I was quoted in a Daily Mail story over the weekend on Thames Water. As the Mail noted:

Thames Water sparked fury yesterday when it announced it will not pay corporation tax for up to a decade.

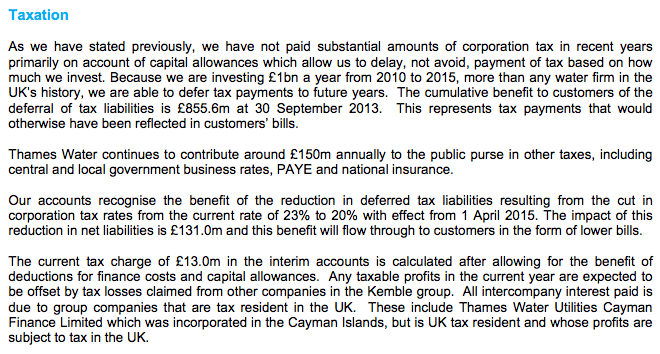

Britain's biggest water supplier has already been berated for racking up more than £1billion in unpaid taxes.

But as it reported soaring profits after the summer heatwave, finance director Stuart Siddall said: ‘It will be seven to ten years until we pay tax.'

Labour's Margaret Hodge, chairman of the Commons Public Accounts Committee, called it ‘deeply unfair', saying Thames Water — which is owned by an Australian consortium — had an ‘obligation to pay their fair share in tax'.

Tax accountant Richard Murphy, who helped expose tax avoidance by Starbucks, said: ‘The reality is that much of this will never be paid.

‘They are never going to stop spending money on infrastructure, which means they will probably never pay tax. Companies like this have to say when and if they will ever pay tax.'

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

I’m with Thames -can you change your water supplier-No!

here’s what Ofwat says:

‘Under the current legislation, household customers are not able to change their water supplier or sewerage service provider. The water or sewerage company that supplies your property will depend on where you live.

Only non-household customers who use more than 5 million litres of water a year (50 million litres in Wales) can choose their provider.

In 2002, the Government said that it would not introduce competition for household customers. It felt that the cost and complexity of the regulatory regime that would be required would outweigh any benefits’

Oligopoly once again – nationalise them or give us choice!

Shock horror.

Company invests huge sums in its infrastructure and legally claims capital allowances in exactly the way the legislation envisages which results in no taxable profits.

What would you like to happen? They stop investing? They put up bills? Both might result in some profit which could then be taxed but to what benefit?

Thames Water are doing absolutely nothing wrong here yet you continue to create an atmosphere in which the public now assume that any company not paying huge amounts of tax ‘must’ be up to something.

You clearly have not rad what I wrote

Please don’t call again

I think requiring companies to state when DT will fall due is too strong: it is impossible to do it with any accuracy. A disclosure of the projected position might be interesting as an indication, however.

But I’m not sure that knowing when a company is likely to pay cash tax is information worth having, other than to satisfy my curiosity. It doesn’t affect the amount Government receives; and investors should understand that the value of the DT liability (or asset) is based on the headline rate which is only known a year or two in advance, so any DT figure should be treated with a pinch of salt.

By the way, I’m curious as to where you think avoidance might be taking place, if the Cayman Islands company is UK-resident. The piece in the Independent seems to be asserting avoidance because of the CI connection, but if that’s not a problem…?

And what does the the CI company pay?

I have not checked

And I see every reason why a cash projection is needed and explained why in the piece

If the CI company is UK-resident then it’ll be paying the normal rates. Unless it has its own borrowings from outside the UK, of course, but there has been no suggestion of that. In the absence of any suggestion of profits flowing outside the UK there seems to be no evidence of any avoidance.

I see why you think a cash projection might be helpful, but as it would have to be hung around with so many caveats it would be of very little use to any investor aware of how DT works, and misleading to anyone not aware of it. Mandatory reporting of figures that can’t be relied on seems counter-productive.

So you’d rather a void?

Odd how vested interests have always thought that best when it comes to reporting

Coming at it from the business side, all I’m thinking is that if the information is of no value to the users of the accounts then it’s a shame to force people to spend time and effort providing it.

Certainly when I’m involved in valuing a company we wouldn’t go with the DT figure in the accounts, even if it did have a projection – we’d dig into it to get much more detail of how it’s made up so we can form our own view. Providing that level of detail in as a matter of course would make the accounts unworkably obese.

So yes, the information is interesting and useful, but I dont think that putting it in the accounts is a sensible way of getting it across.

If DT were a simple subject then I’d be right behind disclosing it more fully. But it isn’t, so I’m not.

How am I a vested interest, by the way? If anything I’d get more work out of helping companies navigate the minefield of extended disclosure. Though they’d probably not want to pay for it…

You seem to ignore the International Accounting Standards Board’s stated purpose for accounts

They’re not for you when buying or selling

They’re for markets who can’t ask that question

Would you like to recall that?

There are many users of accounts, and most of the accounts out there aren’t being examined by people looking at buying a few shares here and there.

Even if you could get a precise figure in there in a usefully concise form, which is a challenge, there is more uncertainty about what future profitability is going to be than how the DT will reverse. To get any sort of accurate DT forecast in there you’re going to have to have a profit and investment forecast – and out of profit, capital investment and deferred tax I think DT is the least important to investors.

