressed with them springing it on me). I wish I could remember the terms, but it was something like 5% fixed for two years.

It was also an endowment, and I recall a letter at some point explaining that the bank’s investment was not likely to pay off the original term, at which point I decided that bank’s were a bunch of crooks, as this arrangement would not have been allowed if my payments fell short.

My deposit was £250 in 1983.

I also used an endowment policy – which I ditched in 1987 fur mortgage purposes, moving to repayment, but kept. It paid out less than half the 1983 predicted value.

I bought my house (smallish 3-bed detached with garage and gardens) not far off 22 years ago. I was a SINK (Single Income No Kids), had a reasonable deposit saved up and could easily afford the repayments whilst still doing pretty much whatever I wanted to do in my social life. This on an income not much above the national average, although I admittedly do live in an impoverished northern town where prices were low. The value of the house has probably trebled since then.

Around 5 years ago, my sister-in-law and her husband bought their first house near Norwich. Both were teachers working full-time at a private school. However, they initially weren’t able to get a mortgage, because my sister-in-law was employed on a rolling short-term contract basis and the school wouldn’t offer her a permanent job at the time. To cut a long story short, the only way they could get a mortgage, was for her to stop teaching and take a full-time job at the same school as a teaching assistant at a much lower, but guaranteed salary! Absolute idiocy, and things have only become worse since then.

Sir Howard probably thinks this shows the system is working!

The average earnings for an industrial worker in 1955 were £10 17s 5d, which is about £130 a year.

130 is around the average annual wage for that year, which means the house in question cost a multiple of 34 times the average wage. 34 times the average wage right now would be £1,292,000.

I don’t think this example is demonstrating that houses were more affordable in the past. The house you have used an example certainly wasn’t.

The average house price in 1955 was about five times average wage

You ignore the fact that average wage was aberage household income – most women did not work

You also ignore the massive availability of social housing

YTour figures make no sense. Average pay was arounf £400 a year.

The increase from 2014 to now – so just 10 years – is absolutely ludicrous considering the wages have more or less stagnated over this period.

Certain people live in bubbles, so have no idea how the rest of society lives. I’m sure Howard Davies really thinks it’s easy for people to get on the housing ladder – because he sees his children and their circle doing it without much problem. That’s why it is important to have people from all walks of life and parts of society in politics and economy. Something we were better at in the 1920’s than we are now. Labour for some reason, if you look at their different short-lists, doesn’t seem to get this. That’s why private schools are poison. We all have to mix and see how other people live.

I’m on more or less median wage, living in a part of UK with relatively cheap housing, and am still giving more than half of my income on housing and utilities. I have no idea how a single person in London with my earnings could survive and lead something resembling a life.

I think those “average” salaries may be average MALE salaries. Just sayin’

I bought my first house, with my then husband, when I was 18 and he was 21. We did this without any financial support from our parents (chance would have been a fine thing).

I would love to know how many 18/21 year olds could afford to do this nowadays.

For the curious, it had 2 bedrooms, a semi-detached new build in Darlington. I think it cost £13,500 but I can’t be certain.

I bought my first flat in less than three times my income in 1983.

Ok, I was a newly qualified chartered accountant but none of them could do that now when the flat in question was three bedroomed in Tooting and in good nick, but no central heating.

The chart on the link below showing average house price inflation to earnings over the last 23 years. It’s clearly not sustainable or in any way economically healthy.

Only a privileged banker could say it is not “that difficult” for people to get on the housing ladder. He probably does not even know that there is a housing crisis. It’s politicians and their banker friends like Davies who are at the root of the problem.

https://www.bbc.co.uk/news/business-67890334

Agreed in all fronts

I was astonished when I heard Howard Davies’ comment on the radio this morning. Amol Rajan pushed back a bit, but nowhere near enough. I bought my first flat jointly with my sister in 1983 – couldn’t afford to buy on my own. I paid a 10% deposit on a £35,000 2 bed flat in Clapham, with a repayment mortgage. Remember, it was only in 1975, after the Sex Discrimination Act passed, that women could apply for a mortgage without facing discrimination. Even by 1983, it was still hard to find a lender willing to take us on.

