The Finance for the Future’s report ‘Making Pensions Work’ when combined with my work on the tax gap shows that there is now an alternative narrative available ion how to finance the sustainable growth this country needs.

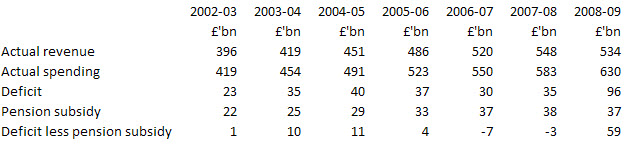

As I’ve noted already on this blog, the deficits from 2002-03 to 2008-09 were as follows:

Of course matters went out of hand in 2008-09. That had nothing to do with Labour: that was the crash caused by the irresponsibility of the City.

It could be argued that the deficits before then were Labour’s choice, but note that this so called ‘structural deficit’ arose from misplaced belief that the private pensions industry could deliver two things. The first was real growth for the UK economy by investing responsibly. The second was sustainable private pensions. They did neither. In fact, in 2007-08 private pensions were £35 billion and the subsidy paid to provide them some £3bn more.

The average deficit in those years was around £35 to £40 billion — and would be a bit more now. Much of it was due to investment spending. This is the so called ‘structural deficit’. But the reality is that this deficit can be, and should now be, covered in two ways.

First, as I’ve suggested in ‘Making Pensions Work’, up to one quarter of the £80 billion current annual pension fund contributions (or £20 billion) — should go into new investment that must be proven to result in new productive activity in the real economy. That could be by investment in a Green Investment Bank, by investment in a Green New Deal, by investment in infrastructure in place of PFI, or by investment in the shares or bonds issued by a company — but those companies would have to show the proceeds of issue were being used for new investment and not for refinancing debt or paying for acquisitions or they would not qualify. This releases £20 billion of investment into the economy — to create the work and wealth that is needed for our long tem benefit.

Match that with the £20 billion I estimate could be raised by a concerted effort to close the tax gap — as an initial target — and there is £40 billion of funding needed to get our economy going again. Do that and we will have growth in the UK. And with growth in the UK the deficit will melt away — because tax receipts will clear it.

The point is a simple one: we now have the alternative economic narrative we need to show cuts are a choice, not a necessity. They’re a choice to impose cost on the UK: the real cost of mass unemployment, of failing public services, of recession rather than the prosperity from growth that I suggest is possible.

This, I suggest, is the narrative labour’s new shadow Chancellor should be pursuing.

Thanks for reading this post.

You can share this post on social media of your choice by clicking these icons:

You can subscribe to this blog's daily email here.

And if you would like to support this blog you can, here: