On Thursday night Frances Coppola and I walked through Bloomsbury to Kings Cross / St Pancras following an event on modern monetary theory at which I spoke and she attended, and where I made sure she got a chance to ask her question. I thought we had a good and useful conversation. I tweeted to thank her for it.

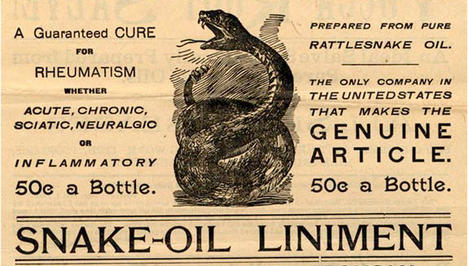

And then yesterday she published a blog by someone called Paddy Carter in which People's Quantitative Easing was described as 'snake oil'. For the sake of doubt the blog title (Frances' work, no doubt) was 'Monetary Snake Oil' and the image that accompanied it, again, no doubt Frances' work, was:

I think we can be pretty sure that Frances was not publishing opinion with which she differed. So let's for a moment remind ourselves what snake oil is:

Snake oil is an expression that originally referred to fraudulent health products or unproven medicine but has come to refer to any product with questionable or unverifiable quality or benefit.

And so:

By extension, a snake oil salesman is someone who knowingly sells fraudulent goods or who is themselves a fraud, quack, charlatan, or the like.

I think the intimation is pretty clear.

I have to admit that I'd have thought Frances might have raised the subject, and her intention to publish such a description of work intimately connected to me when she had the chance to do so on Thursday. She didn't. But if there is something I have learned from Jeremy Corbyn over the last few weeks it is 'don't do personal'. So I'll be letting the libel pass by. Which Paddy Carter might like to note too.

Who is he? I first came across him when he commented on this blog, supporting Chris Giles' view that tax is extortion. I now note that he is, according to his biography (linked from the Coppola blog) a development economist specialising in tax for the Overseas Development Institute. Now tax and development is something I know about. I have a track record there, and some (I went over-egg it) small record of promoting change. I have never heard of a Paddy Carter. And the ODI's contribution would be best described as an opportunity lost, but Paddy clearly feels PQE is his thing because, as he says of himself:

Paddy Carter is really a development economist but has been brainwashed by years of teaching undergraduate macroeconomics and absorbing more by osmosis, briefly having had an office down the hall from Tony Yates.

To contextualise: he is then a man who has taught the basics of macroeconomics under the influence of a man who left the Bank of England some time ago and who now thinks he is the spokesperson for 'the Bank view' of PQE, to whom it has provided an opportunity for comment the likes of which he has never enjoyed before. I think we get the drift: Paddy's a man who, like Prof Tony Yates, appears unable to appreciate that there might be a need for new fiscal tools to deal with the next economic crisis given that all the monetary ones we now have available have failed. That's the necessary starting point to contextualise discussion, but let's at least welcome a new voice to debate. There are few enough of them.

So let's now look at the economics on offer from Paddy. In doing so I can't help but start with a quote from a Danny Blanchflower paper from 2012 in which he in turn quoted Oliver Blanchard's 2008 description of the standard macroeconomist' approach to an issue (Blanchard is now chief economist at the IMF):

A macroeconomic article today often follows strict, haiku-like, rules: It starts from a general equilibrium structure, in which individuals maximize the expected present value of utility, firms maximize their value, and markets clear. Then, it introduces a twist, be it an imperfection or the closing of a particular set of markets, and works out the general equilibrium implications. It then performs a numerical simulation, based on calibration, showing that the model performs well. It ends with a welfare assessment.

And that is, almost exactly, what Paddy Carter does. I will come back to all his other assumptions in a minute. What is most telling to me about Carter's whole approach is that is his whole criticism of PQE is based on the logic of this paragraph:

And here's why People's QE (PQE) is snake oil. So long as the BoE is still targeting inflation, it will still be pushing and pulling money in and out of the system, as required to meet demand for money at the interest rate it has set. If the BoE is still targeting inflation, then whatever money PQE puts into the economy on one hand, the BoE is going to be taking out with the other. Or, if the BoE happens not to take the money out, that implies it would have been putting it in, anyway. And that means that over the long run the rate of seignorage, or the extent to which the government is able to spend without borrowing, is not affected by PQE.

