I made a television recording yesterday on the role of the Big 4 firms of accountants. I am doing another later this week. Since one will be broadcast in Italy and the other in France most readers of this blog will not see them. But what it shows is that the world is noticing that there is an audit crisis, and that the UK is at its epicentre.

My approach yesterday was calm, reasoned, and careful. I am, after all, a chartered accountant. And I did, after all, train with what is now KPMG. I have an interest in this issue. And a risk of bias: I believe accountancy and audit can both be of enormous value to society.

I explained why in the interview, saying that if capitalism is to continue to play a role in the mixed economy that has been the basis for our prosperity for what is now most living memory then it is essential that what companies do be accountable, and that auditors must ensure that the data that they supply to investors and stakeholders is genuinely true and fair and genuinely seeks to meet the needs of those users.

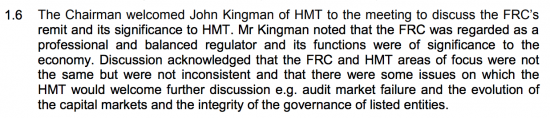

It was in this context that I said independence is key. That is why it is so worrying that Sir John Kingman who is to head the review of the FRC comes with baggage attached. This comes from an FRC minute from September 2013:

Is less than five years long enough to have acquired a more objective view? I don't know. It does not help the review that this evidence of past association and opinion exists, most especially when one of the key issues for the review is whether the link between auditing and other commercial activity are also too close: an issue I discussed in my interview.

But there are other reasons for concern, which this minute hints at, if only by not mentioning them. The crisis of auditing is largely about the role of the Big 4 and their failings. It is not about other auditors. But the crisis in accounting (because let's be clear, that also exists: it is still not at all clear that the FRC truly understands what 'true and fair' means in UK law, or applies it properly) is much broader, relating not just to how IFRS applies to large companies and how that is interpreted in this country, but also to the new accounting demands now being imposed on smaller companies in the UK that appear to me to be almost wholly unsuited to their needs and that of their stakeholders, investors and management, few of whom will undertsand some of the new requirements meaning that the resulting data could be detrimental to them. The minute noted above does not refer to any of these issues: it's their absence that is telling.

I want the FRC review to look at auditing, and the Big 4's role.

I want it to look at the application of IFRS to the UK and the FRC's role in that issue.

But it has to go much broader than that. Good accounting is at the heart of a prosperous economy. It cannot make prosperity, but it can most certainly sustain it. Just as it can also sustain tax bases. And help hold governments to account. And these things matter. But they are not, it seems to me, at the core of what the FRC is all about when that should be as much their concern as making sure the Big 4 work, vital as that is.

There is a role for a strong auditing and accounting regulator in the UK. The structure of that regulator is rightly in question. But let's not pretend for a moment that this is just about big business. This is also about ensuring all business gets the data it needs to understand the operation of enterprises when they may only have accounts once a year. There is little sign that the FRC gets that at present. Nor do they understand that it is vital that small business accounts be public documents. And that their quality does need to be regulated, even when not produced by accountants, or we end up with a degradation in business data and so confidence that will impose a massive cost on smaller businesses who already find access to capital an issue of real concern.

Let's review the FRC, for sure.

But let's make that an objective review.

And that means looking at the whole scope of its work, actual and potential, and not just the bits that have caught the headlines: the malaise goes much deeper than that.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

“My approach yesterday was calm, reasoned, and careful.”

I’m glad to hear it. Screaming and shouting and stamping your feet would have been infantile, even though it must be tempting.

Good to know your Chartered Accountant training is securely embedded.

Perhaps when you feel like a third age career change you might be an anger management practitioner. (?)

🙂