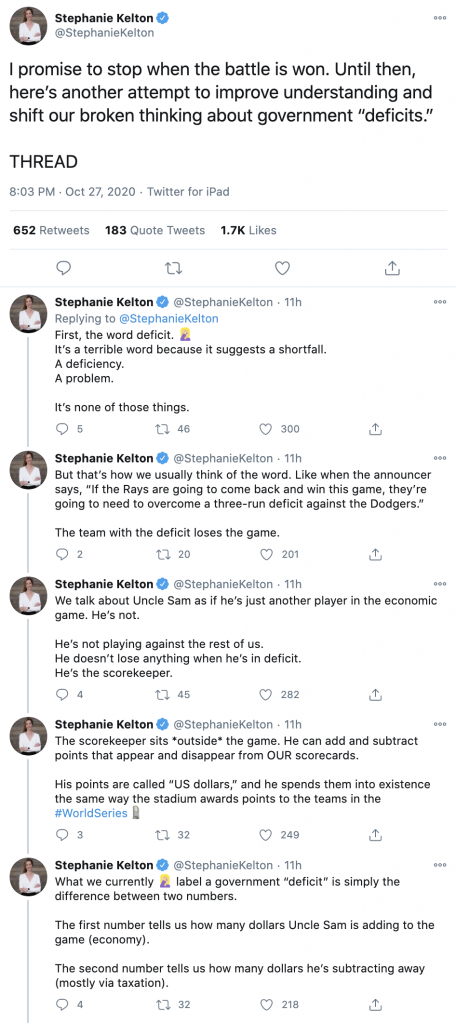

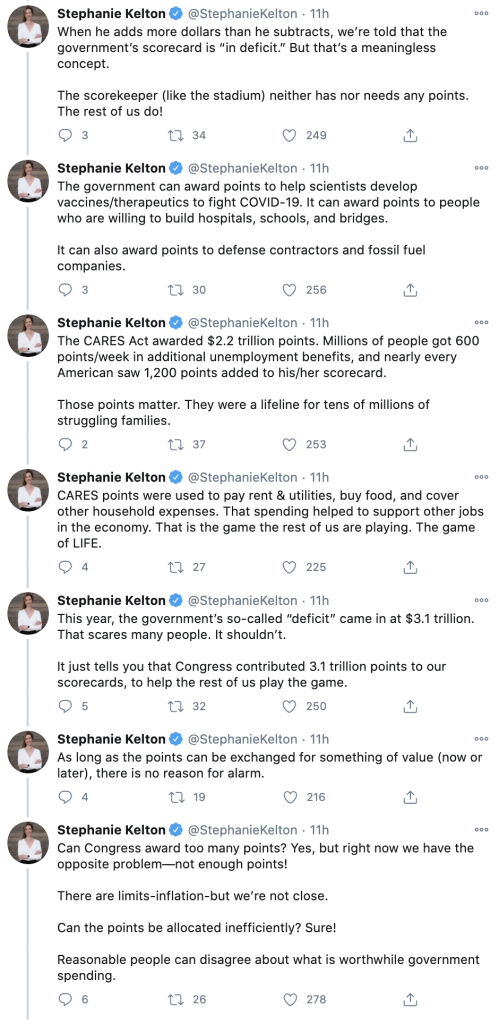

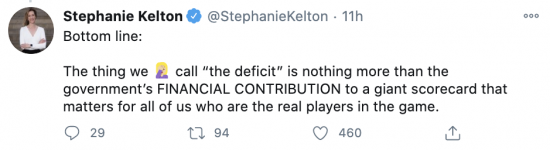

This is a really good thread from Stephanie Kelton:

And for those who ask how I reconcile this with my call for hypothecated saving, that's easy: hypothecated saving is investment funding, and not borrowing.

Borrowing is deficit funding. Hypothetcated saving is purposeful activity for a specific goal.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Very good explanation and easy to follow. Sadly, the ‘govt. is like a household’ myth is so entrenched with media and many in the population that this explanation may only break down one of many, many barriers.

It’s a start.

Craig

It was Warren Mosler who I think first used the scorecard analogy. I think I first came across it in something Stephanie Kelton wrote about the dawning of her understanding of MMT; through Warren Mosler.

It’s in the book…

Prof. Kelton writes well — almost as well as you!

I think there is more “thinking” to be done on savings. As far as I can tell, MMT does not really have a view about saving — other than how it might impact “capacity utilisation” in the economy and any resultant inflation. But savings levels and the change in savings levels are part of the balancing act that MMT seeks to achieve.

The first observation is that saving is not an option for many people. Low pay, high rents etc. prevent it. That IS a problem but not what I am writing about.

The problem with saving is that I can store money/gold/land etc. but I can’t store what I really want to consume in the future which will be, broadly speaking, other people’s time. Will my money be exchangeable in the future for other people’s time? And at what exchange rate? Saving more might help me….. but at a macro level, if everyone saves more then we just have more money chasing the same pool of goods/services. In aggregate, nothing is achieved. Worse than that, money saved is money not spent which potentially leaves resources being under used today.

The challenge is to raise the amount of “time” available in the future for the things that people will want….. and the only way to do that is to do what we can today in order to free up time from certain tasks in the future. The obvious answer is to address climate change — this needs huge amounts of work and if done today it will free up time in the future for tomorrow’s workers to deliver the things we want then. Given the urgency of climate change and the huge pool of untapped resources resulting from the pandemic this really is a “no-brainer”.

Handling the desire to save and balancing its good and bad aspects is more subtle — but still important.

People save for various reasons – “saving up for a new XXXX”; “saving for a rainy day”; “saving for old age”; “saving to show off” for example.

Saving up for something is a perfectly reasonable and from a macro perspective not a big deal because the cycles are relatively short. Interest rates paid on these savings are not that important.

Saving as a competition to accumulate more money than others is absurd. Technology has created a “winner takes all” economy and for the sake of everyone — including the billionaires themselves — this needs to be taxed away…… and certainly not rewarded.

The more interesting challenge lies with the other two. Saving for a rainy day and saving for old age are both reasonable, too. But how much? The critical thing I need to know is what support might I get from the state. Many people are finding out for the first time that the “rainy day support” is pretty meagre. As the economy recovers many people will rethink what “rainy day” money they need and will save more. The solution is straight forward — a more generous benefit system. Not only will that money be spent today to support other workers it might also aid the recovery as re-employed workers do not feel the urge to aggressively save.

It is also tough for pension savers. Without a defined benefit scheme I am juggling life expectancy and expected investment returns. I budget assuming zero returns and that I will live to 100 so I end up saving more than I need to. A better state pension and the ability to save or buy an annuity at a decent rate would let me save less.

It can be thought of this way. I could stash cash for all emergencies…. or I could by insurance. By pooling the risk the insurance company’s stash of cash is far smaller than the aggregate stash that its policyholders would have to hold.

We need a tax, benefit and interest rate policy that encourages a sensible approach to saving. It should aim to reduce the pool of savings held for “insurance “ (against a rainy day and old age) but offer a fair return on savings that are reasonably held against those risks.

Clive

Apologies for taking many hours to get to this

I describe what you refer to as the fundamental pension contract, of which I have said :

This is that one generation, the older one, will through its own efforts create capital assets and infrastructure in both the state and private sectors which the following younger generation can use in the course of their work. In exchange for their subsequent use of these assets for their own benefit that succeeding younger generation will, in effect, meet the income needs of the older generation when they are in retirement. Unless this fundamental compact that underpins all pensions is honoured any pension system will fail.

I have read some of what you have written on the fundamental “contract” between generations….. and I think we largely agree. My first section restates (less concisely) what you have already said but I guess what I am interested in is exploring how this contract evolves.

Clearly COVID and Climate change are central to this but on the periphery I think we need to understand how these very large pools of pension money are deployed

Savers are complaining about low rates and one response is to say “if you don’t like it then don’t save”. That is not an unreasonable response but I think something more nuanced is required. I suppose I am trying to make the case for a tax and benefit policy that reduces the desire to save which then permits an interest rate policy that offers a sensible (zero real) rate of return on long-term gilts to those who do wish to save reasonable amounts.

Why does this matter? At present QE is seen as “what we do after rates can’t be cut any further” and supposedly helps the economy by making borrowing cheaper across the yield curve. In practice, the economy is not constrained by lack of credit (or price of credit) and in reality QE acts by allowing governments to spend directly into the economy.

I fear that without efforts to reduce this pool of savings and/or an offer of a “natural” home for them then we will see destabilising flows that will produce asset bubbles, FX crises etc. as pension (and other) savings tries to find a home in whatever is the fashion of the day.

Is this top of list of “things to worry about”? No, does it matter? Yes.

I think we are agreeing, including in the fact that this another issue MMT needs to finesse

Clive, I think you go to the heart of the issue for many of us: What will we do in retirement without a DB pension scheme? I cannot buy an annuity to guarantee me a useful income as the returns are dire. I get no return on cash savings. In my view my options are to buy shares or property to rent out.

That suits many of us – part of our income is from government via the state pension and the other part from investments of some kind.

Whatever happens with the acceptance of MMT ideas, anything on pensions is going to happen long after I need it, if ever.

Hi Richard, 2 quick questions related to this.

Is the UK Debt the total amount of money created over the years and pumped into the economy (including investments, savings, bonds etc.), minus the amount taken back as tax over the years?

If so, why is it called ‘borrowing’ ?

It is often written that Govt. ‘borrows’ at market rates, however, would it not be correct to say the Govt sets the rates to make them attractive to the market for investment, so as to reduce the need to create money, and therefore has control of the rates?

Sean

No, because QE also has an impact

And the gov’t does, of course, heavily influence rates

It may not absolutely control rates but it is very close to doing so

Stephanie’s general point is correct but the analogy of a scorekeeper who “sits outside the game” is not helpful.

The government is the single biggest actor in a modern economy who’s very much part of the game.

