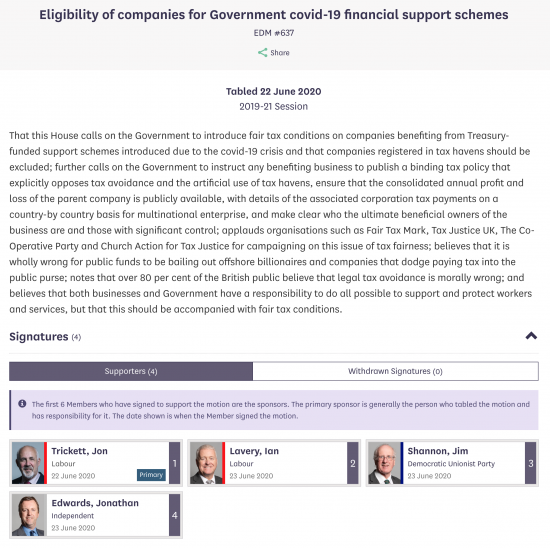

This won't go anywhere of course, but it's still worth noting:

At least some parliamentarians think that attaching reasonable conditions to bailouts is appropriate.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Promising.

I’d have thought there would be more progressives in Parliament than four. Unless there’s something in the detail of the edm or some other politicking going on.

I’m disappointed that the SNP aren’t backing or involved in this. Culturally inclusive, socially progressive, economically tartan tories. Frustrating.

Shall just have to keep going with what you said in another post, about repeating new, progressive ideas over and over, until they replace the outdated, failing processes.

Maybe I should send Nicola Sturgeon ‘The Deficit Myth’ once I’m finished reading it.

Do….

Did Alistair Darling impose reasonable restrictions on the bankers concerning under-writing lending amounts on the bankers after their 2008 financial crash bail-out to prevent future hyper-inflation of house prices?

No

Richard, you really don’t understand the sigbifciant changes in mortgage underwriting post 2008?

Presumably you also don’t understand the significant changes to bank regulation and capital requirements that followed 2008 either?

I am very aware of the changes

But I am also aware of precisely what the limitations of that were

Yes, regulations were changed substantially. All lending is backed by more capital and that includes mortgages. Banks also have to be more liquid, too.

No, this has not stopped house prices rising.

The point of all the regulations was to make the banks safer so that they would never need a bail out again. What they have NOT done is address the need to direct lending towards productive economic activity. My personal view is that Credit Controls might be the only answer.

I am not sure that “The Deficit Myth” is going to worry too many mainstream economists or conservative politicians or necessarily revolutionise the policy sphere either here or in the US.

Whilst the book correctly sets out the basic premise that Government does not have to tax before it spends, that tax is a tool to combat inflation and what matters is the effective use of resources not the level of deficit what it doesn’t really say is how MMT allows policy makers to use that knowledge. Having set out the basic premise above the middle chunk of the book devotes itself to a wishlist of mildly “progressive”/left of centre desires which could have been articulated without any reference to MMT.

In my view the book fails to detail;

1) How policy makers can identify spare capacity in the economy

2) If that spare capacity exists how it can be used effectively by government in an efficient manner. Critics will argue that central planning has always failed in a real world setting.

3) She accepts that once full capacity is reached there is effectively an inflation constraint to further increasing the money supply. If that point is accepted and she does what she is in effect saying is that at that at full employment any future government spending is funded by tax rises and therefore the taxpayer.

4) Given that the spare capacity condition cannot be accurately calculated and therefore where the inflation will kick in any non-MMT economist could argue that at least by targeting government borrowing/”debt” however crude that target may be they have a better mechanism for controlling inflation before it happens than MMT does.

5) It is accepted that overseas trade does export jobs and that manufacturing industries will move to cheaper locations. The MMT solution is a Federal Job Guarantee that is difficult to envision working in any real way for displaced workers and could be used by Trumpian tariff mongers as a justification for using tariffs and keeping “good” jobs at home.

The job guarantee fails in a number of respects for me.

1) It is too complex for any government minister to risk managing even if they had the ability to do so which I doubt especially as it would be centrally funded but locally administered.

2) The argument that skills can be maintained is unlikely. If a steel works or car plant shuts down it is almost impossible for those skills to be replicated in a community with what is in effect a paid volunteering job creation scheme. Those industrial skills will be lost.

