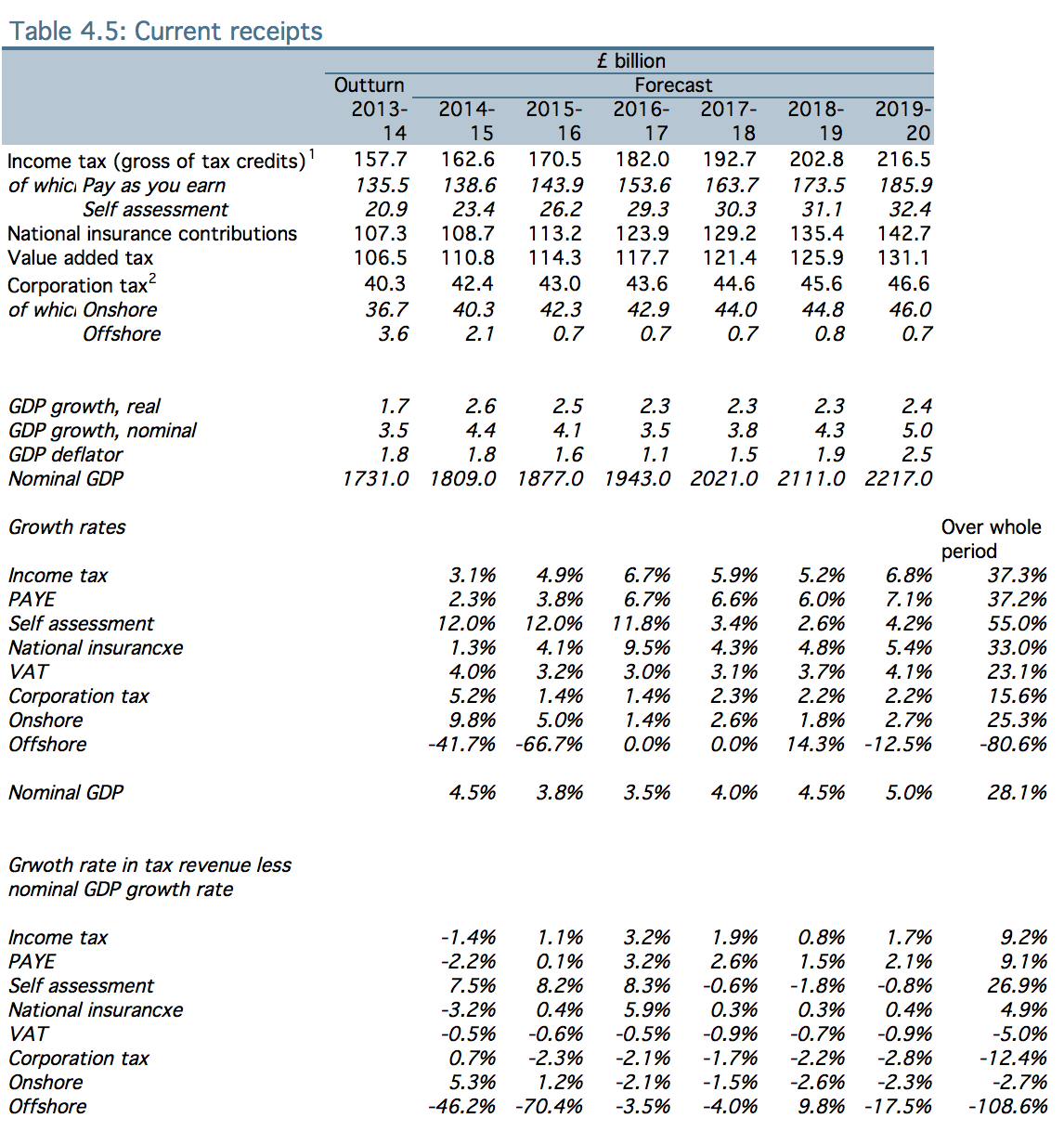

It's always interesting to see where a Chancellor expects to pick up tax from. I did such an exercise a year ago on Osborne's 2014 budget and I thought I would repeat it today based on this year's data (table 4.5 in OBR report fro those interested):

The data covers the main sources of tax revenue, stated at current prices and compares their growth with nominal GDP, also stated at current prices.

The assumption is that there will be nominal growth i.e. unadjusted for inflation, over the forecast period of 28.1%

Curiously VAT does not reflect that fact. It must be that George Osborne thinks that a significant part of growth will be saved. I think that very unlikely.

But he does definitely think there will be income growth, or more likely, increasing income tax rates that he has yet to announce because income tax yields are set to grow by 9% more than nominal growth. That is slightly down on last year though, when the projected rate was 10%.

The optimism in the growth of self employment remains astonishing: this is the only obvious basis for the growth in self assessment yields and they are forecast to grow 26.9% more than nominal GDP, although that is down from the 35% a year ago.

But the one thing you can be sure of is bigger business run through limited companies is going to have a good time. Onshore corporation tax growth (that's everything but oil, which is the offshore figure) is set to fall in real terms, although not by as much as last year.

However looked at though, Osborne intends to give big business an easy time of it over the next decade whilst making heroic assumptions on the profits to be made by the self employed and significantly increasing the taxes that will be due by the 25 million of so people on PAYE in the UK.

That's the story of the budget he does not want to tell. That's the reality that the figures tell.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

Really interesting. So income tax goes from bringing in 3.9 times what corporation tax brings in to 4.7 times- pretty big change.

That could imply that tax rates will shift, as you suggest. But could it not also imply that more corporate revenue will be taken up by wages, with less available net profit? Does it not imply an anticipated shift in earning power from shareholders to wage earners? Or am I being naive? (entirely possible, these are genuine questions!)

That shift in earnings to labour would be unprecedented

Assume it is tax rates, I suggest

The interesting question that comes to my mind with this table (as with others from the OBR at budget time each year), is: does the OBR have a discussion with Osborne about what he plans before they make the “assumptions” on which their forecasts are based? Or does the OBR make their “assumptions” and forecasts and then Osborne decides what his policies will be?

Either way, the degree of fit between one and the other is always extremely helpful to Osborne.

And yes, I know the OBR is supposed to be independent. But as long as it remains inside the Treasury that can be seen as about as independent as my fingers are from my brain.

I too doubt the OBR independence

From The Guardian, Richard, so on some things at least the OBR is “off message”:

‘The rhetoric of the OBR has annoyed the Treasury as the budget was designed to slightly ease the pace of austerity to undermine Labour’s argument that the Conservatives wanted to shrink the public sector back to the level of the 1930s as a proportion of national income.’

Maybe….

I think the OBR is “semi-detached” to purloin a famous phrase; it can’t be seen to be too slavishly devoted to the chancellor (no doubt the “roller coaster” phrase won’t go down too well with Osborne either), but as Ivan says it can’t be trusted to do its job properly whilst inside the Treasury. The IFS is far more trustworthy surely.

A genuinaley independent structure with its own governors funded by gov’t better still

IFS has its own weaknesses