For the sake of doubt, let me deconstruct that. What Paddy Carter is assuming is that at the moment PQE is introduced the economy is in equilibrium (the first Blanchard condition). In other words, Carter assumes PQE would be introduced into what he thinks is an already perfect world - because that's what he has apparently taught piles of students is what exists in the macroeconomic world. The consequence is that he assumes that the only need the Bank of England would have if PQE was introduced would be to immediately cancel the consequence of it because the world was perfect before PQE happened. This is the fulfilment of the second Blanchard condition: introducing PQE is to create an imperfection in an already perfect world. And the third Blanchard condition requires that the imperfection must be addressed, which is why the impact of the PQE funding must be cancelled by pulling it out of the economy as fast as possible in Carter's opinion by selling bonds. And then in the final sentence we get the fourth and fifth Blanchard conditions combined: there is no impact on ability to spend without borrowing as a consequence and so no net welfare change, it is claimed.

Give Paddy Carter his due: he'd get a good 2:1 for that on any course he taught. He's followed the rules of the great and good of macro really rather well and as a result to his own satisfaction, and no doubt that of Prof Yates, proved his case beyond all reasonable doubt.

And now let's explore why that is total nonsense.

First, we are not in a state of general equilibrium. We are very far from it. We have (to list just a few of the reasons why this assumption is not true):

- Unemployment

- Low productivity

- Limited investment by business

- A chromic shortage of necessary social infrastructure like affordable housing

- A market unable to price minor issues like climate change and the funding needed as a consequence

- An impending exogenous shock in the form of China

Second, we do not have inflation and are likely to have deflation.

Third, monetary policy has not worked for more than six years because we are at the lower bound of interest rates and there is little sign that is going to change.

Fourth, the money supply has been falling for several years although we have had growth in GDP.

So, in summary, we have unmet need in the economy (for investment) and the resources available to meet that need (under- and unemployed people plus spare business capacity) but we have no mechanism to match them despite deflation looming and a likely decline of export markets on the horizon. And in response to this Paddy Carter says:

In theory PQE is entirely unnecessary

Well on your logic Paddy, I agree.

But in the real world where none of your assumptions hold true and those I note do then we definitely do need it.

In fairness I should add Carter then said:

and governments can finance investment during downturns by borrowing when rates are low

And actually, we do, in theory, have a point of agreement there. But let's be clear why theory fails again. First, Carter (and Yates et al) have apparently not noticed the austerity and anti-debt narratives to which they, no doubt subscribe. These mean that whatever the theory the political reality is that issuing bonds is politically hard to sell right now, precisely because conventional macroeconomists have worked hard to feed that cause.

Second, this ignores the fact that right now PQE is significantly cheaper in interest terms than gilts, and I think it will remain that way for some time.

Third, not selling gilts breaks the narrative of the importance of the bond markets: something that has to be done once and for all.

Fourth, the potential that PQE provides to sell a positive narrative of investment is wholly ignored. These things matter in the political economy, where I think.

And finally, because of the real world conditions I note PQE will not need to be withdrawn by bond funding (or taxation: Carter has not noticed the impact is the same) because:

- The money supply is needed

- There will be growth without beating inflation targets, and

- Unemployment will reduce, yielding net tax flows that do actually, although (I stress) not necessarily, at least partially and potentially also more than cancel the PQE injection in any event. Carter has forgotten the wonders of the multiplier.

So, let's summarise this. First, Carter's macroeconomics is a proof existing solely in its own fantasy world that in turn exists solely in his imagination and that of his fellow so-inclined macroeconomists.

Second, in the real world the conditions for PQE exist.

And third, the reason why that is the case is a) cost b) the need to reframe the narrative and c) technical feasibility.

So why, in that case, would the central bank want to neutralise the money injected by PQE? It would do so only if it wished to undermine the will of economic policy of the democratic government. We got rid of the House of Lords to do that more than a century ago. The time has come to make quite clear that a central bank cannot now play the role of blocking democracy that constitutional reform supposedly ended in 1911.

But let's step back to the economics for a minute. In the light of all this who is selling snake oil? Not me: of that I am quite sure.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Seems to me the fundamental objection to PQE is that QE purchased gilts already in circulation. PQE creates new money — so I presume the problem there is that it might be considered inflationary. Quite why that is a current danger I cannot see.