The best you can say about the mortgage market now is that the endowment/pension/PEP mortgage has long been banished. What a scam they were!

None of my kids have yet bought property. My daughters have moved out of London as they can’t afford the rent there. My son, 32, married, with a child, is hoping to move out of a rented place in London this year and buy somewhere on the coast, with help from parents for the deposit, of course. They can’t afford to buy in Peckham, where they rent, or anywhere else in London. It’s a huge mess.

Agreed

We were neighbours on the Northern Line in 1983

Haha, yes, and I sometimes had to travel south to Balham to get on a tube as by the time they reached Clapham Common they were stuffed already! Mostly I cycled to work though – much nicer way to travel.

My sister bought me out in 1988 and sold that flat in Clapham last year for around £450,000 I think. Nice little earner!!

I gather that is what mine would be worth now – more than my current house

Laughable.

The only way I was able to get on the housing ownership ladder was due to the existence of 100% mortgages, one of which me and my then wife took out to buy a two bedroom maisonette in a not very desirable part of Nottingham in 1981. There was no way we could have found the money for a deposit at that time as neither of us earned enough to save anything.

Interestingly, I know of at least three other friends of similar age who all got on the housing ladder via 100% mortgages and all of them would have been in the same position as we were with regard to never having enough money to save any for a deposit.

I’ve never quite understood why such mortgages disappeared.

My deposit was £250 at the time.

It’s hard to recall now how much this helped with all the other costs of starting a home

£250 doesn’t sound much now, does it, but I recall that £90 was the most I ever had in a savings account through the 1980s. Mind you, as an accountant you should have been at better at saving 🙂

As a new chartered accountant I may also have been better paid than average for a new buyer. About £11,000 I think in 1983. It seemed like a fortune.

But, I also share the cautious characteristic of that profession in that regard. There will always be a rainy day, is my lifelong assumption.

Bankers out of touch?

One of the directors of (I think) Barclays back in the 2000’s had to have help using…………an ATM/ cash dispenser – he had never used one before. Didn’t know what to do.

Out of touch or out of their minds?

What is not mentioned enough is rental costs. When I bought my first place in a dodgier part of S London (now gentrified) in the 70s rents were much less than mortgages. The days of 12-16%… a bit different to the 2% of recent years. Those lower rents allowed people to save. I also wonder whether the wide availability of social housing in those days had the effect of keeping private sector rents down. As well as allowing those council house tenants who could afford it, to save and then move on to buy their own places.

Current rent levels make it pretty impossible for anyone to save. I note that at least one building society (Skipton?) has recognised this and is prepared to give mortgages to people with a good rental record.

Not that Howard Davies would have a clue about any of this.

I comment I used to make when I heard nonsense like that was if he isn’t on hard drugs he ought to be. I’m sure he was the Bank of England Governor in the days of Major,Blair and Brown. I think that proved my point.

One of the factors that emerges when one studies the world of finance is how the promise and reward of money and stature helps people to forget their scruples.

It really is as simple as that with people like Davies I’m afraid and modern capitalism marches forward on this factor by rewarding people to say and do the most outrageous things.

In fact, the average UK house price in 1955 was £2003 ( according to Nationwide) which is 15 times the then average wage. Still not very affordable.

We all know that house prices were much lower in relation to wages in recent history, but if we look at trends over a longer period that seems to be an anomaly. In the 1850s they were about 13x the average wage and in 1900 they had fallen, but only to 8x.

The fact that owning property was unaffordable to most people in the past doesn’t seem like a good argument for continuing that state of affairs, but nor should we make the mistake of thinking house prices were cheap in the past just because we haven’t done a conversion.

The average salary was £400

Please stop wasting my time with nonsense