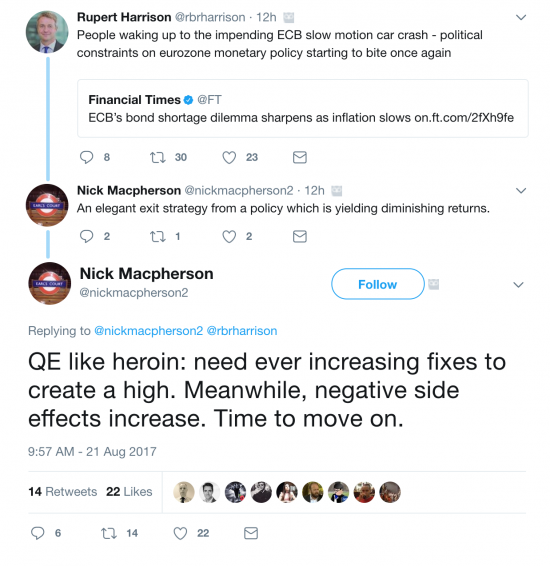

An exchange of tweets created economic headlines yesterday. This is it:

Let's put this in context: Rupert Harrison was George Osborne's Chief of Staff for most of the time he was Chancellor whilst Nick Macpherson was Permanent Secretary to the Treasury during that period. These two know each other, well. And they are disagreeing over the unwinding of QE, which I discussed yesterday.

Harrison responded to an FT tweet that in turn referred to the fact that the European Central Bank may have to stop QE soon: but that's because there just aren't enough bonds left for them to buy. Harrison clearly sees that as creating a crisis in its own right: without QE it's not clear what happens in the eurozone. Mcpherson on the other hand wants out of QE, which he says has not worked.

This is a real issue. It needs to be discussed intelligently. So let me work through this.

What was QE for?

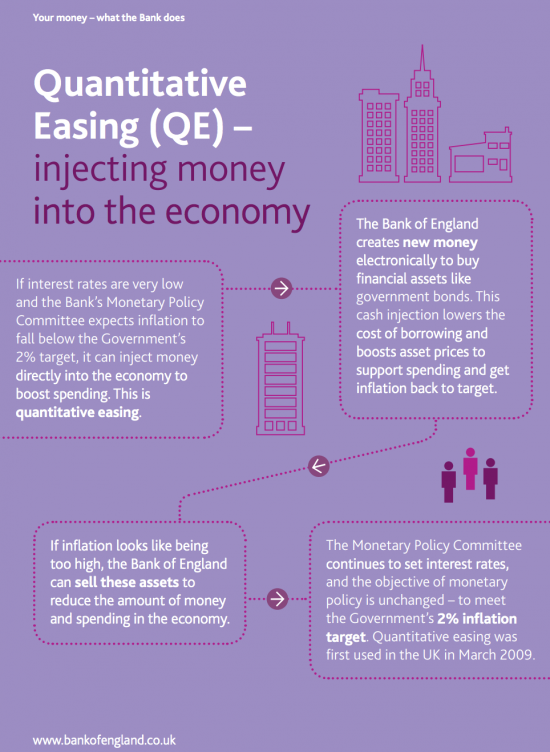

The Bank of England summarises the whole process like this:

To be a little more technical, what this means is that the Bank bought safe assets (government bonds) off those who held them. In the process they bid their price up (gilts are at record price levels as a result) with the intention of forcing their rate of return down. Around the world that's so successful that US$9 trillion of bonds trade with negative yields i.e. people pay governments to deposit money with them.

What did QE achieve?

Except, that was not what was meant to happen. Savers were meant to go to look instead for higher yielding assets to hold. But let's not ignore the fact that they did; they just bought the wrong ones. As a result Wall Street and the FTSE 100 have seen record prices. Commercial property is doing nicely. And banks in the UK, awash with QE money, lent money as fast as they could to fuel (yet another) property price boom. And when that looked like running out they just pumped money into new car leases like oil was going out of fashion instead.

The cost of borrowing was lowered as the Bank wanted, and it's stayed at record lows.

And asset prices have risen, enormously, and that has boosted very particular spending. So far so good

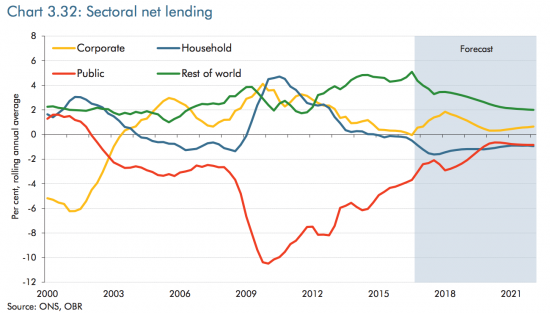

But it has not boosted investment in the real economy. As the Office for Budget Responsibility showed in March 2017, low interest rates did not persuade the business community as a whole to borrow to invest:

At this level QE simply failed. It boosted bank balance sheets. It boosted asset prices and so increased inequality whilst taking private housing out of the reach of millions more than need be the case. But because it did not boost investment, it did not increase productivity and so it did not boost wages, and as a result it did allow the personal debt crisis for those on lower pay to grow. In other words, it exaggerated but did not tackle any of the issues that so plague the UK economy.

