Andrew Bailey, the Governor of the Bank of England, gave another of his excruciating speeches on economics yesterday.

You only had to read it to know how far adrift from reality he is. Start with this:

Monetary policy, in other words, works through the management of aggregate demand in the economy. Simply put, when inflation is too high, we increase Bank Rate to dampen demand; when inflation is too low, we reduce Bank Rate to boost demand.

The obvious question Bailey had to answer as a consequence is where is the evidence of excess demand? In a country with consumption flatlining and incomes falling there can be none. He obviously has not noticed that simple fact.

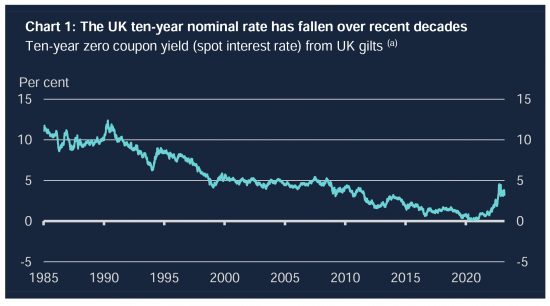

Instead, Bailey tried to justify this chart:

Bailey claimed that the aberrational uptick at the end of the chart, which is of course the result of his policy, could be explained as follows:

A good part of this decline can be explained by lower inflation itself. It reflects the success of inflation targeting in delivering low and stable inflation over long periods of time. Under inflation targeting, monetary policy makers act decisively to return inflation to target whenever shocks cause prices to rise or fall by too much. So even if inflation is now high, people can trust inflation to come back down to target. As a result, savers have come to demand a lower premium to compensate for expected inflation.

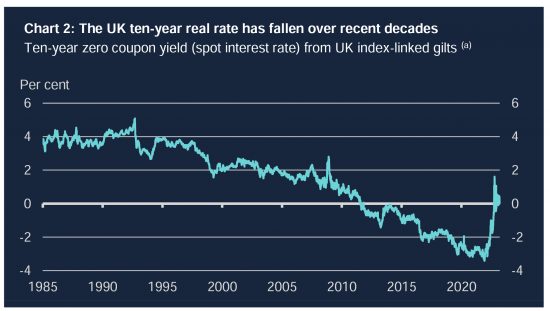

Very politely, this is drivel. The claim is that the Bank has been so good at targeting inflation the need for interest payments has faded away. His own next chart proves that is nonsense:

People did not give up on interest. Instead, rates went markedly negative from 2008 onwards. The trend was heavily downwards. The current policy he is promoting, in the absence of any explanation of its need based on there being no excess demand in the economy, is a blatant attempt to restore positive interest rates. The problem is that there is no evidence to suggest such rates are sustainable.

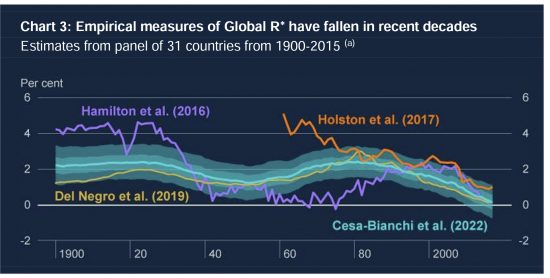

This is shown in his third chart, which refers to global average long term interest rates, where the persistent downward trend is seen since the onset of neoliberalism and the growth in inequality:

Bailey has a different explanation for this. He argues the downward trend is for two reasons. The first is that there are more old people in the UK. The second is that productivity in firms has fallen, especially since 2008. He said:

As people accumulate savings over their working life to fund their retirement, wealth in the economy increases as the age distribution shifts towards older cohorts.

As statements of the obvious go, this is first rate. This has always been true. What he said next is not true:

So ageing households have sought to lend more at a time when less productive firms have sought to borrow less. The only way to establish an equilibrium between the supply and demand in the market for investable funds – that is, to incentivise firms to invest this additional wealth into productive capital – has been for the price of those funds, the real interest rate, to fall.

This is nonsense for three reasons.

First, it suggests that markets set interest rates. But the whole premise of central bank regulation of monetary policy is that the central bank is able to do so. Bailey has to believe that this is true or his whole argument, and job, fails. He cannot make both arguments in the same speech: only one of them is true.

Second, the argument assumes that banks are intermediaries between savers and investors and that investment comes from saved funds. But the Bank of England admitted that this model of banking was not true in 2014. They admitted that it is credit that funds lending and so investment, and so saving. In that case, once again he cannot make an argument that the Bank knows is not true.

Third, he ignores the fact that savings have alternative uses, such as speculation. Financialised markets have not made their returns from investing: they have made money from speculating in money itself. Again, it is absurd that he does not acknowledge this fact.

The result is Bailey's claims make no sense at all.

That said, he may be a little closer to the truth on productivity, where he said:

[F]ollowing the financial crisis, manufacturing productivity growth fell back sharply. This fall in manufacturing productivity is the main cause of the slowdown.

The reasons behind it are much debated – and productivity may be harder to measure in the modern economy where businesses invest as much in intangible capital, like software and branding, as in physical capital, like buildings and machinery. Measurement problems could be a big part of this. But much also points to structural change. Perhaps new ideas have become harder to come by, or perhaps technological innovation and specialisation have faded as globalisation slowed.

I think he is right about measurement. He is also right about the shortage of ideas: there appear to be very few. There is nothing like the idea of the internet around now to transform the whole process of business and to transform markets as there was in the 90s and 00s. AI is not it, I am fairly sure.

But being partially right does not support his argument that business is not investing for this reason. It is not investing for three reasons.

The first is that there are bigger superficial returns to be made from speculation.

The second is that there is that there is no real demand for what business is making. The people with money to spend - the more elderly - are saving more precisely because that is the case.

Third, increased inequality because the wealthier are saving more has reduced the multiplier effect on investment - and so has reduced the incentive to do it.

Even negative real interest rates did not induce businesses to spend on investment. Why Bailey now thinks artificially high positive interest rates, set with the deliberate aim of deflating the market in real goods and services, will achieve that outcome is hard to imagine.

Bailey's argument is that getting older people back to work will apparently solve this problem. Again, when he also thinks that they have the means not to do so, how this makes sense is not at all clear. Indeed, how he even makes the leap from one position to the other - except by saying that this is where the growth potential in the economy is - is hard to fathom.

Bailey concluded saying war has hit us hard, as have the terms of trade (call it Brexit). There is a downturn, he says, in income that we have to acknowledge, but despite that he is intent on forcing inflation down by deflating the economy some more. And, he added, he saw no threat from a banking crisis, to which he had not previously referred. These conclusions did not flow from anything he said. I have to conclude that all that came before the conclusion was a vain attempt to justify high interest rates when in reality none could ever be found in the real economy.

So what should he have said? I offer just three of many things that he might have considered.

The first is that inequality needs to be tackled, very urgently. Money has to be given to those who can spend it and be taken away from those who will not. The distortionary effects of excess savings need to be addressed.

Second, markets are out of ideas because overall people know we do not need more ‘stuff'. What we need is sustainability. It is the exact opposite of more uselessly differentiated products only capable of being sold on the back of massive advertising campaigns that create feelings of dissatisfaction which the products they are promoting cannot dispel because they meet no known human need.

Third, what we need instead is more public services. The way to deliver growth is to supply what people really want, which is an improved NHS, better education, social care and justice, and all from people paid fairly to deliver those things. He is wrong to look to the market for solutions in other words: what we have is a shortfall in state supply in the UK.

Bailey got nowhere near this. It shows how wrong it is to put monetary policy in the hands of such a person and his acolytes: they have no clue about economics, the real world or what is required. Living in their own very comfortable bubbles guarantees that. All they can do is make up falsehoods to justify what they are doing, and as this speech showed, Bailey is not even very good at that.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

I take my hat off to you! You have succeeded where I have failed… you actually managed to read all the way through the speech.

Your 3 points at the end are spot on.

It was grim, but someone had to do it

I agree with Clive, you’ve nailed it good and proper.

Banking should be the tail and nothing more.

The fact that the tail is wagging the dog tells you all you need to know about our elected representatives having no new ideas and the vacuum left behind enables such idiots like Bailey into the gaps.

Bailey certainly makes Mark Carney look like a saint.

Good demolition job – have but link on LSE Events @LSEpublicevents

I read back to the beginning and cannot see where Bailey claimed that there was excess demand.

I quoted the para

It bwasn’t hard to spot

Bailey is reported to have said today that the problems of the SVB ‘caught them by surprise’?

I mean? Really?!

Goodness me – what they don’t know at BoE seems to outweigh what they do – at least to me.

As useful as using a colander to save a sinking ship.

Their field of view is deliberately narrow. Nelson’s I see no ships. Or what we dont know we cant be blamed for…

Imagine a lunatic is driving a bulldozer straight at your house, with the intention of demolishing it. Bailey’s idea of monetary policy is to pick up the gravel in your drive and throw it at the bulldozer, in the expectation that will stop it.

The suggestion that early-retired 50-64 year olds are a significant factor in the rate of inflation is utterly risible. As someone in that category, I wish it were true, but I doubt I have spent nearly as much of my redundancy and pension lump sum on stoking consumer demand, as opposed to having had my civil service pay cut over 12 years of tory government.

Nobody ever suggests any more that many of those 50-64 year olds have left the workplace because of long covid.

I do

But officially the neoliberal narrative is that Covid never happened now

I listened to his speech as well, as did a prominent economist I know well. We exchanged live messages on how dreadful it was. Like a year 1 primer for economics students. I wonder whom he thought his audience were. No real acknowledgement of the supply drivers of current inflation or of the negative consequences of his interest rate policy. Dismissed any idea of fiscal (spending) interventions as not his business – though he could perfectly well have commented.

I’d add a fourth point on why investment is so low. For SME’s they struggle to get any kind of finance – unless they are some kind of tech business than can be bought and sold again in the near future at vast profit. Banks have neither the skills to understand their business (they shed all that years ago) nor the interest. For larger, public companies, the pressure from the City is for profit maximisation, dividend distribution and share buy-backs. That is seen at its starkest in the privatised utilities. That means minimising the kind of investment in people, R&D, technology that pays off in the longer term.

Thanks Robin

Much to agree with

I did read the speech – or forced myself to. As it was delivered to the LSE it would be interesting to know what questions were asked, assuming they were allowed. There are plenty at that school who know full well that it was 90% nonsense.

I was listening live and there were lots of questions, both from within LSE and outside. There were plenty questioning the dogged pursuit of interest rate cuts and lack of attention (by the government) to the fiscal side but Bailey either waffled or they were ignored.

If you’d wanted an illustration of why Richard is so critical, Andrew Bailey provided it.

PS The Post-Crash Economics folk and their book are especially critical of LSE teaching. The book is well worth a read – and it’s short and readable! Think its on Richard’s recommendations

Are you referring to this one? https://link.springer.com/book/10.1007/978-3-319-65855-1

LSE is generally pretty grim on economics

Thats the book. Quite understandable by non economists.

Suspect its not popular with LSE academics.

There are plenty at that school who know full well that it was 90% nonsense.

Is it the case that many know it’s nonsense but find it easier and more profitable to “go along with it” and make a career of speculation rather than doing something useful and productive?

I must admit I could not bring myself to read through this stuff to the end but I suppose it is no surprise that Bailey would deliver something like this.