To my suggestion that if that were a problem then in order to counteract it, a few less gilts could be issued instead, Frances Coppola replied “The Bank would sell the same value of gilts as the NIB bonds purchased, leaving both the monetary AND fiscal positions flat. Such a neutralised (“sterilised”) PQE operation would thus simply exchange regular gilts for NIB bonds. It is not clear to me that this is in any way beneficial to the economy. Indeed it is not clear to me why it would have any net effect at all.”

So the opposition is worried about the money supply as if it were some force of nature.

I doubt those who obsess about it are unemployed or paying sky high rents. PQE supporters think the economy should work for everyone rather than the other way round. (In some ways it is a problem that PQE, in only tweaking the system, is not radical enough.) But in order not to frighten too many of the horses and with politics being the art of the possible, it has to be a very good start.

A wholesome put down! Interesting article from the Telegraph stating only corbynomics can save China:

http://www.telegraph.co.uk/finance/economics/11831426/Citigroup-braces-for-world-recession-calls-for-Corbynomics-QE-in-China.html

Paul Gambles @PaulGambles2 cites Buiter [Citigroup chief economist] as mad and the”Torygraph” as facile but just because someone is mad doesn’t necessarily mean they have verbal diarrhoea!

Thanks

Looking now….

Richard,

Since when do I have to post on my site only things of which you approve? Or obtain your agreement before posting them?

Coppola Comment has hosted guest posts by a number of people, actually, which if you read it regularly you would know. With reference to this blogpost, I thought the points Paddy made deserved a hearing and therefore agreed to post his piece. The title was his, not mine.

I am sure Paddy can defend his own arguments and I look forward to the discussion between you. However, I have on many occasions made my own views on “PQE” clear, not least in the FT last week and in conversation with you on Twitter. I regard it as a distraction from the real issue, which is the over-tight fiscal stance that is sucking all demand out of economies across Europe. I’ve made my opposition to that abundantly clear on many, many occasions.

I have openly supported the need for much greater fiscal investment and the creation of some kind of public development bank or sovereign wealth fund. In fact I have gone further than you, since I argued that the investment bank or fund could take equity stakes in businesses, especially the young innovative companies and start-ups that are the future of this country. I see absolutely no need for the Bank of England to buy the bonds issued by such a body, except as part of a monetary easing programme justified by economic conditions. I consider that there is more than sufficient demand for safe savings vehicles from UK residents, and the interest paid to them on those bonds would itself constitute monetary stimulus in addition to the fiscal stimulus from the investment projects. I therefore consider PQE unnecessary.

If the government compelled the Bank of England to buy NIB bonds, but continued to hold it accountable for meeting the inflation target, then the Bank of England would have to counter any tendency for PQE purchases to raise inflation above target. It would therefore have to offset NIB purchases with gilt sales. This is the “push-and-pull'” to which Paddy referred. Of course inflation is some distance below target at the moment, so there might be some justification for NIB purchases on those grounds. But that would simply be converntional QE similar to the Fed’s purchases of agency MBS. As such, it would be neither new nor innovative and the BoE would happily do it now if it saw the need (and we had an NIB). At present, however, the BoE does not see the need for further large-scale asset purchases. If you think it is wrong, you need to make the case for further asset purchases to the members of the MPC.

You have said you believe there will be a recession by 2020, and that therefore BoE purchases of NIB bonds would be appropriate at that time simply as monetary policy. You may be right. But I do not think the investment the country needs should be dependent on there being a recession. I said that in a blogpost I wrote last week. You don’t seem to have read it.

For the record, both Paddy and Tony have said they consider the fiscal stance substantially too tight. You are therefore wrong and unfair to say that they “no doubt” subscribe to the anti-debt and deficit hysteria promoted by the government and various media outlets. It’s very clear that they don’t. In fact I would say that the consensus among mainstream economists now is that austerity does not work, far too much has been expected of monetary policy and a much looser fiscal stance is needed in Weatern economies.

I agree that the big problem is political: Osborne has done all too good a job of convincing voters that fiscal austerity is good for them. Indeed, that message is being spread by politicians all over Europe, to the detriment not only of people in Europ but, now, people from elsewhere too. Europe’s inhuman response to refugees is principally caused by slavish adherence to fiscal deficit and debt rules. Why don’t you say this? I did, yesterday.

But I cannot in conscience subscribe to a policy of using what amounts to financial engineering to avoid challenging the poisonous message being spread by politicians and media about fiscal deficits and debt. There I stand. I can do no other.