In countries running current account deficits like the UK, the government’s net spending (aka its deficit or surplus) determines whether and how much the private sector prospers or not, in terms of being able to generate profits (businesses) and save (individuals).

(It’s a mystery to me why “fiscal conservatives” don’t understand that all government spending boosts British business, unless it’s saved or spent on imports).

For British readers, a better way to convey Stephanie’s general point might be to point out that the British government is the monopoly issuer of the currency used in the UK. It’s called the pound sterling and it’s simply a government IOU (“I promise to pay the bearer on demand…”). In principle, there is no limit to the amount of IOUs (pounds) the government can issue (spend) and it obviously doesn’t need to obtain IOUs in order to issue them, whether through taxation or borrowing. So the idea of a “deficit” is nonsensical.

(Taxation withdraws IOUs from circulation, reducing the private sector’s spending capacity and preventing inflation. Borrowing enables the government and central bank to adjust interest rates).

Although the government can issue unlimited amounts of IOUs, the authorities must carefully monitor overall spending in the economy (by government, businesses and individuals) in case excessive aggregate spending threatens to exhaust the economy’s capacity to meet demand, which would ignite inflation.

p.s. One of the world’s biggest ship charterers is planning to fit sails to its ships in an attempt to cut carbon emissions…

What will they think of next?

https://uk.reuters.com/article/uk-shipping-cargill-wind/cargill-looks-to-use-wind-to-cut-carbon-in-shipping-idUKKBN27D1UF

Thanks

Comment appreciated

@ Norman

“Borrowing enables the government and central bank to adjust interest rates”

Since March 2009 the UK government has paid interest on reserves this sets the base rate.

That, I think is the purpose for doing so

It would seem to be effective in short term rates

Helen,

You’re absolutely right. Thankyou.

Since governments don’t have to borrow to finance their “deficits”, there must be a reason why they issue bonds, especially those which pay interest on bank reserves.

Suggestions include: for ideological purposes (to drive home the incorrect message that ”like households, governments shouldn’t spend more than they earn”); for use as collateral in the private credit market; to provide a safe, long-term, interest-bearing investment for wealthy people, banks, corporate savers like pension funds and foreigners, as well as a benchmark for other borrowers in sterling, and to provide their pals in the City with a risk-free instrument to speculate with.

If you think we don’t need the City in the foreseeable future, dream on

We do

Norman.

The wheel perhaps?:)

As soon as a private sector bank decides to issue a loan it’s running a “deficit”, its books are unbalanced. It’s running an “unbalanced” or “deficit” flow. Are we to do away with bank loans because private sector banks plunge themselves into debt in this way? Of course not!

To paraphrase Karl Polanyi:-

“The transformation to a capitalist market economy from a hunter-gatherer one, or even to some degree a feudal one, implies a change in the motive of action on the part of the members of society: for the motive of subsistence that of gain must be substituted. All transactions are turned into money transactions, and these in turn require that a medium of exchange be introduced into every articulation of our dominating market work-place lives.”

I am not sure how well the paraphrase of Polyani reconciles with Graeber.

Well it hinges around how you interpret the word “gain” it doesn’t mean that gain has to be entirely selfish. Graeber would be comfortable with the idea it should incorporate a moral compass so that we all “gain” well-being equitably. Clearly few, for example, would want to go back to a hunter-gatherer life of subsistence for health reasons even if the working hours were shorter.

Helen,

When a private sector bank makes a loan, it creates a deposit in favour of the borrower and enters that amount on its books as a liability. At the same time, it enters the same amount on its books as an asset.

Its books are always balanced. It’s illegal for banks to operate with books that don’t balance.

In the banking racket, all loans are “assets” (i.e. amounts owned by the bank) and all deposits are “liabilities” (amounts owed by the bank). In the case of a loan, they refer to the same thing, which is created out of thin air by the banks.

Loans are sometimes called credits. Liabilities are debts.

The term “deficit” usually refers to a shortfall between income and expenses, aka a “loss”. Most banks try to operate at a profit.

Although very interesting, not sure what Mr. Polanyi’s wisdom has to do with bank accounting.

Debit = credit does not equal balanced

Banks are notorious for the assets being long term and the liabilities being short

The ‘financial contribution’.

Yes. Indeed.

The ‘deficit’ is just a record of that contribution. After all – that’s just good accounting isn’t it? What is the State supposed to do – hide its achievements and commitments under a bloody bushel? To make it appear it makes no contribution?

Now…….. I wonder whose agenda that would benefit?

I have a problem with the game-scorekeeper analogy as, in this case Kelton tosses out, an apt description of deficit investing. Neither team enters the field expecting or relying on a scorekeeper for the points that will propel them to victory. Each team must earn the points with execution of their skills, or failure to execute to keep the points from being scored against them. The scorekeeper merely accounts the acquisition of execution.

The scorekeeper doesn’t decide the game isn’t exciting enough and requires the awarding of, or extraction of points to one side or the other to feed energy into the game. And games, with scoring, are win-lose propositions and MMT is win-win. This analogy is a lose-lose.

Interesting

Thanks