Was QE's failure foreseeable?

I would argue that QE's failure to deliver anything much of benefit to the UK economy was entirely foreseeable, because I foresaw it. Writing with Colin Hines in 2010 I argued:

The [2009] quantitative easing programme might be considered a short term success, but as we note, the benefit has been captured almost entirely by the financial services sector whilst further asset boom and bust cycles are, at least potentially being recreated with resultant risk to the economy. These are undesirable long run outcomes when the real aim is to get the UK economy working again. For that reason we cannot support a further round of quantitative easing in the form used in 2009.

When we wrote £200 billion had been spent. Since then another £235 billion has been spent. I would argue that this was wasted money. What was needed in 2010, we argued, was green QE (and it still is). How this might work is explained here: it is very different from QE as run by the Bank of England.

I would argue in that case that Mcpherson was right; QE was a drug, and it was not helpful when better options (which it seems he did not back but of which I suspect he should have been aware) were available. In that case Mcpherson was part of the problem.

Does that mean QE should be unwound?

So far the discussion is over spilt milk: the likes of Harrison and McPherson let QE happen since Treasury consent for QE was required, and given. It may not gave worked as desired, and McPherson may regret that, but that is not the same thing as saying it should now be reversed. I very strongly suspect that QE does not unwind as readily as it was created. Before checking that let's, however, check the reasons for unwinding.

Reasons to unwind

As the Bank of England note in their our purple chart, the reason to unwind QE is that if inflation is too high the bonds held can be sold to reduce the inflationary trend in the economy.

First, let's note that there is only very limited inflation in the economy at present.

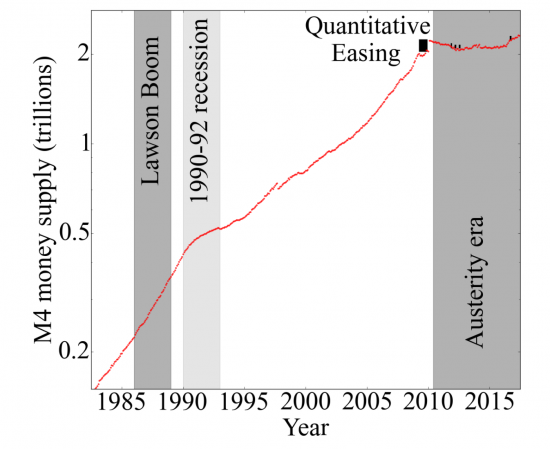

Second, let's also note that this is not because of the creation of excessive new money by the QE programme. As Charles Adams has shown at Progressive Pulse, the M4 measure of broad money in the UK (which is generally used for appraisal of monetary risk) has flatlined since 2010, contrary to all previous experience:

Far from QE creating excessive new money supplies it has, at best, managed to maintain the money supply. There is then no risk of general inflation from excessive money creation as a result of QE. But this is, according to the BoE, the only reason to unwind it. To unwind it to tackle inflation caused by other factors, such as leaving the EU with its consequent impact on the exchange rate, makes no sense at all. That would be to use the wrong tool for the wrong job.

Far from QE creating excessive new money supplies it has, at best, managed to maintain the money supply. There is then no risk of general inflation from excessive money creation as a result of QE. But this is, according to the BoE, the only reason to unwind it. To unwind it to tackle inflation caused by other factors, such as leaving the EU with its consequent impact on the exchange rate, makes no sense at all. That would be to use the wrong tool for the wrong job.

That leaves only one other reason to unwind QE, and that is normalisation; or, to put it another way, to put things back the way they were before 2007. I have already dealt with this issue. It is primarily motivated by a desire to put bankers back in charge of the bond markets, which is a power QE has destroyed. I can say that with confidence because no other coherent explanation for it has been offered.

I have heard it said that normalisation, meaning an increase in interest rates, will give the BoE the tool it needs (the potential for an interest rate cut) to tackle the next recession. It will, however, also create that recession, which makes the prescription somewhat self-fulfilling.

And it has certainly been said that this will favour savers who have suffered for too long. Except savers are, of course, the better off in society, and respectfully, the world is already tilted rather too far in their favour.