Here is a man who has never worked in the real world of manufacturing, dealing with industrial problems, financing innovation through R&D etc and winning export orders in countries where English is not spoken.

Fortunately his waffle was diluted by my listening to Radio Caroline UK Pirate on Spotify!

Caroline takes me back…at least I got good reception where I grew up

“Perhaps new ideas have become harder to come by”.

This is not true. Allow me to use an analogy. Without Maxwell’s theory (equations) of electromagnatism, and Hertz’s experiments there is no modern digital world. Nevertheless, Maxwell struggled to see any value in – the telephone. The first patent for a fax machine, by Bain in the 1840s (pre-Maxwell’s theory) worked imperfectly, but as important, few saw its economic value at the time. Faraday invented the eletric motor in the early 1820s. Essentially we are proposing to use Faraday engines in our modern cars, as if it was ‘cutting-edge’ technology.

Major ideas often take many years to exploit the economic potential fully. We are only now seeing the fulfilment of the economic potential of the internet, in an exponential growth in business and consumer apps, and the dangerous communications revolution in ‘surveillance capitalism’; 40 years after its invention; and the spectular false dawn of the revolution, before its time in the dot.com bust in the early 1990s. Economic success does not follow, even if money is thrown at a brilliant idea, before the world can handle it. The internal combustion engine was invented circa 1860s/70s; it was the turn of the century before it had real impact, and now is only coming to the end of its consumer application, 150 years later. It is a very old technology, but until recently, did not seem so. Its many applications, in a vast array of profitable consumer and industrial products were unimagined by the inventors.

I make no value judgement about all the applications made from these seminal inventions; because many that may seem quite pointless or even valueless in retrospect, may have been eonomically successful and highly profitable. However snooty we may wish to be, economics does not follow closely what we may wish to deem virtuous priorities.

The innovation is in battery technology. I know scientists working in materials science on battery technology.

Also our electric motors are much more powerful and efficient and come with microprocessor control.

You are ignoring a lot of innovation.

I do not doubt that there is innovation

I want more e.g. on tide technology

But, will they change thevecon9my in the way the internet did?

Or am I suggest8ng the wrong criteria because growth is not the right indicator?

I do not know to whom You are directing criticism, but I am ignoring nothing. I am contextualising how innovation has worked.

Remarkably, this article popped up in my phone’s Google news feed overnight! I realise, of course, that one’s news feed learns what topic-areas are of interest ( broadly speaking, economic policy) and reflects that, but I normally get mainstream articles from the likes of Guardian/FT/Telegraph/the broadcast media. This is the first time taxresearch has appeared, and pleased to see it.

It seems that Andrew Bailey, operating as a Treasury stooge, is finding it increasingly difficult to offer anything remotely coherent as a justification for the Bank’s abysmal Rates policy.

Incidentally, re your last reply, why indeed is tidal-power for renewable electricity generation seemingly so neglected?

Wow

I admit to surprise

And I wish I knew why tidal power was so neglected

The claim is made it is too difficult for investors. But like all the really big innovations, it requires public financing to take the risk first, at scale. The UK do not do it because the markets are adverse to real risks they can’t manipulate, or palm off

Thank you! Most illuminating.

But one issue I would emphasise is AI – my hunch is that it will transform business & economics more than we can possibly imagine at this stage.

Maybe

And to what gain?

I don’t know. But I plenty of futurists point towards AI replacing many cerebral jobs like lawyers & doctors for example – or perhaps such technology becoming the mental equivalent of mechanical enhancements. Just like robots changed the production of cars. This points to a transformation of labour & issues around the ownership of such tech. I don’t know but I don’t think AI can be dismissed as inconsequential

You ignore that no one goes to a doctor or lawyer for the answer they can give

They go for reassurance

AI cannot give that

Your second point towards the end I concur with entirely. The world went wrong when “customer” was replaced with “consumer”. We need to move away from the capitalist, market mindset.