According to the FT:

Defaults on US credit card loans have hit the highest level since the wake of the 2008 financial crisis, in a sign that lower-income consumers' financial health is waning after years of high inflation.

They added::

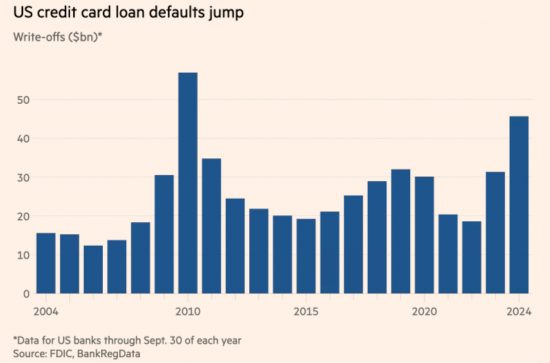

Credit card lenders wrote off $46bn in seriously delinquent loan balances in the first nine months of 2024, up 50 per cent from the same period in the year prior and the highest level in 14 years, according to industry data collated by BankRegData.

The data looks stark:

Note that the data does not appear to be adjusted for inflation, but the trend appears to be very clear nonetheless. I think four things stand out.

First, post-Covid people have had to borrow to cover for declining real incomes. Inflation has obviously not helped this trend.

Second, many have obviously reached the limit of their capacity to borrow as indicated by their inability to repay what they owe. This suggests they face the likelihood of growing real poverty.

Third, there is a debt crisis in the US ( and almost certainly elsewhere) but it has nothing to do with government debt and everything to do with private debt.

Fourth, if this is a growing trend - and it appears that way - then this only adds to the concerns for 2025. Debt crises almost always precede economic downturns.

In summary, worry, because we do not have politicians who look as though they might have the imagination to deal with situations like this.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

Where actually is the money that the credit card companies have lost? How much still exists?

Michael

When will you get it? There is no such thing as ‘actual money’. It has no physical existence. It is not somewhere else. Money is a promise to pay. This promise to pay failed. The money ‘lost’ represents the value of the promises that failed. The credit card holders got goods they did not pay for. The bank had a hit on its equity. That’s it.

I am not sure I will answer this question again. You are wasting my time now.

Richard

Let me see if I get this right.

The credit card holder received goods and/or services. The bank promised to pay the provider of those goods/services. The credit card holder promised to repay the bank, so the bank was broadly flat, with a credit and a debit (a receivable and a payable).

The service provider probably made a profit (financial upside) and no doubt used the promise from the bank to secure goods and services from others, and/or pay employees or distribute to owners, and/or pay taxes, but ultimately the credit card holder did not repay the original bank. So the bank ended up with a payable but not a receivable and that difference represents a loss (financial downside). That loss destroys some of the banks capital (accumulated profits, or other equity capital).

Essentially the bank has given some of its capital to the service provider and the credit card holder has got something without paying for it.

“Exists” is a tricky word, but presumably the amount of money in circulation has increased slightly.

A fair summary

Richard, I am sorry we are at cross purposes. And thank you Andrew for putting so clearly the point I was aiming at. Yes, a $ is an IOU. I am no economist, but I was once a research scientist. There you are always looking for things that don’t quite fit, or suggest that something interesting is going on. Most, maybe almost all, of the IOUs in defaulting credit card debt will still exist, held by someone else and circulating in the economy. My suspicion is that comparing the fate of credit card IOUs to those created for Government spending or created by Banks for mortgages and other loans may be helpful.

Sorry, but the IOUs represented by the defaulting credit card debt gave cased to exist. That is it. There is nothing more to it than that. IOUs that will not be settled cease to exist.

Very interesting data – they certainly don’t seem to fit with strong growth data and bullish stock market seen over the period.

It probably tells you more about why the Democrats lost in November than anything else.

Your last sentence is apposite.

This is what happens when you don’t address rampant inequality. The ‘economy’ may look healthy, but most people are getting poorer

I note that the ex-trader, Gary Stevenson has returned from his 4-month break. Tackling inequality is his biggest campaign ahead.

I can recommend his book, The Trading Game (out in paperback at the end of January), https://amzn.eu/d/jiMaqBh

But I can’t recommend his stance on Modern Money Theory (I don’t think he quite understands it).

https://www.youtube.com/watch?v=pgvb5GfudtE

I don’t agree with him on MMT

I watched the video. I think it a bit arrogant for him to assume he is the answer to our problems. He can undoubtedly help, but that’s all any of us can do. I found that a but off putting and took that as a warning about video making.

Stevenson would make for a great interview.

We need to do it.

Wall Street flies but people die. All makes sense.

Credit card companies lend whose #newmoney?

They are banks

The effect of credit on people’s perceptions of themselves and the world is worth some sort of research. This is because I think it has relationship with politics. Voters made to feel wealthy – even by debt – will reward systems that enable them to feel like that. As we know, money is all about confidence and feeling good.

The real crisis now though is real wages and the ability to pay down those debts. As we know, working people tend to pay down their debts or want to if they can. Working people are being put through a lot of strain on this issue currently in the West it seems because of greed.