3) Anyone managing the scheme will not want to see workers entering and leaving the scheme at points throughout the programme especially if any degree of training is required. Managers will see what they are providing as vital and will want to attract workers rather than see them return to the private sector. That will encourage them to bid up the wage level for those workers.

4) Conversely private sector businesses will bid down the labour costs they want to hire to a point just above the level set by the government because they know that the alternative for a worker that loses their job will only be the rate guaranteed at the set level. There is no incentive for businesses to offer high wages.

5) Trade Unions will want to have a say in the terms and conditions of employment. They will not want to see the jobs as tokenism. If the jobs are required then they should be permanent and remunerated at a level as high as in comparable private sector industries.

6) Labour is not a fungible commodity. An hour of skilled building labour is arguably more valuable than an hour of litter picking yet my understanding is that all labour will be priced at the same set rate. That could lead to resentment in my view.

I was hoping for a much clearer path to show how the state’s money creation capability could be used to change the way the economy can work for many more people than it currently does. I would be happy to be disproved and corrected.

I admit to being very tired this evening: one of my very large deadlines has been met, but another requires much work before the end of the month so I am afraid my response will be brief.

First, you miss the purpose of the book. That was to say that the idea of deficit constraint is not real. That’s it. It was a massive objective. It does it. There’s time for another book after that.

Second, the evidence that we are not at full employment and that there is capacity is that there is no inflation from domestic / non political shock sources.

Third, you’d appear to prefer unemployment than take the risk of full employment. I am bemused.

Fourth, I am bemused about your dismissal of a JG. Sorry – but it just seems you just do not want to believe it – rather like you don’t want to believe there can be spare capacity.

And fifth, clearly you are unaware that we have a minus wage that delivers all the downsides you talk about already and a JG should be pushing wages up, not down: that’s the whole point of it.

No, Stephanie did not deal with all these points. No reasonable book could.

But all the answers are available and to not look for them makes no sense.

I hope others might wade in now: I am packing up for the night.

A bit late in the day…… but, at Richard’s invitation, I will “wade in”.

Let’s park the Job Guarantee scheme for a moment and focus on your first 4 points that ask directly about the operation of MMT.

(1) You are right – it is difficult. Indeed, Central Banks have been trying to do just that and have floundered over the last decade (and more) on this issue with inflation undershooting in most countries. But, whether we have MMT or carry on under the current regime, it makes no difference to identifying when inflation might (or might not) kick in. It is difficult.

However, what we DO know is that the level of Government Debt or Deficit is not a leading indicator of future inflation. Japan have been “at it” for 25 years and the price level has scarcely changed in all those 25 years. If a variable is NOT a leading indicator for the thing that matters it makes sense to drop it as an intermediate target. So, Governments/CBs SHOULD be looking at Producer Prices, wage levels etc. (where the linkages to CPI are clear)… but NOT the deficit where the link doesn’t exist.

(2) MMT does not specify “central planning and control”. Merely that there is a list of “things we want” and that, inflation permitting, Central Government should allocate money to achieve those things. Those “things” could be determined locally, they could be provided by the private sector. There IS evidence that some goods are best provided centrally but I entirely agree that devolving spending decisions and execution to as local level as possible usually delivers the best results and MMT does not preclude this approach.

(3) NO. Central to MMT is the idea that spending is NOT paid for by taxation… whether the economy is operating at full or only partial capacity. What IS true is that if the economy is operating at full capacity and the government chooses to increase spending then that money will have to be drained either by taxation or issuing gilts (in order to prevent rising inflation). MMT says government should try to keep the economy operating at full capacity and that if inflation starts to pick up (as capacity constraints are breached) it must drain money from the system. MMT is indifferent to spending cuts, taxation or bond issuance. Which tool is used is up to the government of the day…. but debt and deficit levels should not direct policy.

(4) I disagree. The evidence suggests that existing models that use Debt and Deficit levels to predict future inflation have failed…. and that failure is not academic it means lives lived below what could be achieved. MMT is an attempt to address that failure.

In summary, MMT is about allowing the economy and everyone in it to operate to their maximum potential and whether you are on the Left or the Right this is surely a good thing.

Many thanks

Mr Gray,

Richard and especially Mr Parry have replied trenchantly to your comments. I have nothing useful to add, save to note you begin with this: “I am not sure that “The Deficit Myth” is going to worry too many mainstream economists or conservative politicians or necessarily revolutionise the policy sphere either here or in the US.