Frances

Of course you need not agree with me. I never asked you to do so and never will. But libel is something else, and that is what you did

And you can’t defend your self by saying it was only Paddy’s view: the convention in that case is to make that clear and you did not

I think your comments demean you. I suspect your readers will as well. An apology might restore their good faith

As for the arguments: I note you have not defended Paddy. So much for you think it worth publishing the view.

For the rest, including the FT, you by and large agree with me except on bonds. I have been suggesting the NIB could be the core of a wealth fund. I have been suggesting variations on this theme since 2003. All are on the blog this week. I have not denied the attraction to savers: I would make these bonds available to them. I said so this week. I have also made it clear I would want such funds to be invested in technology and SME companies driving it: so has Jeremy Corbyn.

You have said nothing original there or which adds to what I have said for many years.

So let’s get the rest clear. First, I would have thought it obvious if I did not believe in BoE independence that I did not also believe in the primacy of inflation as an economic target, but maybe I am guilty of not having spelt this out sufficiently: I would do so, and soon.

Second, despite the fact that you say that people want to secure saving mechanism of gilts provided no suggestion as to how this might be achieved: the least I have had the decency to do so in the form of the Peoples Pension Fund. This I have explicitly linked to the National Investment Bank. I see no incompatibility in doing so.

Third, your logic that any excess of funding pumped into the economy by the purchase of bonds issued by the The National Investment Bank must be cancelled through gilts is really rather odd. The cancellation could also be through taxation, and if the taxes in question were, for example, redistributive to ensure that greater equality was achieved and multiplier impacts were maximised by delivering to those with greatest need then that would be so much more useful than gilts. But you ignore that, and I have no clue why: I presume you think tax is there to raise revenue when that is glaringly obviously not true when governments can print money (as you obviously agree).

Fourth, this is precisely why the BoE cannot make these decisions, but I know you have already agreed the BoE independence is a sham so I am not sure why you cannot conceded on this issue.

Fifth, you ignore the cost issue, although that seems bizarre.

And last, on Thursday evening you were telling me all your fears about the ownership of UK gilts: indeed, you said your thought foreigners should be banned from buying them. So, like me you think bond markets should have reduced influence. And I am making sure that is possible, at lowest possible cost but you do not like it.

If I could find any logic to support your libel it would help. But right now I can’t. I am openly promoting more accountable use of deficits for the national good. I wish you were too, but I can only see a person beholden to the bond markets who has no explanation as to how we might access them, which pouts you into the same fantasy space as Paddy Carter.

And if you want to continue the debate, apologies for accusing me of being something I am very obviously not don’t cost much, and will be readily accepted

Richard

I have not “libelled” you, Richard. Indeed, I could argue that since you have not corrected your wrong statements about me in this post, you have libelled me. I have already told you that the title of the post was not mine. Please correct your statement.

I do not think it appropriate to apologise for posting something on my own blogsite of which you do not approve. The purpose of that post was to spark debate, and it has succeeded in doing that. I do not think contrarian voices should be silenced and I am more than happy to give them a voice. In days gone by, Paddy’s post would have been put up at Pieria, not on my own site. But that is no longer an option for me, for reasons that I’m not prepared to discuss.

Frankly it would be more gracious of you to engage in the debate than throw brickbats here.

It is depressingly evident that you have read very little of my work. In particular, you clearly know nothing of my writing on the relationship between fiscal and monetary policy. For example, I have written many pieces discussing the role of taxation as a monetary drain and the equivalence of taxes and interest rates. I have also written many times about the importance of safe assets and the responsibility of government to provide them, not for bond markets but for its citizens. Yet you accuse me of regarding taxation as “funding government” and you say I am “beholden to the bond markets”. If you were familiar with my work, you would not make such mistaken remarks.

You also seem to know nothing of my work in relation to safe savings vehicles, both liquid savings and pensions. I find your accusation that I have not “had the decency” to make any proposals along this line surprising, considering that I told you on Thursday that I had discussed some ideas with the Treasury two years ago and was pleased that they had actually done some of the things I suggested.

I ignore the cost issue because for a monetarily sovereign government it is not relevant. If government issues bonds only to its own citizens, it can pay interest on those bonds at far above market rates, since this is merely money that will be spent into the economy either now or in the future. You can regard it as tax credits or basic income, if you like. Whatever. It is monetary stimulus. There is absolutely no reason to artificially depress interest rates on bonds sold only to UK residents. To suggest that “cost” is an issue implies that government is not monetarily sovereign. It’s not me who is beholden to the bond markets.

