The government published its review of the submissions made to its consultation on the country-by-country reporting that will be required from financial institutions (mainly banks) under the EU's Capital Requirement's Directive (CRD) yesterday. It also published a revised impact assessment.

To summarise what will be required under the CRD, the institutions affected will be required to publish their turnover, number of employees, profits earned, taxes paid and subsidies received on a country-by-country reporting basis.

The outcome was, perhaps, better than I expected because the approach adopted has been a very clear requirement that data published reconcile with the consolidated accounts of the institutions reporting this data. It was possible that an alternative approach, which would instead have published local data that would, when aggregated, not reconcile with the group accounts (the so called 'bottom up' approach) would have been adopted and that would have resulted in seriously conflicting information and a lack of data on just where group profits really are. This has been avoided, with the support, it seems, of business itself (disappointingly I supplied what looks like the only civil society submission to the review).

There is further good news in that turnover is to reconcile to the accounts and no standard template for production of the data is to be ordained: I feared that may restrict disclosure. It is also good that audit is expected, whether or not the data will be in the statutory accounts. This is very welcome, and sets a powerful precedent for future country-by-country reporting. A compromise on audit of the first published data seems fair.

It's also very good news that an exception for smaller entities has not been given: the government has rightly said that smaller entities tend to be less complex and therefore the burden on them is correspondingly smaller and as such an exemption for them is not needed under this new requirement: I wholeheartedly agree.

But that is not to say there aren't problems with the outcome. Firstly, and most importantly, tax paid has been interpreted literally and cash tax paid is to be used as this measure, which is absurd as cash paid in a year for tax does not relate to profit in a year. I warned EU legislators on this issue when this law was rushing through the parliament and was advised I should accept whatever we get, but this is a poor outcome. The only good news is that the report suggests fuller disclosure and narrative notes will be allowed and encouraged, not that I see it happening, at least for now. This will cause problems, I suspect, but equally - those who told me to take what I could get were right.

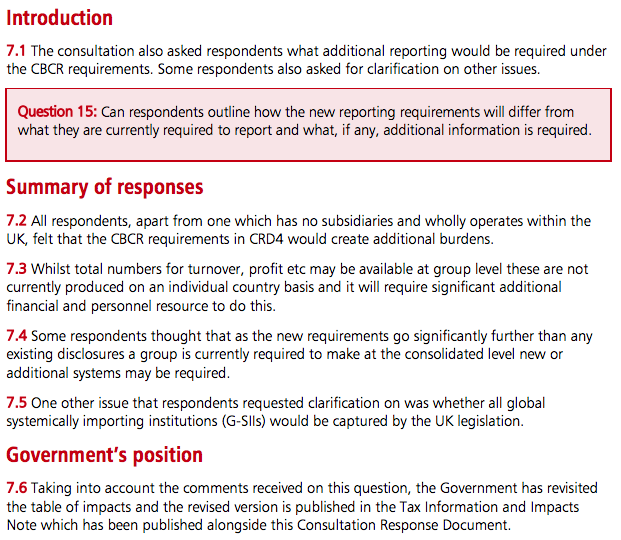

And it's also encouraging to see that the government has simply rejected the view that this proposal places too much of a burden on business. I'll simply reproduce their response on this issue:

The objections have simply been dismissed: this is very good news. What the impact assessment shows is that the government thinks the cost of this data may be between £3 million and £5 million a year for the companies involved. Personally I doubt that, but if true still think it worthwhile. And what this will then set is the precedent for the approach which I then expect to rapidly spread into other sectors.

What does worry me though is the government's response on the expected benefits of the data. They say:

The CBCR requirements concern reporting arrangements, not tax or policy. Therefore, the measure is not expected to have any significant economic impacts.

It is very hard to see how disclosure of what is happening in tax havens will have no economic impact. Similarly, this comment upon the impact on HMRC looks naive, at best:

We are proposing that the information required under this directive will be reported to HMRC in addition to the Commission. This will be used for risk assessment purposes and have negligible impact on HMRC.

Why improved risk assessment at HMRC won't have an economic and tax benefit is hard to understand. I think there is some posturing going on here as there is in the summary of 'other impacts' which says:

Other impacts have been considered and none have been identified.

Knowing who does what, where, does not apparently have benefit, therefore. I beg to differ.

But I can't get too worked up. The outcome is better than I hoped for: banks will have no choice but prepare country-by-country reporting data from July 2014 with it being audited in its second year onwards and with that data being required to reconcile with audited accounts. The tax data may be naively chosen and simplistic in style but in that case we'll use it at face value as a measure of what is really going on in each country where a bank operates to reveal how much (or how little) they pay by place. And that's one of the goals for this disclosure, which, I can assure you, will be used.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here:

You deserve a great deal of credit for the work and commitment you’ve put into this cause, Richard, so it ought to be ‘trebles all round’ in the Murphy household this evening. 🙂

I’m afraid I’m out with a client….doing practical stuff

Maybe tomorrow

Congratulations Richard for your persistence on CBCR. We can use this victory in our own places to push our own governments.