I wrote a reminder of the danger of the end of December in financial markets yesterday. In it, I highlighted the rise in the price of precious metals, including silver. And yesterday, as the FT reports, the silver price fell by nine per cent. Gikld fell by four per cent.

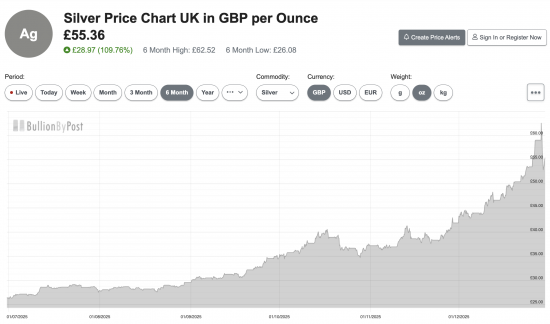

The silver price looks to be especially erratic and irrational, as this chart shows:

The month chart highlights the volatility:

This is what happens when hubris and speculation defeat any fundamentals in investing logic, and bubbles occur.

I am aware that China is making changes to its silver trading, and this may have driven some activity, but the reality is that this is trading disconnected from the real value of silver.

This might be more apparent in the case of silver, a commodity, than in trades in AI shares. The overvaluation still exists in both, though. Corrections are still required. This one began just a little sooner than I expected, though.

Comments

When commenting, please take note of this blog's comment policy, which is available here. Contravening this policy will result in comments being deleted before or after initial publication at the editor's sole discretion and without explanation being required or offered.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Richard,

I saw something on the internet and sent it to you – with a pinch of salt but its been suggested that a major bank has defaulted on some ‘silver’ trades. Now if its (probably) not true I suggest that whoever created the story thought it was credible.

So I wonder what things will look like in the first week in January?

I can find no evidence for this, as yet.

Although I would say this, I do think that the time for rather more certainty in one’s financial life has arrived. It is possible to remove all but inflation risk from one’s capital by ‘running for cash’ with National Savings & Investments and well-capitalized building societies – far preferable institutions than the high street banks and banks that no-one has ever heard of.

If you are old enough and have a defined contribution pension plan(s) then consider switching your funds to a more stable choice such as the cash/deposit fund, even if only on a temporary basis, whilst you take stock.

Pension annuities still offer value, certainty, and ‘safety’, in my opinion. Of course, I do arrange these as part of my work with clients and they are becoming more and more important as the ‘Baby Boomers’ retire en-masse. Just yesterday, an new pension annuity completed. The fund was held in an old FSAVC and, in roud numbers, was £80,000. £20,000 tax-free cash was paid as a lump-sum and £60,000 was used to buy an annuity. The applicant is 71 and his partner 70. A joint life, last survivor annuity has been bought, with a 66.67% survivor’s pension should the applicant die first. The annuity also includes a 5-year guaranteed period, overlap, and a proportionate payment and, most importantly, will be adjusted annually by any changes in the RPI with a zero floor (meaning that it will not decrease in payment). The annuity payable is £3,383.64 in the first year, payable monthly in arrears, before the deduction of any income tax due. I think that an inflation-adjusted 5.63% ‘rate’ is very attractive. Our fee was 1% of the purchase price, just so you know.

Thanks, Mark.

And, much to agree with.

This article implies there are a few things going with US banks and also the silver markets that could be signs of issues to come:

https://www.dcreport.org/2025/12/29/ny-fed-unlimited-cash-infusions-bank-crisis/

I know two of the three reporters. I strongly suspect they are right.

Yikes.

https://www.dcreport.org/2025/12/29/ny-fed-unlimited-cash-infusions-bank-crisis/

Agreed