My comment about excess funding being mopped up by gilt sales was in response to a comment on Paddy’s post. The commenter suggested that gilts could be used to neutralise the monetary effects of PQE. In response, I outlined two possible uses of gilts for that purpose. The commenter has quoted me above out of context.

Some of the language you have used both in the above post and in your reply to my comment is beneath you.

Dear Frances

Thank you for commenting

I note that your sole purpose in doing so appears to be to throw more abuse: as a matter of fact you did publish an article that was intended to be deeply offensive, and succeeded in being so, whilst also being absurdly wrong.

You have now responded using the same type of argument that Paddy Carter used: for example I note your defence of the interest cost argument is based on the assumption that no one from outside the UK owns gilts when we know that a significant proportion of gilts are, in fact, owned abroad. If you wish to argue on the basis of your fantasies feel free to do so, but please don’t ask me to read whatever you write if that’s your basis for comment.

What this does imply to me is that, as one person who wrote to me about your post said, you are “not arguing in good faith”.

I have, of course, held this view before: for a long time you happily joined in trolling abuse with the likes of Tim Worstall and I broke off any engagement with you precisely because it appeared you wished to play in that gutter. Your pulled yourself out of it, I thought, and so I tried again. I now see that was a waste of time.

I extended the courtesy of a fully developed argument in response to your abuse: you have just replied with more offence. I long ago realised that argument on this basis is a complete distraction. As I said: I have no desire to do personal, and since it seems you won’t debate I draw matters to a halt here, happy that you have had your chance to comment and have had nothing to say.

In disappointment

Richard

You nailed it. CBs routinely undermine the welfare of the nation. Orthodox economists are trained to be the pawns of banksters everywhere. Trade flows are driven by income not prices, a system of private money is an inherently deflationary system where price reductions must necessarily follow from the income reduction that interest and austerity provide. However the asset inflation is what allows banks to transform price into money. The extreme Venezuela example is given in order to scare people but one must also look to the extreme Greek example, where the greeks are forced to barter because their monetary system has been completely and willfully mismanaged by the very serious people. PQE is the trillion dollar coin http://neweconomicperspectives.org/tag/trillion-dollar-coin both scare the Establishment.

What the less radical Coppola* should be explicit about is that the captains of industry are not lions but kittens, so PQE is a shot that needs not be fired. *the faux outrage with the migrants issue and the snake oil stuff ought to bring her kudos from the VSPs

Richard

I think you do mainstream macro a bit of a disservice which has become heterodox (cf De Graewe Sapir Pisani among others) Yates et Al are narrow sophists who Coppola want to join the ranks of the no longer great or good as a classic wannaber which is why I no longer follow her on Twitter. Seems to me PQE is a superior form of fiscal activism why FED ECB and BoE are using it without daring to speak it’s name.PCB ha no such problem

Leslie

Leslie

You are right: PQE is fiscal activism

And Frances does, indeed, appear to want to be one fo the conventional great and good

Best

Richard

Somebody really should tell this Carter guy to read Voltaire’s Candide, because he, and the whole macroeconomic perfect equilibrium thing REALLY does sound Panglossian.

You remember “All is for the best in this, the best of all possible worlds” bleats Dr. Pangloss continually, as he experiences one disaster and mutilation after another. But he expires with a smile on his face, poor fool!

Isn’t he just saying PQE is incompatible with existing monetary policy of targeting a particular inflation rate. Ie. because PQE is inflationary the BoE would automatically counteract its effects. That’s why he says ‘so long as the BoE is still targeting inflation’.

I will address this…

You are right Richard. I think there is clearly jealously from mainstream economists when it comes to considering your Corbynomics work. Unlike you they cannot see beyound their neoliberal noses. Some of them have spent their entire working lives studying economics and some do it as a full-time job. Unfortunately, they see you as a provincial high street chartered accountant. They should know better. Accountancy deals with money and you’ve been an accountant for years. Therefore, you understand economics because that involves money.

We have a Chancellor who has not worked in the real economy

We have an economics profession who has never been near it

And I have been

And apparently I don’t know about it

All very odd, isn’t it?

Totally agree, Richard. Unlike some you have worked in the real world. Your PQE was developed because you are QBE in economics.

I think there is a good bit of intellectual dishonesty surrounding the economics fraternity’s reaction to PQE.