Richard Vague (The Paradox of Debt, 2023) argues that debt enables/creates wealth but also has the capacity to destroy. He argues for improved incomes as well as better monitoring of debt especially in the private sector – also debt jubilees in certain sectors.

Whatever one might say about his suggestions, I think that we can all say that in terms of private sector debt, we have become too relaxed – the growth of derivatives that seems to be able to turn everything into a bet – cannot be ignored, and once again shows how the word ‘investment’ is so abused in banking. And when things go wrong, everyone gets the blame other than the government that presided weakly over it and the bankers who created such toxic practices in the first place and who always get their fat fees and keep them.

We obviously have system where those who create debt know that when the shit hits the fan better to be a creditor than debtor because also they will be bailed out – and only them – the debtor gets the blame. Looking over here, and the hero worship of the banking sector by Laboured I cannot see things improving either.

Trying to top and tail this post, it seems to me therefore that we have system that reinforces the desire for affluence in society but neglects the realities of money creation and destruction. Insisting on low wages but also encouraging debt is the most stupid idea going. We deserve better than that as you suggest.

Thanks

Thank you Pilgrim.

Your penultimate sentence is the perfect summary of Thatcherism and the underlying principle of successive British governments with respect to their approach to the real wealth creators – those who work.

I’m afraid that it isn’t so very different here, based on the experiences I have had during ’24 with a proportion of people I have met at work. They are the minority, thankfully, but some people in their late 50s and early 60s are hitting a debt wall with insufficient pension income to look forward to.

I know too many like that

You’re using a graph which is based on 1/4 of the data being missing to tell us to worry. Each tower in the histogram is for a period of 9 months. You have to wonder why the FT has done this, probably to fill column inches, but no-one should not use charts like this to try and inform public policy.

You ignored everything I said.

You are obviously clueless about how data is used in the real world, let alone public policy creation.

I wouldn’t bother calling again.

What was the figure I saw recently

Mortgage debt has gone from 20% to 80% of UK GDP

Last time we had a mortgage debt crisis lenders were holding off taking action on debts because it would then highlight the fact that the loans were now more than the security was worth.

We could be navigating a well known creek without a rowing implement as well

2025: It’s inequality, stupid.

When the mortgage defaults rise, then the danger of a general financial crisis is likely. As the stock market prices have risen far above the real value of shares (“productivity” is stagnant) we are in dangerous territory.

People are also terrified of a resurgence in inflation after the next administration takes office. People and companies are on a shopping spree for durables because of it. This is emptying the shelves and causing demand that was a not anticipated, so it’s a supply chain shock, which is having predictable consequences. We can add this additional financial stress to 60 to 70% of the population.

Distinct from how economists define inflation, the public defines it as stuff they can no longer afford. The inflation spike was around 8% in the US over the last few years. For the majority, wages did not keep up anywhere up to this, and this after generations of wage suppression. It explains the confusion economists have over vibeflation.

—

I saw a graph a few weeks ago on Mastodon. It compared wealth inequality in the United States to France in 1789. They look remarkably similar.

Given the response to the assassination of Brian Thomas and the utter cluelessness of the establishment, politicians media and even law-enforcement in the face of it, we’re not in a comfortable place. And the sociopathic PayPal cult that figures they’ve got a lock on controlling the US government, they’re out making it clear just what they think about the US population. Guess what? Their “retribution”, Donald Trump himself, is siding with them.

I don’t know what will happen. There isn’t an alternative figure that people can rally around and it’s certainly not the Democratic party who’s been busy purging all the progressive voices that have been dealing with economic issues.

—

I recommend to anyone who has friends or are considering an education in the United States to look elsewhere. Skip traveling to the United States. You don’t want be anywhere in this country even in the coast states over the next couple of years.

Some references would help when making claims like these.

How is money written off? “46bn written off” if someone spent that money on a CC then defaulted that money would be in circulation but is not paid back, would this be inflationary?

The debt is written off by the bank.

It is simply a case of recording that the asset of a debt owing no longer exists, with that debt now recognised as bad being treated as a cost in the income statement.

Remember money is nothing more than double entry. It is not real in that it has an existence outside a ledger.

Is this inflationary? In that money created will nit as such be repaid it could be, except for one thing and that double entry shows there is a consequence – banks have less income to distribute. That means this is redistributive, nut inflationary per se.

” banks have less income to distribute. That means this is redistributive, nut inflationary per se.”

Forgive me, Richard, but ‘banks have less income to distribute’ to whom? Are we talking of dividends and bonuses here?

As I understand it, bank income in respect of a loan consists of the interest charged on loans while the loan itself is ‘destroyed’ once repaid. Though I suppose the interest itself is likely to be a substantial sum.

I must confess that I do struggle to understand just how banking works 🙁

I do mean that there is less income for the bank distribute via dividends to its shareholders. That is the inevitable consequence of a bad debt.

Remember that we are not discussing interest here, but the capital sum that was advanced as the loan, in the main.