I have to overload on data this morning: I am on the BBC Radio 2 Jeremy Vine Show at lunchtime to discuss Rachel Reeves' Spring Statement. We will be in air at 1.30.

As I noted in this morning's video,

This Spring Statement is, effectively, useless because every assumption on which the Office for Budget Responsibility might have based it is now completely irrelevant. War in the Middle East has ensured that it's the case.

Oil prices are continuing to climb. This is from Trading Economics:

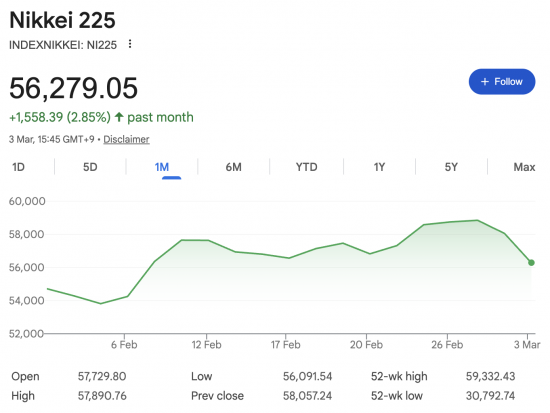

The Nikkei share index in Japan has fallen again in what we think of as overnight trading:

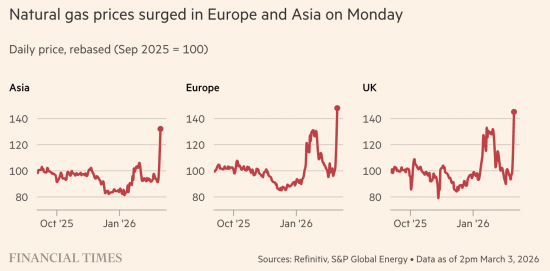

Gas prices are going through the roof:

Inflation is on the cards, inevitably, even if no significant disruption to supplies actually occurs, as was the case in 2022 when we last saw this happen.

Rachel Reeves' spreadsheets won't be balanced as a result. It will be interesting to see what she has to say about that.

I will have live tweeting and commentary here later, and then a video reaction this afternoon.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

It looks like liquefied natural gas supplies from the Gulf States are stopped. The amazing usefulness and flexibility of gas coupled with the drop in supply has increased the price by around 90% since Friday, compared to around a 10% rise in the oil price.

It’s a reflection of gas not being fungible with energy sources like solar and wind. Gas from abroad would of course be fungible with new domestic supply if it were only possible.

Well, the good news is that UK natural gas demand is about to drop substantially due to seasonality. The UK is also consuming less gas each year as renewable generation continues to shoulder more and more electricity generation, with electricity displacing piped gas in more and more households. The UK does rely on imports however, and usually uses the summer months to restock storage. However, Qatar supplies about 5-8% of total uk LNG imports, no real supply issues looming.

The bad news is that gas is still the balancing price for the UK’s mis-managed power sector, so the price impact will be immediate. As an aside, no realistic amount of additional domestic production would change this. The UK exists within a broader European market and has decided to allow markets to fix prices, so the uk will always be at the mercy of international price shocks despite the tremendous growth of renewable energy.

If the supplies resume within 2-3 months the price impact should be quite short lived, if not things will get far, far worse.

Understood. But to treat the UK as an entity in isolation in a global market really does not make sense. We are price takers, not price makers, and our government does not let us be otherwise.