Let me make some observations on this

1. The substance of economic complaint about PQE is rather thin, in fact most of the objection appears to be political, institutional and sociological. Many such as Wren Lewis accept there is a need for macroeconomic stimulus and room for exploring more innovative forms of QE (see helicopter money). They also accept that the UK has a productivity and infrastructure deficit, and there is a place for a public investment bank to target that. Their complaint is that PQE is not needed to fund an investment bank and it could be financed through conventional government borrowing because it is so cheap at the moment (Carter touches on this too). Your point is that it is even cheaper to do it through PQE. I am not sure how much would be in it, and to be honest it’s not a terribly interesting debate. The objection is that proposing PQE as a means of financing an investment bank is caving into deficit fetishism by not borrowing, but that ignores that all of this is about changing that dominance of that narrative politically and there are signs that this is already happening. That leaves you with an objection that this is unnecessarily unconventional and nobody could be sure what the long term consequences and implications are, so better to play safe and go for the conventional borrowing option. Its all bit speculative and unconvincing as a critique at the moment.

2. The second substantive complaint is that this will destroy central bank independence. There is a general notion that you shouldn’t touch the current inflation targeting regime because of the anti-inflationary credibility it has generated — a sacred cow. But as a guide for policy the current target has been redundant for getting on for EIGHT years now, – that’s not 2 or 3 years, it’s the best part of a decade. Maybe that is telling you that what might have made some sense in 1997, makes less sense 18 years after a financial crash of historical proportions. But on no account must you open the central bank independence box because that debate has been settled — the current regime works. Even with mounting contrary evidence you should not have a constructive debate about appropriate central bank institutional design. And of course under Mr Carney, the BoE has not always appeared terribly independent in any event.

3. Privately many economists indicate that they think that PQE is not a completely terrible idea. (I’ve heard and seen them doing this). It has some merits, there maybe something to it, it would need a lot of refining, and of course its heavily macroeconomic context dependent. Show me a policy proposal that isn’t. Publicly however there is a dismissive sniffy-ness to the response that is quite unedifying. There are three possible reasons for this. A) The political label of far left attached to Corbyn means if you are a leading talented professional academic economist you can’t be seen to be associated with that label, because such an association would be damaging for your professional esteem with your peers (see the Observer letter we are not Corbyn supporters but); B) the proposal has come from a non- Ph.D economist, who is primarily a campaigner, rather than a professional academic economist and so lacks credibility and should be dismissed; C) it is difficult enough to get public and political space for ideas that advocate government funded investment on infrastructure and varieties of macroeconomic stimulus, that you could do without others queering your pitch and muddying the waters, with different if similar ideas.

I will leave readers to work out what is going on. There is a lot of huff and puff, but the critiques thus far lack economic substance and in my view there is quite a bit of unsavoury intellectual dishonesty and professional snooty-ness surrounding this. I’m afraid this is only start of mobilization against the idea and against anyone associated with Mr Corbyn.

I fear you may be right

I think a little waking up to the smell of coffee is needed

And, of course, I am open to refinement. It would bizarre to think it did not need it

Having read more on the PQE topic and more comments on it over the past few weeks, on this blog and elsewhere, than on any other single topic that I can remember I have to say I think APB’s analysis hits the nail right on the head, Richard. But I don’t see the three possible reasons (A, B, C) as necessarily either/or – in many ‘critiques” I’ve seen, and particularly in the press, they all seem evident to some degree or another even if only implied. So it would seem your call for “fiscal activism” as Leslie Budd accurately refers to PQE has upset an awful lot of people and will undoubtedly continue to do so after (if) Corbyn becomes leader of the Labour Party. I know you’re prepared for that, and many other commentators on here have alerted you to that threat, but it will be unrelenting, that’s for sure.

In closing I’d just like to add that I think you’re absolutely justified in the anger that clearly underscores this blog. If someone I knew or considered an associate allowed the publication of a slur as egregious as “snake oil” with reference to my work I’d find it absolutely unacceptable. The fact that it is, as you rightly point out, clearly libelous, is even more shameful.

Thanks Ivan

Appreciated

I am more than ready for the argument

What annoys me is those who make it personal

Which is why Frances Coppola has made her last comment here for a long time to come

As a point of clarification let me say I am not wholly convinced about PQE – as best policy, but I don’t know for sure – and it depends on lots of things.