Whilst the book correctly sets out the basic premise that Government does not have to tax before it spends, that tax is a tool to combat inflation and what matters is the effective use of resources not the level of deficit…..”

As the dinosaurs of neoliberal economics (whose greatest success was to survive 2008 as if nothing had happened, because they are so good at what they do – survive their own blunders) look for ways to ensure their survival in spite of being found out – again; you have neatly summarised their technique (give them credit); adopt the new wisdom, embrace it; say that was what you always understood – and change not an iota of thinking about all the issues that flow from it. Contribute precisely nothing.

The real trick, however is that from the bastions of privilege they currently hold, and intend to keep; the neoliberals claim that MMT is still wrong because it has not provided all the answers, neatly packaged; or already corrected the 40 years of catastrophe that mainstream economics has created. So neoliberalism was right all along. Nothing has changed, and nothing will change – neoliberalism guarantees it, no matter what. Then they can all go back to sleep, their tenures safe, yet again.

Well said

Patrick Jenkins also says there should be conditions in an FT editorial today. There is progress on this.

I was also intrigued by Martin Wolf’s “summer reading list”. Of course The Deficit Myth is there but also others on UBI, problems with Capitalism etc. – I wonder if we tracked back and looked a previous “reading lists” if they were a predictor of changes in thinking of “mainstream economists/politicians??

Interestingly, he says that MMT is right but he doesn’t trust politicians to do a sensible job. I guess that is a start…… but my question to him would be “and you think they are doing a good job now?”

Alex Cobham too….

What I think is important is that, if I who is hugely sympathetic and agree totally with the principle about deficits, cannot be persuaded by this book then how on earth can you hope to convince those that disagree who are currently in the majority that the methods proposed will work.

To counter some of your comments;

1) I don’t miss the purpose of the book but am disappointed it was not more precise in its refutation of existing economics.

2) I am being devil’s advocate. Critics will argue MMT is seeking direct Government action and therefore centralised planning. That needs to be refuted or accepted. There is nothing inherently wrong with the state getting directly involved with the provision of some services. The world will will struggle to combat climate issues without state intervention.

3) I have no desire to accept unemployment and that is my misuse of language if that is what came through. I want to see good jobs at proper wages and if that means the state provides them then I am all for it. I believe private companies can and do provide many good things but there are some things that private enterprise will not provide. I am in this respect more of a central planner than many. A key fact is that the state can provide these and pay properly for them because the state can create money and where there is spare capacity these can be provided at no risk of inflation. Government currently uses the inflation risk element to suppress wages and conditions of state employed workers and to refuse to invest in other needed assets that the private sector does not provide which is simply a neoliberal untruth.

4) I don’t understand your 4th point. Clearly there is spare capacity. My point is that MMT does not say how much or how to calculate it. That is a point of attack for critics. As for the JG you are right I don’t think it works as set out. What the state should be doing is saying this is what we need to benefit our society and these are the jobs we need to do it. A JG is a US solution that fits a US culture.

Your last para is slightly disingenuous. Yes I could look them up and do but the book and some of your other commentators who wish to send it to mainstream politicians seek to use it as the last word.

And a quick word re Clives number 3) I totally agree that taxation doesn’t directly fund Government spending. But Clive critics can argue that at full employment, and I also agree that full employment may in fact never be reached, it is possible that any further spending has to be matched by increased taxation. It is important to rebut such issues and not leave them hanging and leave the deficit myth open to refutation.

I reiterate I am a supporter of the principle of MMT and to state intervention where private enterprise fails but I have never been someone who blindly accepts something. A key principle for anyone should be “can I refute my own argument”. That way we get better theories and better policies.

I am baffled

You want one book to solve all problems?

Really?

And because in the exceptional – and unknown in event history – of full employment at living wages taxes have to equate to government spending (not fund them I stress, just equate to them) if inflation is to be avoided you say that the argument fails?

Why?

I’m baffled.

It is not me who wants one book to solve anything. It does seem that no criticism is allowed. That is odd seeing as you have just trashed someone else’s book.

As for your last point you are putting far too much emphasis on it. It is a minor argument upon which you are focusing all criticism. OK forget the minor issue that at some extreme event taxes do in some way fund spending. It is irrelevant but there has to be debate not simply acceptance.

Dammit, have you seen the debate on MMT here over the years?

And criticism, from me included?

The is one book with a purpose, but the answer to everything