Now if you were recommending that companies should do a five-year forecasts of revenue, profits, investment, pension fund performance, future government tax policies, and so on, then projecting the DT reversal would be a good thing to tag on as well. But it would depend on all those, and be behind them in importance. Not to mention being surrounded by so many layers and layers of caveats about forward-looking statements as to be useless.

Your comment is irrelevant

It is those isn the capital market that all shares are prepared for – that’s what the IASB says

So why is DT data irrelevant?

Please answer the only relevant question

DT data is not irrelevant.

However, a forecast of how DT might be expected to reverse in the future would:

a) require a host of other forecasts to be made and disclosed if it is to have any context, none of which could be relied on

b) therefore be so vague as to be useless at best and misleading at worst.

But DT estimates require those forecasts to be done anyway

In that case your argument falls flat

There’s a big difference between the workings required to justify recognising DT in the accounts, and the work required to determine when DT will turn around.

In the Thames Water case we’re talking about saying when a DT liability will crystallise. For accounts purposes all we can do with a liability is show the full liability: it doesn’t depend at all on when it will reverse. The only reason you could not show part of the liability is that it is explicitly disregarded by FRS 19 (or IAS 12) – or you could discount it, if you’re using FRS 19, but this is rare in my experience as smaller companies don’t care and larger companies tend to prefer to be in line with IAS 12. Short of that discounting, there is nothing you could do with profit forecasts that would have any impact on the presentation of a DT liability.

With a DT asset you have some judgement to bring in, and that is where the profit forecasts come in. But you have to be prudent about it, and you could only recognise an asset to the extent that you think it more likely than not that it can be recovered. So if you have an asset and really want to recognise it then you have to do some work. If you were to disclose the underlying cacluations in the accounts, however, you’d only be showing an unreliable estimate of when you’re *not* going to be paying tax, which is not what you were after.

So if DT will become “due and payable”, because there’s a liability, then your suggestion would require significant extra work to be done, and I would take it with a pinch of salt.

Apart from anything else, if we’re looking at a blue chip multinational then a major component of the DT is share-based payments, and the impact of that on the DT is going to depend on share price over the life of the options. Do you really think that a disclosure based on a company’s estimate of its future share price is going to be worth anything at all?

Almost all companies have DT assets as well as liabilities – they cannot be offset in many cases

So the forecasts are made

And before IAS partial provision was allowed and was done – so please let’s not pretend otherwise

I’m not aware of a lot of assets and liabilities that can’t be matched off. Capital losses, yes. Otherwise one can pretty much put everything through the trade – at least in the UK. And the matching happens before you start considering whether the assets are recoverable – if you have net DT assets, you will invariably recognise the assets at least to the extent that they cancel out the losses.

Partial provision used to be done, and then it was agreed that it was misleading and open to abuse as it was a pretty subjective area, so the only consistent approach was to do away with it. Are you really recommending that – in order to help investors – companies should be required to put their guesses in as gospel?

Small world view Andrew, if I might say so

And losses are carried forward against the same trade

OK, then give me some examples from other systems. I don’t pretend to be an expert in areas I’m not familiar with, which is why I limited my comment to the UK.

I know perfectly well how losses are carried forward. How many companies have more than one trade? Not very many: for this purpose we’re only really looking at the position where an existing company has acquired a loss-making trade, and the number of such cases where that trade isn’t expected to profitable is smaller still – you don’t buy a business if you think it’s going to stay loss-making.

Within a group is a different matter, but again it is normally possible to sort things out so you can eventually get relief for your previous economic losses. The restrictions on losses are unfair, but they’re not so sweeping that they deny everything.

So yes, there are exceptions – but only a few.

I think more than you think…

Examples?

Do you really want a discussion of losses?

If it’s interesting then yes, certainly.

Sorry…but it may be interesting to you, but no one else

And I have work to do

Sorry – you offer to discuss something out of the blue, then decide not to? How odd.

I have work to do too, but I can spare a few minutes here and there.

So can I – that’s how this gets done

but there is a limit

And this is it

You posted about Thames on 11 June and I pointed out that tax is a cost that directly taken into account in setting their prices.. You asked for evidence with a link which I provided but you didn’t comment on it. Your latest post seems to have ignored what that link showed, which is that low cash tax does actually keep bills down for customers.

I made clear I knew about it

I made clear that’s simply wrong: the rules must be changed

Which rules must be changed? The inference I draw from what you’re saying is that the prices a water company charges should not relate to the post-tax profitability of the company – is that correct?

Of course they should not relate to post tax profit

Any business where price relates to post tax profit is by definition behaving monopolistically and against the interests of the consumer

Isn’t that obvious?

Thank you. I shall tell my client that his small corner shop is a monopoly and he is going against the interests of his customers, when he raises prices so that he and his wife have enough to live on.

Your shop customer will not adjust prices in that way

I guarantee you

Ah. You guarantee it, eh?

He says he does. I wonder whether he’s lying, or just doesn’t know how to run his own business.

I simply don’t believe him – unless he is in very specialist non-competitive market giving him a local or specialist monopoly

Or, perhaps, real life doesn’t fit your economic theories?

Or, perhaps, real life doesn’t fit your economic theories?

Interesting that you have in error revealed yourself as someone who has an identical IP address with someone long barred from this site tonight

Game over – now I know you are wasting my time, just as you did in your previous incarnation

Banned? I stopped posting when you stopped talking about tax, and thought I’d start again when a tax story came up. But this time I thought I’d use my real name, as you’d said something about not liking pseudonyms.

No – it was a ban for trolling evidenced by deletion for time wasting