It is an idea with some potential and in terms of the public conversations it is starting, these are the kinds of conversations, we collectively, as a society need to be having. I am honest enough to say this. Ultimately, my point is that this is all about politics, not coming up with the perfect best fit oven ready policy, – which only exists in the individual imagination in any event. I’m not convinced the economics fraternity and those broadly sympathetic to stimulus + infrastructure investment understand, or appreciate the politics of this. Paradoxically, they maybe as fixated with unpicking the deficit narrative as their opponents are in defending it, that they miss alternative ways of opening this up for the public at large.

Totally fair comment APB

But it sure as heck has got a debate going

If I can be persuaded by those of found judgement there is a better way, I’ll be persuaded and say so

And let me be clear: I think the policy will run alongside gilt sales for the current deficit in any case

@apb.

“Fixated with the deficit narrative”

That sounds very much like SWL to me. His blog posting over the summer has degenerated into an obscurantist navel gazing exercise about why the deficit narrative cannot be broken. The great thing about PQE is that it doesn’t accept the framing of the debate in the first place.

To paraphrase Steve Keen’s latest Forbes column, economists like SWL are analogous to rival Ptolemaic scholars arguing about the retrograde motion of Mars in a heliocentric universe.

You get the point

Paddy is asking the question that all good macro-economists trained in DGSE models ask: “I know it works in practice, but does it work in theory?”

Not original, but I don’t remember who to attribute it to.

Are you saying, Richard, (a) that PQE is a tool for dealing with the next economic crisis (if it arrives before interest rates rise) OR (b) that PQE is a means of maximising funds for public expenditure in any economic conditions OR (c) both (a) and(b)? I am genuinely puzzled.

I have answered those questions many times

Please read what I have written

I am sorry if I’ve missed the answer to this question, Richard. Please could you point me to the relevant post(s)?

The reason I asked was that in the last 10 days or so you seem to me to have switched your emphasis from (b) to (a). Certainly, I think there is much consensus that (a) would be worth very serious consideration if there were another economic crisis and interest rates were still at rock bottom. As for (b), it seems to me that more discussion is needed.

See a blog to follow later today

The rest are all here to read

I have now read the Coppola comments and Murphy replies. I don’t understand why the debate is so heated. Writing from the far side of the Atlantic (my usual location is in Rome on the sometimes it seems much farther side of the channel) I don’t understand why you don’t focus on your points of agreement (on which you disagree with all North Atlantic fiscal authorities) instead of your point of disagreement, which seems to me a matter of form not substance.

I don’t think there is an actual economic difference between PQE and the combination of garden variety deficit financed fiscal stimulus and ordinary QE. In particular, the funding costs to the Treasury are the same if the BOE returns the interest the Treasury pays to it to the Treasury (as say Federal reserve banks return their profits which are said interest, plus the interest on its mortgage bond holdings plus sundry minus its expenses). What difference does it make if the bank issues money and invests in infrastructure or if the treasury issues bonds, which are bought by the bank with newly issued money, and invests in infrastructure ? It certainly doesn’t affect the interest costs the UK public sector has to pay.

I understand that form, presentation, framing and public financial engineering may be important in politics. For all I know about UK public opinion (nothing at all) Corbyn’s rhetorical strategy is brilliant. But I am convinced that PQE is old wine in new bottles. I have nothing against that, when there are elections to be won (sadly not likely to be scheduled any time soon). But I can’t understand how a disagreement over form rather than substance can become so bitter.

One final thing. Murphy correctly notes that fiscal stimulus does not require deficit spending. Tax financed public investment stimulates. If the taxes are levied only on high incomes tax financed public investment stimulates almost exactly as much as deficit financed fiscal stimulus. Allowing those who hate high taxes on high incomes (not all of whom are Tories) to present the argument against stimulus as an argument against deficits is a colossal political error. But the observation that, no matter what the Bank does, fiscal stimulus is not the same as deficit spending strongly undermines the case for PQE as a rhetorical strategy. It becomes necessary to argue that it is a better rhetoric than “soak the rich” or that the two must be combined for some reason, but what might that be ?

Thanks for the comment

I think you miss the point: no is suggesting conventional QE at all. That’s dead

It’s PQE or debt

The difference is a) cost (PQE is cheaper) b) clarity: PQE is an infrastructure financing option as PFI has been c) political framing d) debt figures

And I am not sure what the final para refers to. I assume all spending initially is deficit spending: I argue there is more than one way of reclaiming it. I am not arguing per se that tax pays for anything. Tax is just fiscal policy to reclaim deficit spending to prevent inflation

I think you have missed most of the points as a result

Sorry Richard,

I think you’re being unnecessarily thin skinned and reactionary over this. Frances and you are largely in agreement over desirable outcomes, but just differ over method. I’ve seen no evidence that you’ve been libelled by Frances, and it would be shameful to close her out of the debate. As far as I can tell, Frances main objection is twofold.

