I cam across section 32 of the Finance Act 1951 yesterday (as one does, in my line of work).

The key phrase in this is:

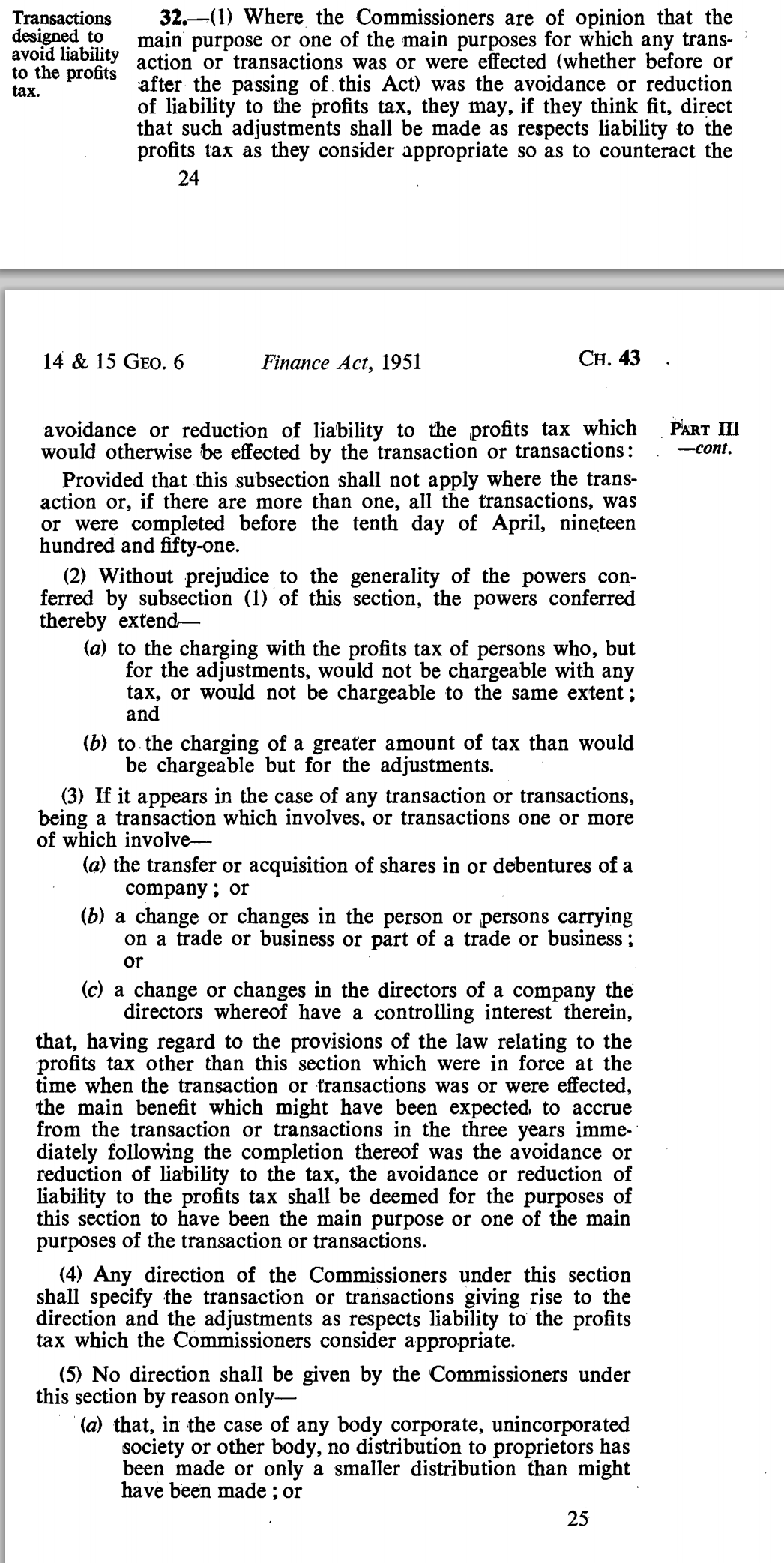

Where the Commissioners are of the opinion that the main purpose or one of the main purposes for which any transaction or transactions was or were effected was the avoidance or reduction of liability to the profits tax, they may, if they think fit, direct that such adjustments shall be made as respects liability to the profits tax as they consider appropriate so as to counteract the avoidance or reduction of liability to the profits tax which would otherwise be effected by the transaction or transactions.

Any way that this section is read it is a general anti-avoidance principle. For the sake of doubt, I reproduce the section in full, below. The title of the section as a whole is

Transactions designed to avoid liability to the profits tax

Can it be clearer than that?

Now, let me put this in context. This section related to profits tax, which predated corporation tax. In other words, this only applied to companies, hence all the discussion of debentures, change of ownership, and the like. And the provision died with the introduction of corporation tax in 1965.

