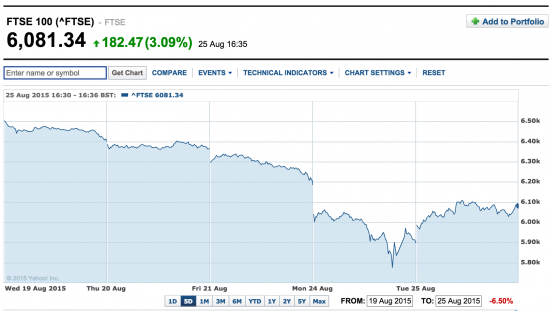

London's stock markets bounced back from Monday's losses yesterday (source: Yahoo):

And it looked like Wall Street would do so as well at first, but then it didn't: it compounded the losses ending the day down (source also Yahoo):

As I write China was looking slightly up overnight, eased, at least in the short term, by falling interest rates . Other emerging economies are not looking so optimistic though. And other news suggests that what is happening is not a blip, but a real issue of deep concern. As Larry Elliott has noted in the Guardian:

It is not just that the growth rate of the world's second biggest economy is faltering, it is that the quality of that growth is deteriorating.

Mike Riddell of M&G notes that the share of gross domestic product accounted for by investment rose from just over 40% in 2007, to 48% between 2008 and 2013, to 54% last year. A higher investment rate is normally associated with higher growth; in China's case it has been associated with lower growth.

Riddell's conclusion is that much of the investment has been wasteful and that China is “trying to hit unsustainably high GDP growth rates by generating bigger and bigger credit and investment bubbles”.

Of all the ways to make an economic crisis that has to be just about the most bizarre, and is the polar opposite of the UK's chosen method, but it is plausible.

And the news is not just bad in China. As the FT has noted:

World trade recorded its biggest contraction since the financial crisis in the first half of this year, according to figures that will fuel a debate over whether globalisation has peaked.

The volume of global trade fell 0.5 per cent in the three months to June compared with the first quarter, the Netherlands Bureau for Economic Policy Analysis, keepers of the World Trade Monitor, said on Tuesday.

This has the feeling of fundamentals coming into play.

China has reacted by cutting interest rates, an option still available to it. But this short term boost to borrowers may just be putting off the inevitable: its economy may really be in a bad shape. The only bright side is that all those new coal fired power stations may not be needed, after all.

And what of the rest of the world? The option of interest rate cutting - the standard response for some decades now to any looming crisis - is not available this time. I do not think anyone is seriously talking about setting negative base rates (as yet, at least). So what are the options? The FT notes that:

Investors believe that the recent market ructions have almost killed off the chances of a Federal Reserve interest rate increase next month, but some big-name industry figures are going even further, predicting that the central bank's next move will be to restart quantitative easing.

Lawrence Summers, the former Treasury secretary, and Ray Dalio, head of the world's biggest hedge fund manager, this week indicated that the US central bank should consider restarting its “quantitative easing” programme

So much for all that confident comment from the like of Chris Giles on the FT aimed at me only a week or so ago saying there was no more need for QE now.

And I still should stress that, of course, we may not be in recessionary territory. This may all be a blip. But the fundamentals do not feel like it. Whilst recessions have not historically begun with commodity price falls, as has been happening in response to the current situation, this time it feels different: those falls look like a reasoned response to the market fundamental of falling demand, starting in China and spreading far and wide.

If that is what is happening we will need QE in the UK. But, as I have shown, that can, and I am quite sure should, include People's Quantitative Easing. This idea may be the subject of near perfect timing. By chance, I would add. But that's the way it is in economics.

And this time, if there is a recession, we must not waste it as we did in 2008. Then we did nothing to really reform the economy. This time that must not happen. How to do that is the subject of the next blog.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

It is difficult to persuade even the most cynical readers here that the intent of George Osborne’s policies is simply and solely to accelerate the concentration of wealth: but I can assure you that the effect of his response to an asset bubble crash will be to protect and subsidise the wealthy and the banks, and ensure that all losses are borne by the middle classes.

Single-property buy-to-let investors, small businesses, younger homeowners, and middle-aged professionals with pension portfolios wil be hit, hard – if not impoverished, Argentinian-style – if the downturn is severe. And yet the market for imported yachts will continue to grow.

The IDS agenda for Social Security is best left unexamined: suffice to say that a crisis is an opportunity, for some.

Simple question. When £75billion was wiped off the UK stock market on Monday, where did the £75billion go?

Is some lucky trader walking around with £75billion? I doubt it, I think the £75 billion just disappeared into thin air.

Likewise, on Tuesday and there was a £45billion bounce back, where did the £45billion come from? Likewise, the money just appeared out of thin air.

I suggest that these are useful questions to ask “sensible” people who pour scorn over thin air theories and PQE.

As far as I can see, money is only real when it moves (the tiny fraction of shares that were actually traded), or when it relates to a useful asset.

On that basis, Jeremy Corbyn, opposing benefit cuts, and proposing PQE, is the only politician with any economic credibility.

You are right

It is just ‘thin air’

Unusually, Richard, I disagree.

Try telling the tens of thousands of Chinese small investors that their hard-earned savings and pensions (now languishing in the fetid vaults of the big players) were just thin air. Or, for that matter, Black America which was similarly destituted in 2007-8.

The popular (amongst marketeers anyway) term of ‘corrections’ should perhaps be renamed ‘re-adjustment’ to properly reflect what happens in these scenarios.

The (admittedly faux) finance of the markets creates the apparent buoyancy of the World’s exchanges to lure in the unsuspecting small investors before vanishing in a puff of smoke creating a contraction.

Unsuspecting small investors bring virgin (real) money into the markets, naively lured by the high returns of the ‘boom-times’, only to lose their shirts when the markets turn.

That same electronically generated finance then reappears to snap up the previously overvalued equity now sold cheap by the gullible small investors.

The ‘re-adjustment’ that ensues is a question of where capital resides before and after the ‘correction’. It is nothing less than a cyclical business model that results in bounteous harvests for the money men and destitution for the rest of us.

In the meantime the big players in the markets act like truculent, indulged children demanding of governments that ‘either you print us some more money or we’ll bring the whole creaking edifice crashing down’.

It is frightening that even the mighty Chinese Government, having opened Pandora’s box seems powerless to resist the visceral forces of the free market.

None of which, of course, undermines the central tenets of your thinking (the contrary in fact).

Forex and LIBOR demonstrated beyond doubt the way in which the main players in the Global Capitalist system act organically and in concert.

If the omnipotence of the Bankers and Traders (and their ability to suck the real money out of macro and micro-economies is to be challenged it will require exactly the sort of measures you propose in green QE and progressive taxation.

But we must- MUST -stop naively thinking that any of this is accidental or unplanned.

We agree on the last point

Michael G.

“money is only real when it moves (the tiny fraction of shares that were actually traded), or when it relates to a useful asset”

That’s a great observation and one that is rarely appreciated. It is remarkable to think of the amounts that are borrowed against collateral values that are essentially nominal.

True

http://www.zerohedge.com/news/2015-08-25/cutting-through-hft-lies-what-really-happened-during-flash-crash-august-24-2015

Good article by Martin Wolf on China in today’s FT.

Agreed