1. Why should you need to indulge in the same sleight of hand as our current government to hide money being printed rather than openly challenge austerity?

2. What’s to stop the BoE from funding purchases of bonds from your national investment bank by selling UK gilts? This would be possible and would not weaken reliance on the bond markets at all, just add an extra step.

If you and Jeremy intend to present these arguments with Jeremy as opposition leader, I’m afraid you’re going to face far worse than Frances. It’s worth continuing to engage. I’ve followed these debates for a long time, and while I haven’t always agreed with any one point of view, Frances has always been a polite and articulate guide to some of the more arcane features of our current financial system. To shut out a voice whose knowledge can add to the debate weakens your standing considerably.

Let’s choose to differ on the libel: I have made my point and wiser people than me see it

Let’s go to the substance

I am not in any way ducking the challenge to austerity. I appear to be (by accident) the main architect of the only major political campaign arguing against it in the UK. Haven’t you noticed?

And I am not using a sleight of hand: I am using the cheapest form of funding available. That seems prudent to me. And an argument against gilts

And I am not arguing against debt: I think there will be a need for it for current funding.

But I am arguing that the government should challenge bond markets: we are not dependent on the City to fund out infrastructure and I am quite sure that needs to be said

As much, by the way, that the same argument also says that the taxes of the rich do not fund our infrastructure: putting people to work does that. And it is vital that it be made clear that the government can do that without seeking market consent

As for Frances: I have made clear I have tried and (like many) have found her style trying

But then, I know some have that feeling about my style

Maybe, just maybe, you can’t be the sort of commentator both of us are without upsetting people on the way

I for one am glad you have dispensed with that silly pompous Frances Coppola.

She has definitely libelled you – you should consult your lawyer.

She is just another dreadful neoliberal interested in preserving bankers and other neoliberals. Making money and keeping the poor as virtual slaves is all they are interested in.

I dream for the day when this island is rid of them.

That is the first and last comment of this type I will post

I do it to show the sentiment exists

But I am also moving very much more strongly to a ‘we don’t do personal line’ now

And I definitely do not do legal

Apologies, I was only trying to be supportive. I only know about this lady from what I read here.

Sorry if I have offended.

Well you didn’t offend me

But I ma trying to turn the heat down

That thread got rather heated. I thought the obvious critical flaw in Carter’s “snake oil” rant was identified with the point about the BofE’s “target rate”. If the rate of inflation is well below that target (and has been for a long time)then the argument doesn’t apply.

He’s tried to create some sort of pseudo-clever monetary version of a Ricardian Equivalence type argument, and it is one which totally ignores the circumstances of the deflationary, ZLB world that he lives in.

His 2nd major shortcoming concerns the incomprehensible quality of his writing. Being an orthodox economist is no excuse for poor writing.

Bill Mitchell has just written on his blog about PQE being described as snake oil. It is under his entry on his book launch in Maastricht.

He states that the writer is mistaken and is offering snake oil themselves.

There is apparently a misunderstanding by many that fiscal operations are confused with monetary ones.

QE was a monetary operation that improved the reserves of the banks and bond buying and sales help control the liquidity of the banks reserves and this in the controls the base interest rates.

There is a misunderstanding as well because reserves are not used orlentfor the non government sector economy.

BillMitchell has stated tooin an earlier article thatPQE is not in the same family as QE, and needs a different framing because it is fiscal policy, or increases inaset wealth for the economy. It is really what Lord Turner called Overt Monetary Finance.

Good article by Bill

I’ll explicitly link to it

What is the matter with these people (neo-liberals)?

Why are they still flogging a dead horse?

The world economy if not in freefall has certainly stalled.

QE hasn’t worked. It was a temporary, illusory fix, because when the Big Banks are not fortifying their own balance sheets, they are using the money to speculate. This drive up asset prices, hence the formerly buoyant stockmarket and the astronomical house prices in the “premier league” cities.

This is pure “bubble economics”!

Their role should be that of the oil pump distributing lubricant (money) around the entire engine, not a leaky one working on an overfilled sump!

What will it take to make the “neo-classical jihadis” realise that banks DO NOT CREATE WEALTH, they are a means to distribute it?