And third....actually, I am struggling for a third reason for normalisation except that it 'puts things right' and 'the way they always were'. And we should remember that the Treasury is deeply conservative (small c) and likes things to be in good order, which means that they're the way they always were, so hardly surprisingly Nick Mcpherson wants to be rid of this new fangled economic method so that old order can be restored, and nanny tucks everyone up for a snooze after lunch. You might think I am being facetious, but so lacking in innovation have central bankers and the Treasury been since the financial crisis (QE apart) and so little has their role been redefined despite the disaster they oversaw I do not think it wrong to say that nostalgia for an old order is the main intellectual driving force in the Treasury and BoE alike.

To put it another way, there is then no reason to unwind QE now apart from a desire to do so on the part of a few central bankers.

Will unwinding QE work?

On this I can be emphatic: no it won't.

Unwinding QE cannot stop an inflation it did not cause: only abandoning Brexit can do that.

Will unwinding QE cause harm?

I can be equally emphatic: yes it will.

The harm comes in a number of ways. First, QE may not have increased the amount of money in the economy but in that case it certainly stopped it declining, which was an initial objective for the policy, with the aim of preventing deflation. That worked. But with there still being no new money around reverse the policy and the money spent buying second hand QE debt will reduce liquidity: that is certain. Deflation is a real risk, and with it stagnation.

Second, as I noted yesterday, there is a shortage of government debt in the economy but that can also be met by ending austerity and running deficits or by creating bonds to fund worthwhile investment. Both have real social benefit and create jobs. Unwinding QE, on the other hand, sells secondhand paper to the financial markets and achieves no social or economic goal whatsoever, other than restoring bankers' pride and power. It is the worst possible choice.

Third, let's assume the downside of QE - asset price inflation - reverses. That would mean gilt prices would fall. As would stock markets. And house prices. All are at least possible. And note that the last two tend not to decline in orderly fashion: rout is their normal method for price adjustment. That is then followed by economic uncertainty and recession, households in negative equity and insolvency and business failure as the collateral used for lending (rightly or wrongly) disappears from the market. You can wish for all those things if you want, but please be explicit about it. I won't be joining any appeal for them. But I think that's exactly what QE reversal will create.

The risk of QE is then deflation, a negative impact on investment, asset price crashes, recession, major insolvency and, as a result, likely bank failures to be followed by a bail out, using QE. It would be ironic that those proposing this exercise cannot see that, except for the fact that it is so tragic.

Can we leave QE in place?

The short answer is, yes, of course we can. QE can just be allowed to roll. Or it could, as bonds are redeemed, be gradually allowed to unwind as reinvestment of the proceeds of redemption did not take place.

What would letting QE roll mean? Essentially it would mean that the debt was cancelled and money had been permanently created, but as noted above, that's had no inflationary effect at all and overall must then have helped the economy keep going.

The only price to doing this is it would mean admitting that the government can create money, which is anathema to bankers and hard core neoclassical economists alike, and yet is, of course, a fact. But don't expect them to concede control on this issue any time soon.

Unwinding QE is about dogma

The argument for unwinding QE will continue despite its disastrous potential because it is pursued by those with financial wealth and power who are also in possession of an anti-government dogma that refuses to believe that, in the first instance, the government can do something and, secondly, that benefit might on occasion arise from it. They let QE happen because it suited banking. But their real fear, and why they want it rolled back, come what may, is that a government that knows it can create money for social gain, using People's QE, will actually make money for that purpose and directly intervene in the economy as a result.

This is what the fight over QE is now about: it's about who has the power to control money. The bankers and their friends in the Treasury want it to be the money markets, as in times of old. And some want government to use money to advantage the people of this country. 'Normalisation' I think really means 'putting the elite back in charge'. And that's precisely why the policy is wrong, in addition to all the harm it will cause, to which those proposing it are indifferent.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

There are links to this blog's glossary in the above post that explain technical terms used in it. Follow them for more explanations.

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Buy me a coffee!

Buy me a coffee!

“Normalisation”!! Wow, now there’s a term with powerful connotations for me, as the husband of a Czech refugee/émigrée.

For “normalisation” is the name given to the process of unwinding the democratic gains and liberalisation of the “Prague Spring”, to return Czechoslovakia to its pre-Dubcek state of Stalinist oppression and social fossilisation.

Hard to tell the difference really then, isn’t it? Like the ending of “Animal Farm” – looking from bankers to Stalinist nomenklatura and back again, it was impossible to tell the difference, as they were both elites, and more like each other, than those they purported to represent.

That is really rather too close for comfort

‘Totally agree with you on this. It needs to be said.

There should be more QE but this time more tightly aimed at benefitting the woman and man in the street (green QE etc.,).