And yet it was radical. It even had a clearance procedure in section 6 as I read it - something that is now said to be impossible.

So the question is, why did this die in law, when it clearly served a purpose and was not (I gather) seriously litigated?

And if that's the case - why did we end up with the near useless General Anti-Abuse Rule (and I say that acknowledging I helped write it, as part of a committee dedicated to producing legislation that would not deliver).

Answers, anyone?

Thanks in the meantime to Paul Donert for this.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

We still have it in the tax code now. Its most famous iteration is in s.703 ICTA 88. And I’m pretty sure it’s drafting is he inspiration for our present GAAR.

I also think our earliest TAAR was in the 1930s – 1932 rings a rather dull bell.

In a draft of the blog written last night I did refer to ‘echoes of the legislation’ and ‘transactions in securities’.

I then took it out this morning because I decided that I did not see the echo

This 1951 law is so much wider I did not see sufficient link to make the connection. I am still not sure I do

Yep – Heather Self has also corrected me (what a wonderful community we have – friendships never get in the way of promoting accuracy). The Transactions in Securities regime began in 1960 FA. Apologies to your readers.

Thank you!

I’d suggest it’s largely because the dynamics and power relations in societies and economies have changed since that time, Richard. Most obviously we’ve seen the rise of the multi-national corporation (MNC) and the increasing financial and economic clout that goes with the size of an enterprise (and the driving force behind globalisation, of course).

Alongside that we’ve had the growth of whole industries devoted to supporting and promoting the cause and interest of MCNs: advertising, lobbying, law firms, accountants, management and IT consultants, (and companies such as the the “big four” that cover all of this, obviously), PR, image consultants and brand management, etc, etc.

We’ve also seen the gradual undermining of the position and power of government and related to that the withering of the status of politicians and public administration. What large business is nowadays scared of the “men from the ministry”? – as the events of the past week and HMRC illustrate oh so well.

The latter is, of course, not unconnected to the doctrine of “private good, public bad” that’s increasingly come to dominate public discourse since the late 1970s – to such an extent that senior public servants and government ministers frequently implicitly – and sometimes explicitly – denigrate their own positions, thus ceding further influence and power to corporate actors and interests.

And the previously mentioned “private good, public bad” doctrine has in various manifestations also driven the privatisations agenda that’s been in place since the early 1980s, reaching its zenith with the firesale of remaining state assets and public services under our current government. It should also be noted that where services have been contracted out the terms of the contract, including monitoring/evaluation and regulation, are always tilted in favour of the contractor (i.e. they further weaken the position of government).

I could add to this list, of course, but this is enough to illustrate my point. In summary, in the 1950’s and through to the mid to late 1970’s, government had status and power and thus the means to devise and enforce laws against those who sought to act against the public interest. In the 21st century under governments of a neoliberal persuasion the state and has simply become the whore of big business.

I have just been interviewed by the FT on this very issue

I should have used that last line

But offered some other choice ones anyway

We do, of course, agree

Will be interesting to see what they make of 30 minutes of interview

I came across art 95 in the Zambian tax law some time ago, and it looks very similar, and is probably more or less a copy paste from the UK tax law from the time of Independence 50 years ago. I would not be surprised if other African states have the same GAAR in their tax law. When I first read it my first reflection was “finally a GAAR with teeth”. But then, teeths have no use if you don’t want to eat (on second thought, they makes your smile nicer).

Section one of art 95 is as follows:

“95. (1) Where the Commissioner-General has reasonable grounds to believe that

the main purpose or one of the main purposes for which any transaction

was effected (whether before or after the commencement of this Act) was

the avoidance or reduction of liability to tax for any charge year, or

that the main benefit which might have been expected to accrue from

the transaction within the three years immediately following the completion thereof, was the

avoidance or reduction of liability to tax, he may, if he determines it to be

just and reasonable, direct that such adjustments shall be made as respects liability to tax as he

considers appropriate to counteract the avoidance or reduction of liability to tax which would

otherwise be effected by the transaction.”

There is a legacy then…

It looks very similar to the anti-avoidance power relating to Income Tax that still exists in the Isle of Man.

And Jersey

It is one thing to have a law it is another to make it stick. Wasn’t it the 50’s when a good many began to use tax havens such at Isle of Man and Channel Islands, think of Norman Wisdom as an interesting example? Major problems are that first you need the evidence and then to make it stick in Court. Then it was in a world of mountains of paper and manual effort. These days it is very different, more complex and even harder to track. Again, then few were actually caught and successfully dealt with. This itself encouraged more and more tax evasion. Certainly it has all got seriously out of hand and damaging but just how you now can stop it I do not know.

But without the right law there is no point even chasing

So the law has to come first

Ed comment: Deleted: changing names does not change IP addresses and you are PaulB by any other name