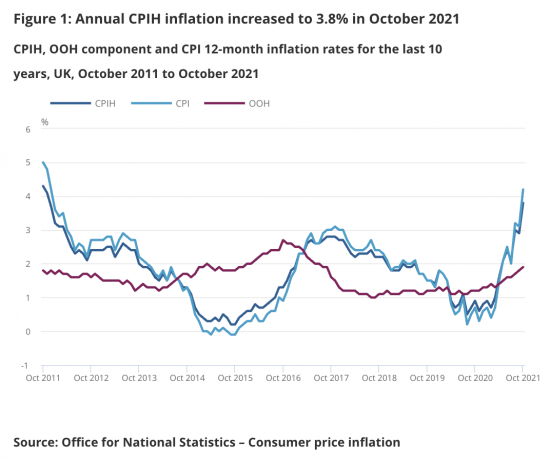

The Office for National Statistics has issued its inflation figures for October and to absolutely no one's surprise they are up:

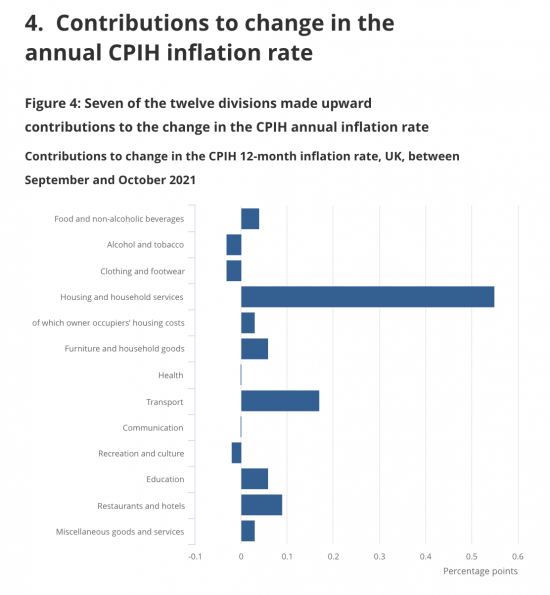

These are said to be the main causes:

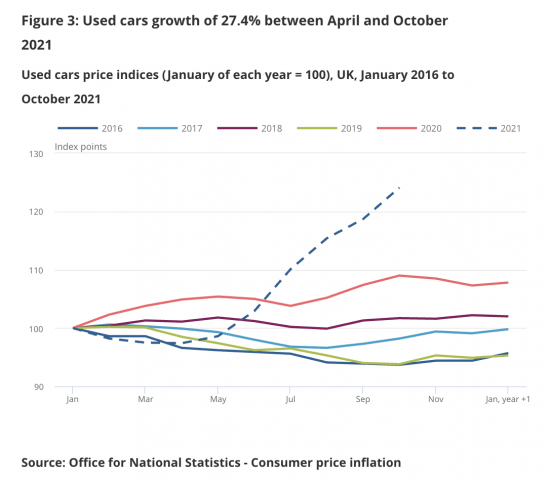

Housing and household services is up because of gas and electricity prices. Transport is up because of fuel prices and the increasing costs of second-hand cars.

The rest amounts to not a lot of consequence.

But although all that an interest rate rise can do is add to the pressure on already tight household budgets, where heating bills will have to be paid, the Bank of England is bound to see this as a reason to increase interest rates.

That rate change will not change the price or supply of gas, electricity or second-hand cars. All it will do is make the lives of many already struggling that much harder. An interest rate rise would be an act of economic masochism willingly committed on the hardest up by a group secure in the knowledge that their own well-being will not be impacted by the decision. I call that unforgivable.

The time for the sham independence of the Bank of England to come to an end has arrived.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Interest rates are a blunt instrument.

A rise will squeeze those households with debt and mean they spend less on other things leaving businesses that rely on their custom to cut prices to compete for a smaller spending pool.

A rise will postpone investment decisions.

So, let’s be clear – a rate rise will push some people into poverty, will send some businesses to the wall, will damage our economy’s longer term prospects. That’s a fact. That is how interest rates work and always have worked.

So, if one wishes to advocate a rate rise you should be certain (a) that the problem really exists and (b) that a rate rise will do some good. In the topsy-turvy post (??) COVID world can we really be sure? I don’t think so.

However, there is a dilemma. Ultra low rates have been driving up asset prices (houses etc.) and that is a problem. In some sense “rates are too low but we should not raise them”. We are in this situation because the prevailing wisdom of neo-liberals over the last 40 years was to use a single variable (interest rates) to control inflation and let the market resolve everything else. It is (and was) nonsense. There are other tools available to intervene more precisely in the economy to support “good” things and discourage “bad” things. In the monetary field it is things like credit controls, differential lending rates etc. but the real place where things should be encouraged/discouraged is with fiscal policy. This government’s drive to return to austerity and an opposition that fails to challenge this neo-liberal orthodoxy is the REAL problem, the BoE is just “extra” in this B movie horror show.

Agreed

Those things, plus active tax policy, of course

It looks to me as if we’ve been blindsided here.

At first there was a climb down and now we’re back where we started.

It shows us that the corrupt system that we have relies on people who are paid to say and do the most ridiculous things and Andrew Bailey is a shining example of such a glove puppet.

Fighting inflation with another form of inflation. Are you serious? Rhubarb!