Bu as we have seen with the electrification of the North of the UK, there seems to be no desire to invest in anything by this bunch of anti-government people who are in Government!

“the power to control money. The bankers and their friends in the Treasury want it to be the money markets,”.

Purposely ceding control of the country’s sovereign currency is bodering on, if not actually, treachery. And this would also be after the knowledge of the events of the first world war:

https://bankunderground.co.uk/2017/08/08/your-country-needs-funds-the-extraordinary-story-of-britains-early-efforts-to-finance-the-first-world-war/

Yet we’re still told we’re cannot do without ‘the City’.

Your last paragraph sums up the situation precisely . It would be comical if it weren’t so tragic ; here are all these supposedly expert, brainy people being paid handsomely for giving advice when the advice they are giving is one hundred per cent wrong . The issue though is political and at this moment the alternative voice is, for most people, hard to hear because they have been led to believe for so long that money is a ‘ thing ‘ and things are tangible and come from somewhere, are constructed with great labour and thus to make the leap to understand and believe that money ( of all things ! ) is made up out of nothing is a very bitter pill to swallow. I know this having laboured away at trying to explain it to educated , clever people . They just don’t want to believe it. But I don’t want to end on a note of despair because we have to keep on keeping on and hope and trust that the truth will emerge .

Thanks

Can anything be learned from an interchange of tweets? Two people bursting with their own self importance pretending that they know what they are talking about.

Yes, I know Macpherson was the head honcho of the Treasury, but anyone who has been the recipient of Dear Accounting Office letters will not set much store by that.

The BoE slide states that the purpose of QE was to boost spending. If I wanted to boost spending would I rely upon the most abstruse method of doing so at my disposal? Spending is increased by replacing one debit (gilts) with another (cash) on the assumption that the QE recipient will invest in something else, which will then stimulate spending. Come on, banks could divest themselves of gilts (convert gilts into cash) at any time they wished.

If more than 90% of money within the economy is created by bank lending why would the above create demand from potential borrowers?

Nothing about QE as explained by the BofE makes any sense to me and therefore I suspect a hidden motive.

If this was the only instrument available to me I would be on to the Chancellor insisting that we should create money to directly stimulate growth /demand.

As gilts are repurchased the residual quantity available for purchase on the market shrinks, this is bad news for such entities as charities, entities that need a safe investment bedrock with a reasonable income return.

Unless you believe in the existence of a fixed quantity of money circulating at the speed of light there has to be a direct link between GDP growth and the quantity of money in an economy, so if the quantity of money is flat-lining then so is the economy. QE has not increased demand and therefore has not increased the quantity of money in the economy.

This article from New Statesman by David Graeber makes similar points albeit from a different starting point…

http://www.newstatesman.com/politics/economy/2017/08/were-racing-towards-another-private-debt-crisis-so-why-did-no-one-see-it

Maybe enough folk are beginning to see through the midden of neoliberalism…

He and I use the same source for the same purpose

I like it….

After from here and a few other voices of sanity on the internet, the terrible state of affairs is that very few people seem to understand what is going on and the general level of reporting on this issue is making matters worse. May I suggest that Macpherson should post some data to support his tweets next time, and then there is Larry Elliot in the Guardian whose piece has the title:

“Quantitative easing is a costly habit we should have kicked long ago”

https://www.theguardian.com/business/2017/aug/21/quantitative-easing-lord-macpherson-qe

I may agree it that it has been ineffective, but costly it is not, it actually saves money by lowering interest payments. Of course there are questions about asset inflation but I think this is another issue and could have been stopped if the right fiscal (tax) policy had been followed. But then it gets worse he says:

“The best that can be said for QE is that it helped prevent an even deeper slump in the winter of 2008-09.”

QE started with a slow taper in March 2009 – a problem with causality here!

Not one of Larry’s best….

I confess I shared the view

I think that Larry E wrote that one in a bit of a rush – maybe he was going on holiday? The problem is that his article has just created more confusion in my view.

I say this because at the next meeting of the local progressive group I am part of I want to try to nail an economic point of view so that the group can put forward better ideas in a cogent way when discussing alternative ideas with the voter at the next election.

Those economic ideas are going to be sourced from this blog and the writings thereof of its founder (that is if I can get them to understand/take them on). I know that we as a group do not like austerity – but there also has to be credible alternative. And tax is only part of it.

Sorry I meant Apart from here…..

Why won’t you wish for a collapse of house prices? As a first time buyer I would welcome a 20-30% reduction. Then I could afford a house big enough for my family without the worry of interest rate rises and crippling debt repayments in the future.

I would love for a fall

Except that millions of households would be bankrupted, and banks would collapse with them